State and Local Tax (SALT) Deductions: Overview & FAQs

The SALT deduction lets taxpayers write off certain state and local taxes on their federal return. It's a good option for people living in high-tax states. Recent legislative changes have reshaped who benefits and how much can be deducted, so understanding the rules is more important than ever. Below, we’ll cover the SALT deduction, what it includes, and the current limits. We'll also discuss planning strategies and answer some frequently asked questions so you know how it might relate to your situation.

Key Takeaways

- The SALT deduction lets taxpayers who itemize write off state and local taxes such as property, income, or sales taxes.

- Eligibility is limited—only about 9% of taxpayers claimed it in 2022, mostly in high-tax states.

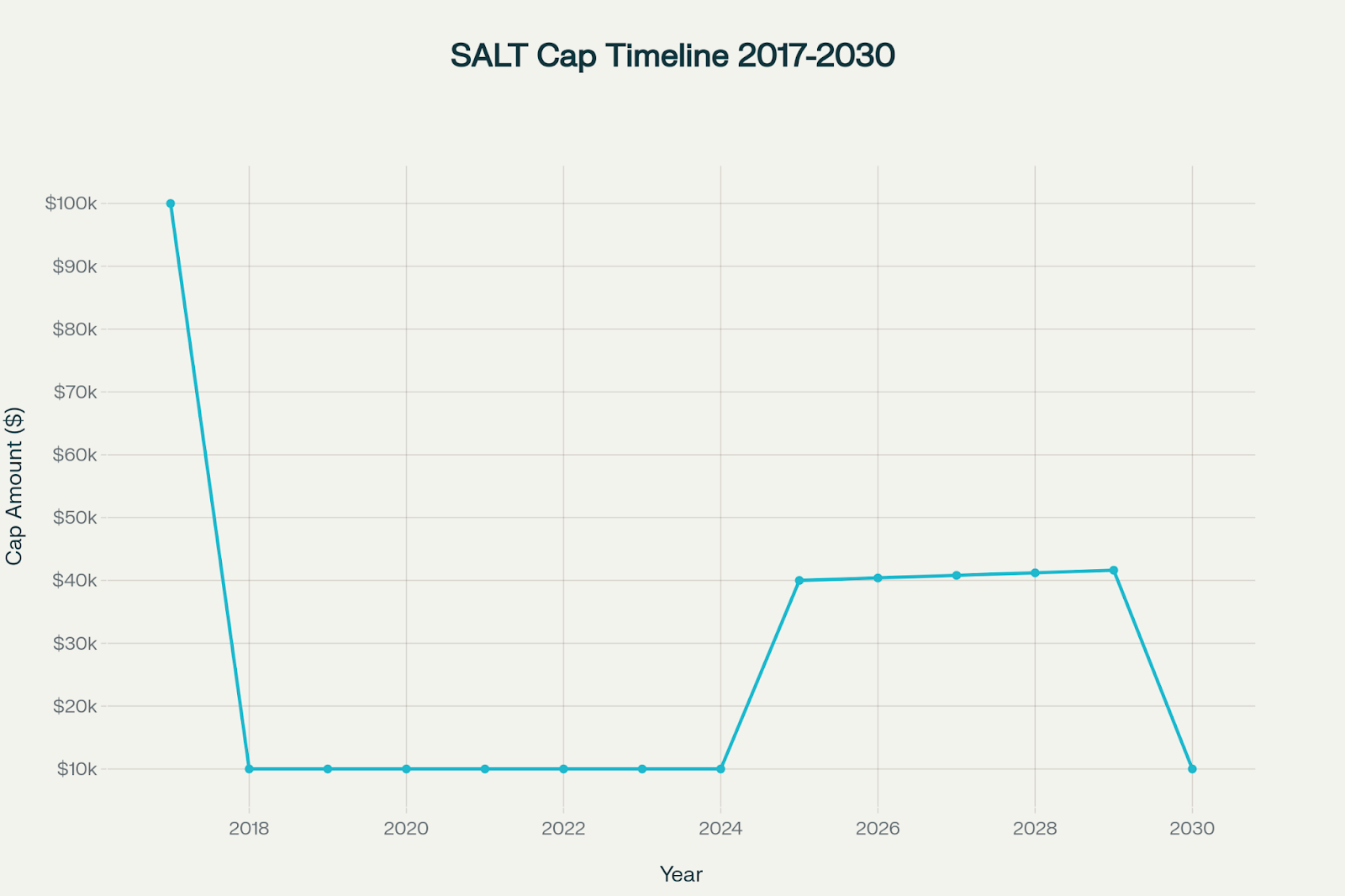

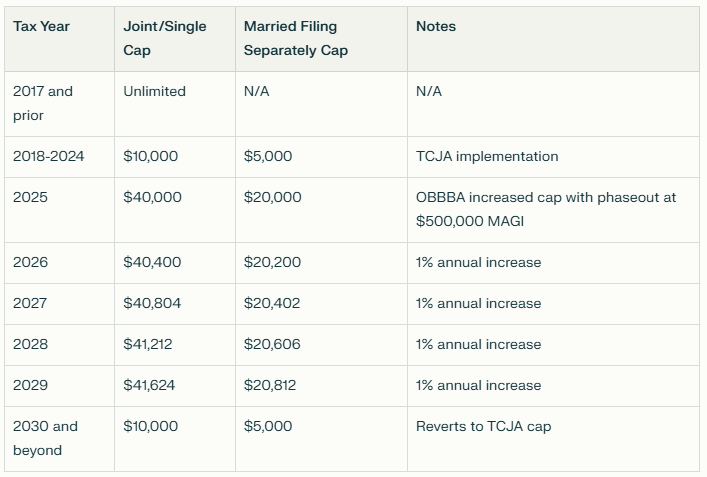

- The SALT cap was set at $10,000 under TCJA (2018–2024), rises to $40,000 under the OBBBA (2025–2029 with 1% inflation bumps), and is scheduled to drop back to $10,000 in 2030.

