Best States to Retire for Taxes: Tax-Friendly States for Retirees

Choosing the state that you want to retire to usually involves more than considering just the weather or the type of lifestyle you prefer. You need to consider how far your money will stretch once you’re no longer working. State taxes play a significant role in shaping that reality. They impact everything from your monthly income to everyday purchases. Some states make retirement savings last longer by keeping taxes low, while others add unexpected costs. Below, we’ll look at how income, property, and sales taxes affect retirement planning. We'll also highlight the states where retirees can benefit the most.

In this article, you’ll learn:

- State taxes can significantly affect retirement budgets, influencing income, property ownership, and daily expenses.

- Income taxes: Nine states (e.g., Florida, Texas, Wyoming) have no state income tax, while others exempt retirement income like pensions or withdrawals.

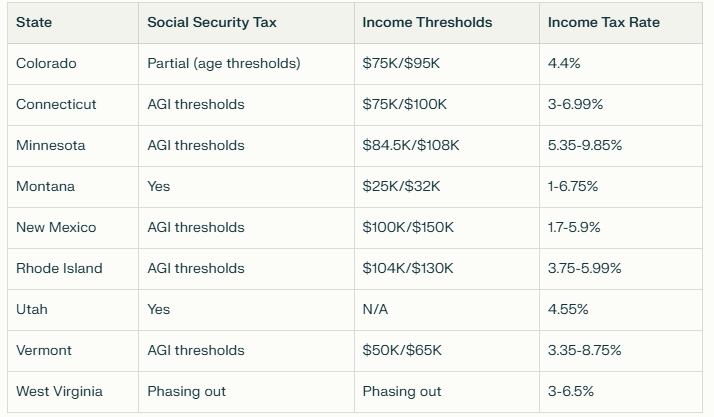

- Social Security: Nine states still tax benefits in 2025, but some (e.g., West Virginia) are phasing them out completely by 2026.

- Property and sales taxes: Some states offer freezes, exemptions, or credits for seniors; others rely on higher taxes that can offset income tax savings.

- Healthcare and cost of living: States like Mississippi and Tennessee combine low living costs with favorable tax policies, making them appealing for retirees on fixed incomes.

- Best tax-friendly states: Florida, Tennessee, Mississippi, Pennsylvania, and South Dakota often stand out for retirees.

- Least tax-friendly states: California, New York, New Jersey, and Connecticut combine high taxes with high costs of living, reducing retirement savings.

- Beyond taxes, retirees should also weigh healthcare costs, proximity to family, and property exemptions before relocating.

Why You Should Start Thinking About State Taxes

When planning for retirement, you need to consider saving enough and decide on where you’ll live. State taxes can add up to thousands of dollars over the course of your retirement, shaping how comfortable your lifestyle will be. The best states for retirement generally stand out because they reduce the financial pressure on seniors. From income taxes to property and sales taxes, the differences between states can vary greatly. That’s why friendly tax states for seniors are worth considering early in your planning.

What Types of Taxes Affect Retirees?

Several types of state taxes impact retirement savings. Income taxes on retirement accounts, Social Security taxation, and property or sales taxes all affect retirement budgets. Understanding how they work lets retirees choose locations that protect their income and make daily living more affordable.

Income Taxes on Retirement Accounts

Withdrawals from traditional 401(k), IRAs, and pensions are often taxed as income. Some states tax these earnings at full rates, while others offer partial or full exemptions. A handful of states also provide special breaks for public employees, teachers, or military retirees. These differences are significant for people who depend heavily on their savings. For example, moving to a state with no income tax makes retirement funds last longer. Staying in a state with higher taxes, however, could reduce your spending each year.

Social Security Taxation

Social Security is taxed at the federal level based on income, but some states also add their own tax. As of 2025, nine states still tax Social Security benefits, though a few are beginning to phase them out. West Virginia, for example, will completely eliminate its Social Security tax by 2026. If you’re asking which states tax Social Security, the answer is important because even a small state-level tax reduces your monthly check. Keeping track of these changes ensures you know what to expect before moving.

Property and Sales Tax

Property taxes can be tough for retirees who rely on a fixed income. In some states, seniors qualify for property tax freezes or exemptions that ease this burden. Sales taxes also vary widely, and they affect everyday spending on groceries, clothing, and household goods. Tax-friendly states for seniors often combine lower property taxes with moderate sales taxes. Together, these savings make a significant impact on how much of your income you can enjoy.

The Most Tax-Friendly States for Retirees

When looking at the best states for retirees, tax policies often make a clear difference. Some states eliminate income tax entirely. Others exempt retirement income or are phasing out taxes on Social Security. Each option means more money in your pocket and fewer surprises in retirement.