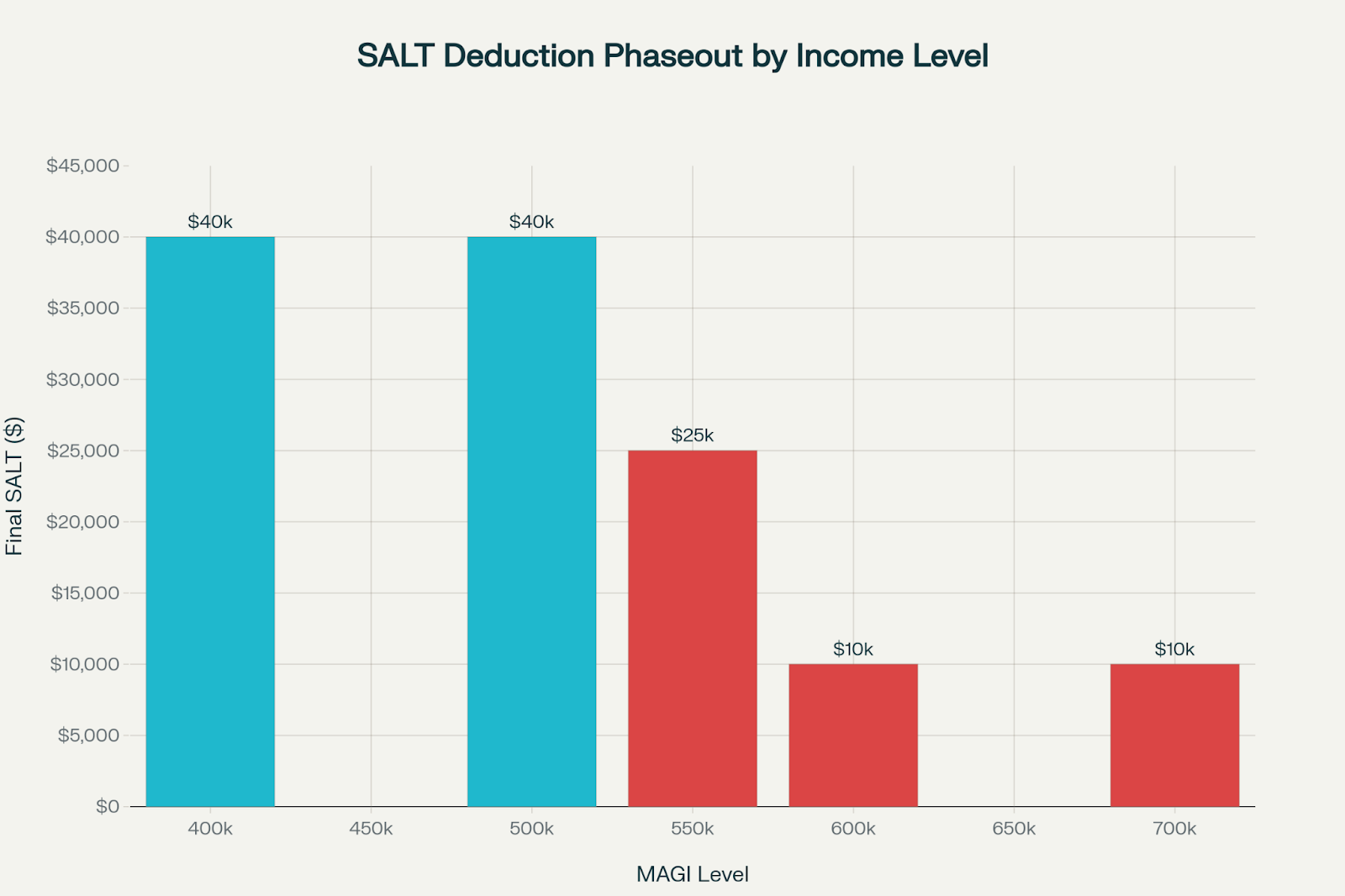

- High earners face phaseouts starting at $500K MAGI ($250K MFS), reducing the benefit but never below $10,000.

- Certain taxes are not deductible, such as federal income tax, HOA dues, and license fees.

- Choosing between the standard deduction vs. itemizing depends on whether your itemized total exceeds the standard ($29,200 MFJ projected for 2025).

- Planning strategies include timing deductible payments, managing income levels, and using PTET workarounds for business owners.

- The future outlook is uncertain, as revenue impacts are large and Congress may adjust the rules again.

What Is the SALT Deduction?

The SALT deduction is short for state and local tax deduction. It lets certain taxpayers deduct taxes paid to state and local governments on their federal return. SALT stands for State and Local Tax, and it’s only available if you itemize deductions on Schedule A instead of taking the standard deduction. The goal is to reduce the risk of being taxed twice on the same income, once by your state and again by the federal government.

According to IRS data, only 9.3% of all taxpayers claimed the SALT deduction in 2022, which is a steep drop from pre-TCJA (Tax Cuts and Jobs Act) levels. Among taxpayers earning $100,000-$500,000, usage fell from nearly 80% in 2017 to just 22.4% in 2022. This shows how recent changes have significantly shifted who takes advantage of the deduction.

What Taxes Are Eligible for the SALT Deduction?

The SALT deduction covers several types of taxes you pay to state or local governments. These fall into three main categories: property taxes, state and local income taxes, and sales taxes.

Property Taxes

Property taxes you pay on your primary home and any second home typically qualify for the SALT deduction. In some instances, personal property taxes, such as annual car registration fees based on the value of the vehicle, might also be deductible. However, costs like HOA (Home Owner’s Association) dues or special assessments don’t qualify.

State and Local Income Taxes

If your state or city charges income tax, you’re able to deduct what you’ve paid during the year. This includes taxes withheld from your paycheck, estimated quarterly tax payments, and even tax owed for the prior year if you paid it in the current year. In high-tax states, this option is often more valuable than deducting sales tax.

Sales Tax

Instead of income taxes, you can choose to deduct SALT. This option is most beneficial in states without an income tax, such as Florida, Texas, or Washington. The IRS gives you two ways to calculate this deduction: use its published tables or keep receipts from your actual purchases throughout the year.

What is the SALT Cap?

The SALT cap sets a limit on how much you can deduct for state and local taxes each year. Before 2018, there was no cap, but tax law changes now place strict limits on this deduction. Understanding the timeline and new rules is key to knowing how much you’re able to claim.

SALT Cap Timeline: 2017 to 2030+

Before 2018, taxpayers who itemized could deduct the full amount of state and local taxes they paid. The TCJA introduced a $10,000 cap, which lasted through 2024. Starting in 2025, the One Big Beautiful Bill Act (OBBBA) raises the cap to $40,000, with a small inflation increase of about 1% each year until 2029. Unless lawmakers act, the limit will drop back to $10,000 in 2030.

New Limits Under the SALT Deduction Cap Bill (OBBBA)

Beginning in 2025, the new SALT deduction cap bill changes how much taxpayers can claim. The cap increases to $40,000 for joint filers and $20,000 for married couples filing separately, with a 1% annual adjustment through 2029. This higher threshold creates more opportunities for itemizing, especially in states with higher property or income taxes.

The OBBBA actually phases down the $40,000 cap for taxpayers with more than $500,000 in income at a 30% rate. This phasedown threshold also rises by 1% each year until 2029, before reverting back to the $10,000 cap in 2030.

Phaseouts for High-Income Taxpayers

High-income taxpayers face additional limits under the new law. The phaseout begins at $500,000 in modified adjusted gross income (MAGI) for joint filers, or $250,000 for those filing separately. For every $1 above that threshold, the deduction is reduced by 30 cents. However, the deduction can never drop below $10,000. For example, a couple earning $600,000 would see their deduction reduced by $30,000, leaving them with the minimum of $10,000.

What the SALT Deduction Doesn’t Cover

While the SALT tax deduction is broad, not all payments to a state or local government qualify. You can’t deduct federal income taxes, gift or estate taxes, or fees such as HOA dues and special property assessments. Professional license fees, certain utility charges, and most vehicle registration costs also don’t count. These exclusions often trip people up, so it’s worth double-checking before assuming something qualifies.

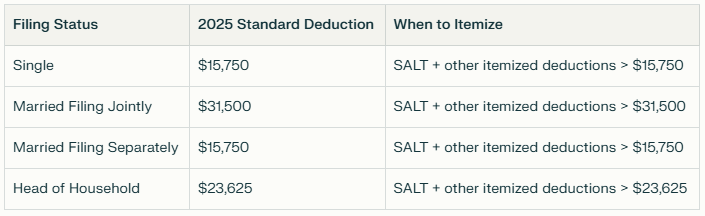

Should You Itemize or Take the Standard Deduction?

When deciding between the SALT deduction and the standard deduction, it comes down to simple math. The standard deduction for 2025 is projected to be $29,000 for married couples filing jointly. There are lower amounts for single filers and heads of households. If your itemized deductions, including SALT, mortgage interest, and charitable contributions, add up to more than the standard deduction, itemizing might lower your taxable income. Otherwise, the standard deduction is generally the better choice.

In fact, the SALT deduction was most common in high-tax states such as Maryland and Washington, D.C., where about 20% of taxpayers claimed it. In lower-tax states like Wyoming and South Dakota, only 5-6% of taxpayers itemized with SALT deductions. This shows why your location is an essential factor when making a decision.

Strategic Tax Planning Tips for Maximizing SALT Benefits

There are a few ways to make the most of the SALT deduction if you qualify. These strategies focus on timing, income management, and workarounds available to certain business owners.

Timing and Income Management

One way to maximize the deduction is by carefully timing your deductible payments. For example, you may plan when to make charitable contributions or pay mortgage interest. Prepaying state and local taxes, however, is not allowed under current law, so that option no longer exists. Another factor is your income. Keeping your MAGI below certain thresholds reduces the impact of phaseouts and preserves more of your deduction.