States with No Income Tax

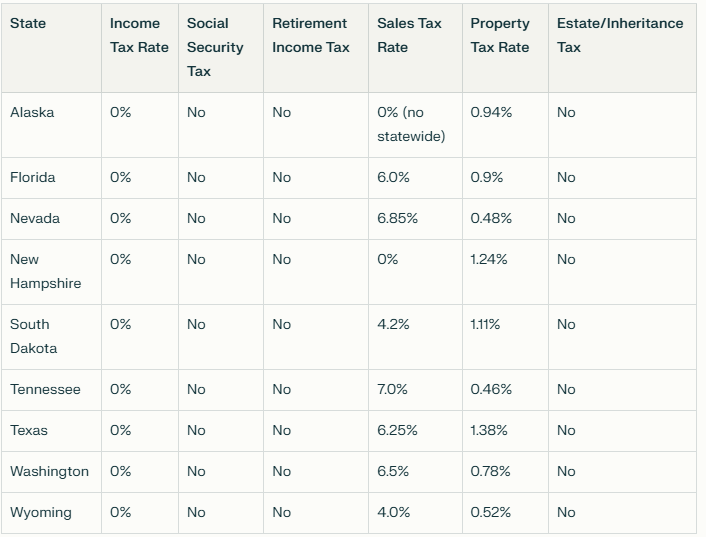

Nine states currently have no state income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. For retirees with large withdrawals from retirement accounts or higher pension income, these states are worth considering. Still, it’s worth looking closer.

For example, Washington now applies a 7% capital gains tax on gains above $270,000. New Hampshire only recently eliminated its dividend and interest tax. Some of these states balance the lack of income tax with higher property or sales taxes, so weigh the trade-offs before moving.

States That Exempt Retirement Income

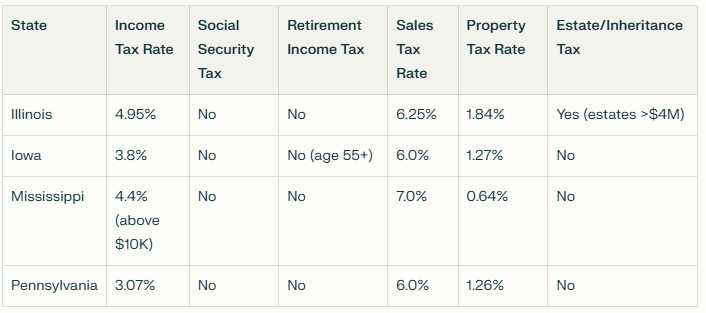

In states like Illinois, Mississippi, and Pennsylvania, retirees can enjoy exemptions on retirement income. Even though these states collect income tax on wages and other earnings, pensions, Social Security, and withdrawals from retirement accounts are not taxed. This can be particularly appealing for people who want to be near family or in larger cities without losing a chunk of their retirement savings. Property tax rates can still be higher in these states, which might offset some of the income tax savings.

States Phasing Out Social Security Taxation

A growing number of states are moving toward eliminating Social Security taxes. West Virginia signed House Bill 4880 into law in 2024, phasing out Social Security taxation over three years. They implemented a 35% reduction in 2024, a 65% reduction in 2025, and complete elimination by 2026. This affects over 50,000 senior households and will save the state approximately $37 million annually. Vermont and others are also making changes, often with income thresholds that reduce or remove the tax for middle-income retirees.

These shifts are significant when planning long-term because Social Security is a core income source for many. Retirees who want stability should monitor policy updates, as they directly impact future budgets.

Other Factors That Affect Retirement Affordability

Taxes shouldn’t be the only factor when deciding where to live during retirement. Healthcare costs, overall cost of living, and senior-specific exemptions have just as much influence on your budget. Looking at the entire picture lets you narrow down the best states for retirement.

Healthcare Costs by State

Healthcare is one of the most significant expenses for retirees, so comparing costs by state is essential. Tennessee, Texas, and Mississippi stand out for having lower healthcare cost indexes, which can impact savings.

This is especially useful when considering Medicare Advantage plans or the long-term costs of prescriptions and care facilities. A healthy 65-year-old couple retiring in 2025 will need $388,000 in savings for healthcare costs under Original Medicare plus Medigap Plan G and Part D, representing a $7,000 decrease from 2024 estimates. As such, even slight differences in healthcare costs between states add up over the years, making this a key part of retirement planning.

Cost of Living and Property Taxes

Beyond healthcare, everyday costs like housing, groceries, and utilities shape retirement budgets. High-cost states like California put pressure on savings, while states like Mississippi and Tennessee make fixed incomes last longer. Property taxes also vary, and in some cases, they offset savings from lower living costs. For retirees, finding the best state to retire on a fixed income usually means balancing low property taxes with an affordable cost of living.

Among tax-friendly retirement states, the cost of living varies significantly: Wyoming (95.5), Tennessee (90.5), Mississippi (87.9), Texas (92.7), and South Dakota (92.2) all rank below the national average, while Alaska (123.8) and New Hampshire (112.6) are well above average, potentially offsetting tax savings.

Senior Tax Exemptions and Credits

Many states offer additional relief for retirees through exemptions or credits. For example, Texas allows homeowners aged 65 and older to claim an extra $10,000 homestead exemption against school district taxes. At the same time, Florida offers up to $50,000 in property tax exemptions. Across the country, some states provide freezes on property taxes. Others reduce or credit the amount owed. These programs are especially valuable for retirees who plan to remain in one place for many years, making certain states more tax-friendly overall.

Best States to Retire on a Fixed Income

For retirees who rely primarily on Social Security or modest pensions, stretching every dollar is essential. The best states to retire usually combine low living costs with tax breaks on retirement income. Mississippi, Tennessee, Pennsylvania, and Florida are all strong options. These states either don’t tax Social Security, have lower housing costs, or keep everyday expenses such as groceries and utilities affordable. For anyone on a steady income rather than considerable retirement savings, the best state to retire on a fixed income is one that balances low costs with a comfortable lifestyle.

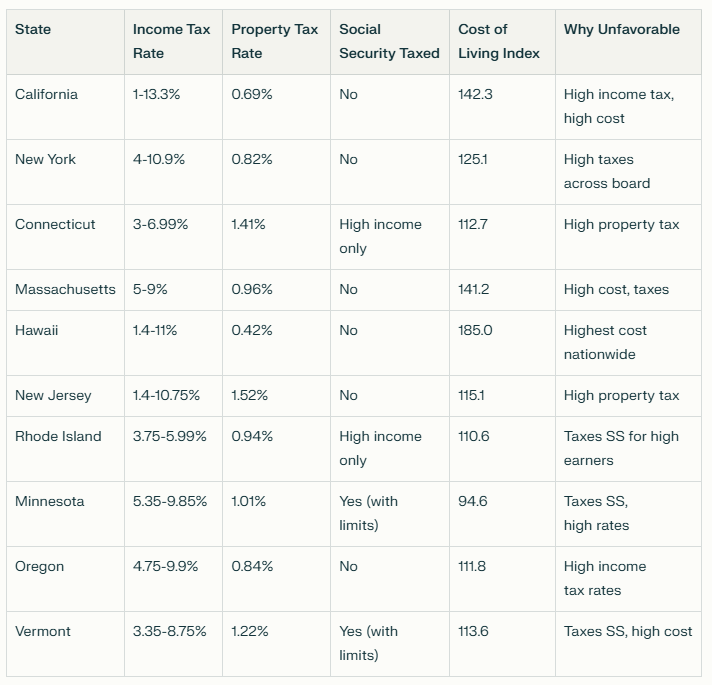

States to Avoid for Tax-Friendly Retirement

Some states aren’t a good match for retirees who want to save on taxes. States like California, New York, New Jersey, and Connecticut often rank among the least tax-friendly because they combine high income tax with a high cost of living. Property taxes, housing prices, and even daily expenses quickly eat into retirement savings. Some of these states also levy estate or inheritance taxes, which affect wealth transfer for high-net-worth retirees. For many, moving elsewhere offers more financial breathing room during retirement.

Making the Best Move: Questions to Ask Before You Relocate

Even if you’ve narrowed down the best states for retirees, moving is a significant life change. Before you relocate, ask yourself a few key questions. Will you be changing your residency properly for tax purposes? How much does proximity to family and friends mean to you? And after accounting for moving costs, will you actually save money? These questions go beyond numbers and bring your lifestyle into focus. For deeper planning, consider strategies like tax optimization to see the complete picture before making a move.

Planning Ahead for a Tax-Friendly Retirement

Finding tax-friendly states is only one part of planning your retirement. Planning ahead ensures you’re not caught off guard by hidden costs or policy changes in the future. Consider how state taxes, healthcare expenses, and property costs will impact your long-term budget. Building these factors into your retirement plan early gives you more flexibility later. It’s a good idea to talk with a tax or financial advisor who understands state-by-state differences. Careful planning now makes your retirement years more comfortable and predictable.

After seeing the impact financial decisions can have on families, Elijah Pell, AAMS®, CEPA, transitioned from a career in accounting and private equity analytics to personal financial planning. Today, he is passionate about empowering post-retirees, business owners, and high-income individuals with tailored strategies that guide them toward their financial goals. His approach to comprehensive wealth management is rooted in deep discovery, bespoke planning, and behavior-aware investing.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy. All advisory services are offered through Savvy Advisors, Inc. (“Savvy Advisors”), an investment advisor registered with the Securities and Exchange Commission (“SEC”).

Works Cited