It’s also been shown that the $10,000 SALT cap introduced in 2018 had a sizable impact on home values. This highlights how tax rules influence broader financial decisions.

Pass-Through Entity Tax (PTET) Workarounds

For business owners, Pass-Through Entity Taxes (PTETs) are a valuable way to sidestep the SALT cap. The IRS approved these arrangements in Notice 2020-75, allowing certain state-level taxes on partnerships and S corporations to be deducted at the entity level instead of the individual level. This can restore some of the lost deduction capacity, particularly in high-tax states that have adopted PTET laws.

Remember, though, PTET rules vary by state, and certain specified service businesses (SSTBs) might face restrictions. If you own a pass-through entity, it’s worth reviewing your state’s rules to see if this option is available to you.

Future Outlook: What Happens After 2029?

Looking ahead, the current rules aren’t set in stone. The higher SALT caps under OBBBA will phase out by the end of 2029, and unless new legislation is passed, the deduction limit will drop back to $10,000 in 2030. This shift could dramatically change how many taxpayers itemize, especially in high-tax states.

Political debates around the SALT deduction are ongoing, and future adjustments remain uncertain. The best approach is to plan for the scheduled rollback but remain cognizant of any updates from Congress.

It’s projected that revenue losses from the SALT deduction will reach about $197 billion in 2027, more than eight times the projected losses in 2025. These numbers underscore why the deduction remains a hot topic in federal budget discussions.

Getting Ahead of the SALT Deduction

The SALT deduction continues to shift with new laws and income limits, so it pays to think ahead. Early planning has a significant impact on how much you save, so staying informed about upcoming changes, and reviewing your situation with a professional, will get you the most of what’s available.

FAQs

What is in the SALT deduction?

The SALT deduction covers three main types of state and local taxes:

- Property taxes on your home (and sometimes a second home)

- State and local income taxes, like those withheld from paychecks or paid quarterly

- Sales taxes — a good option if your state doesn’t charge income tax

You can only deduct one or the other — income tax or sales tax — not both.

Who benefits most from the SALT deduction?

Right now, the biggest benefits go to people in high-tax states like California, New York, and New Jersey — especially those with higher incomes and larger property tax bills. Before 2018, more middle- and upper-middle income earners used it, but the $10,000 cap changed that.

How much is the standard deduction for 2025?

For 2025, the standard deduction is projected to be $29,000 for married couples filing jointly. If you're single or head of household, the amount is lower. This number helps you decide whether it’s worth itemizing your deductions — including SALT.

Will the salt cap expire in 2025?

Not exactly. Starting in 2025, the cap increases to $40,000 for joint filers under the One Big Beautiful Bill Act. That’s a temporary change, though. Unless Congress steps in again, the cap will go back down to $10,000 in 2030.

What other itemized deductions are allowed in 2025?

If you itemize your taxes in 2025, you may also be able to deduct:

- Mortgage interest

- Charitable donations

- Medical expenses (if they’re high enough)

- Casualty or theft losses in certain cases

Adding these to your SALT deduction can help push your total over the standard deduction.

How does the SALT cap affect homeowners?

The cap limits how much property tax you can deduct, which can be a big deal in areas with high home values. Some research even found that home prices dropped after the $10,000 cap started in 2018 — especially in states with high taxes. It’s one way tax rules can affect the housing market.

Jack Fitzpatrick is originally from the East Coast and is now based in Scottsdale, Arizona. With 35 years in the finance industry, he developed a deep understanding of markets, risk management, and strategic financial planning. His career began as a foreign exchange trading executive at Morgan Stanley, followed by roles in portfolio management before transitioning into wealth advising. Today, as a fiduciary and member of Savvy Advisors, Jack leverages their platform of resources to provide comprehensive financial guidance tailored to my clients' unique needs.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy. All advisory services are offered through Savvy Advisors, Inc. (“Savvy Advisors”), an investment advisor registered with the Securities and Exchange Commission (“SEC”).

Works Cited