August 2025 Global Markets Recap

August Highlights

Markets posted modest gains in August amid a mix of tailwinds and headwinds. Solid earnings and resilient economic data supported risk assets, while sticky inflation, slowing job growth, and geopolitical frictions tempered sentiment. The S&P 500 logged its fourth straight monthly advance, the Nasdaq reached new milestones mid-month, and emerging markets drew renewed interest. Still, markets ended August on a cautious note as investors braced for the Fed’s September meeting.

Key Themes:

- Equity resilience against elevated inflation

- Rate-cut optimism fueled by employment weakness

- Tariff shifts and legal developments adding uncertainty

US Markets

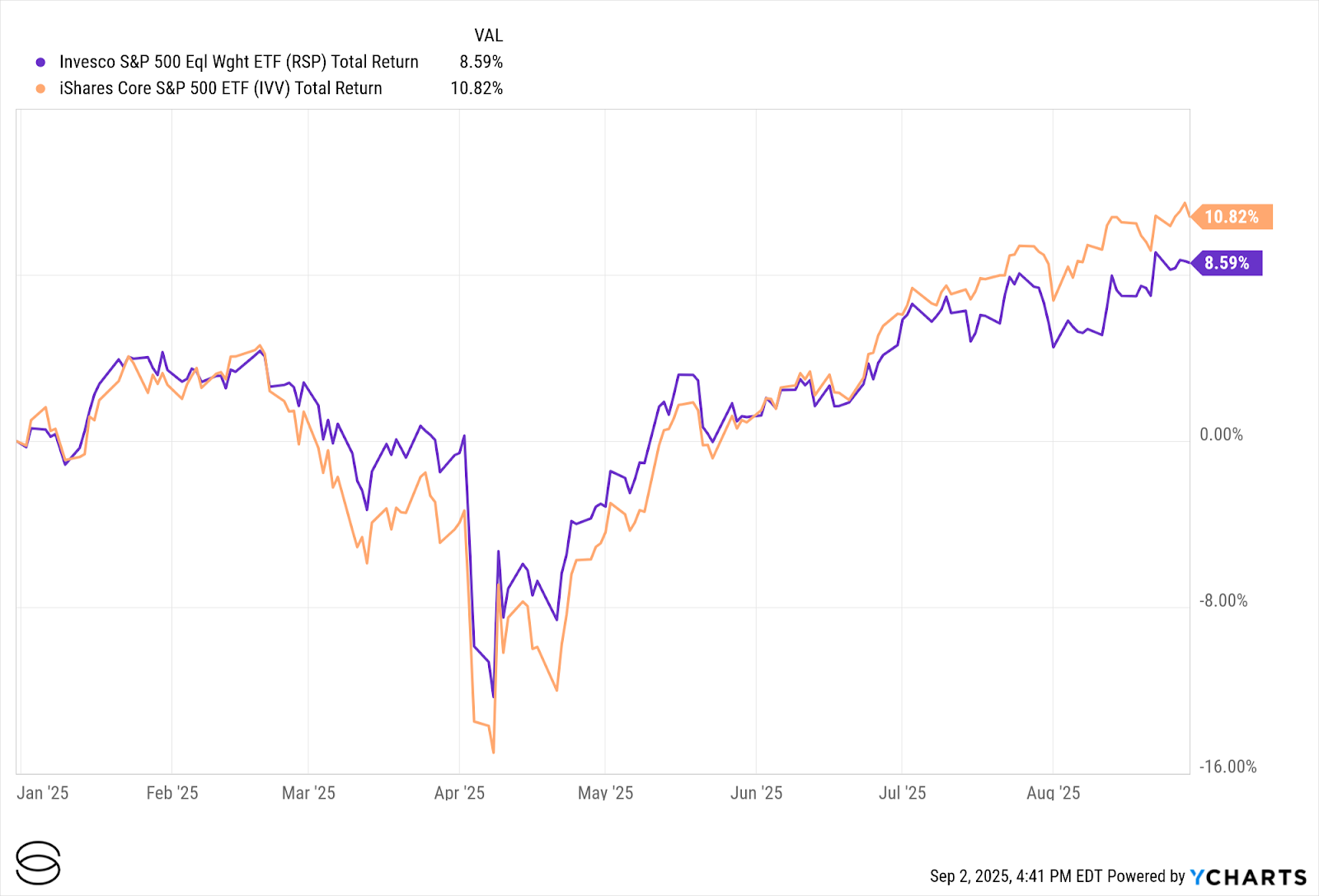

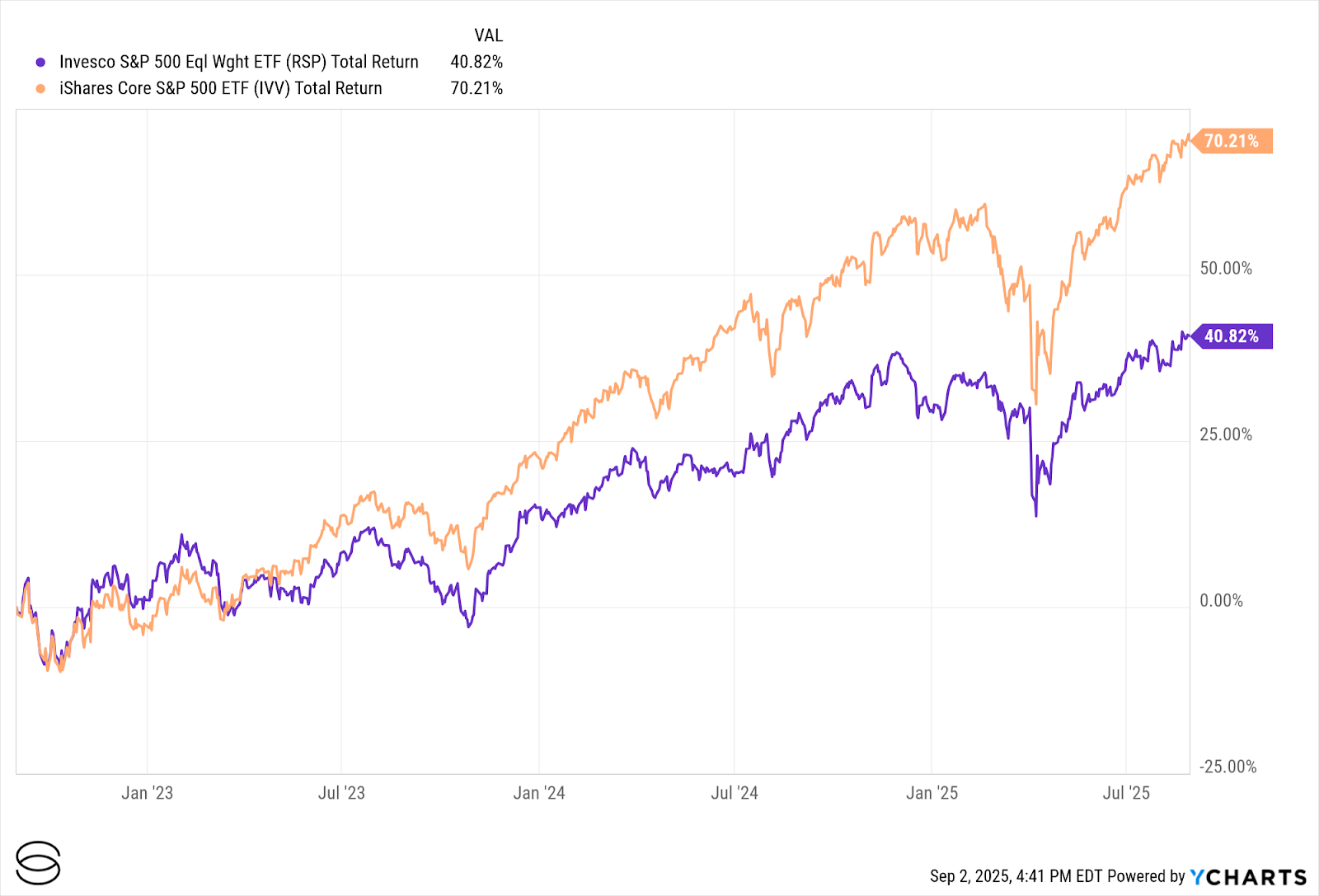

The S&P 500 gained 1.9% in August, closing at a record 6,501.86 on August 28th before slipping into mild profit-taking at month-end. Participation broadened beyond mega-cap leaders: the equal-weight S&P 500 rose roughly 2.7%, its best stretch of relative performance this year.

Broadening Market - S&P Equal Weight vs Cap-Weighted - ytd vs 3yr

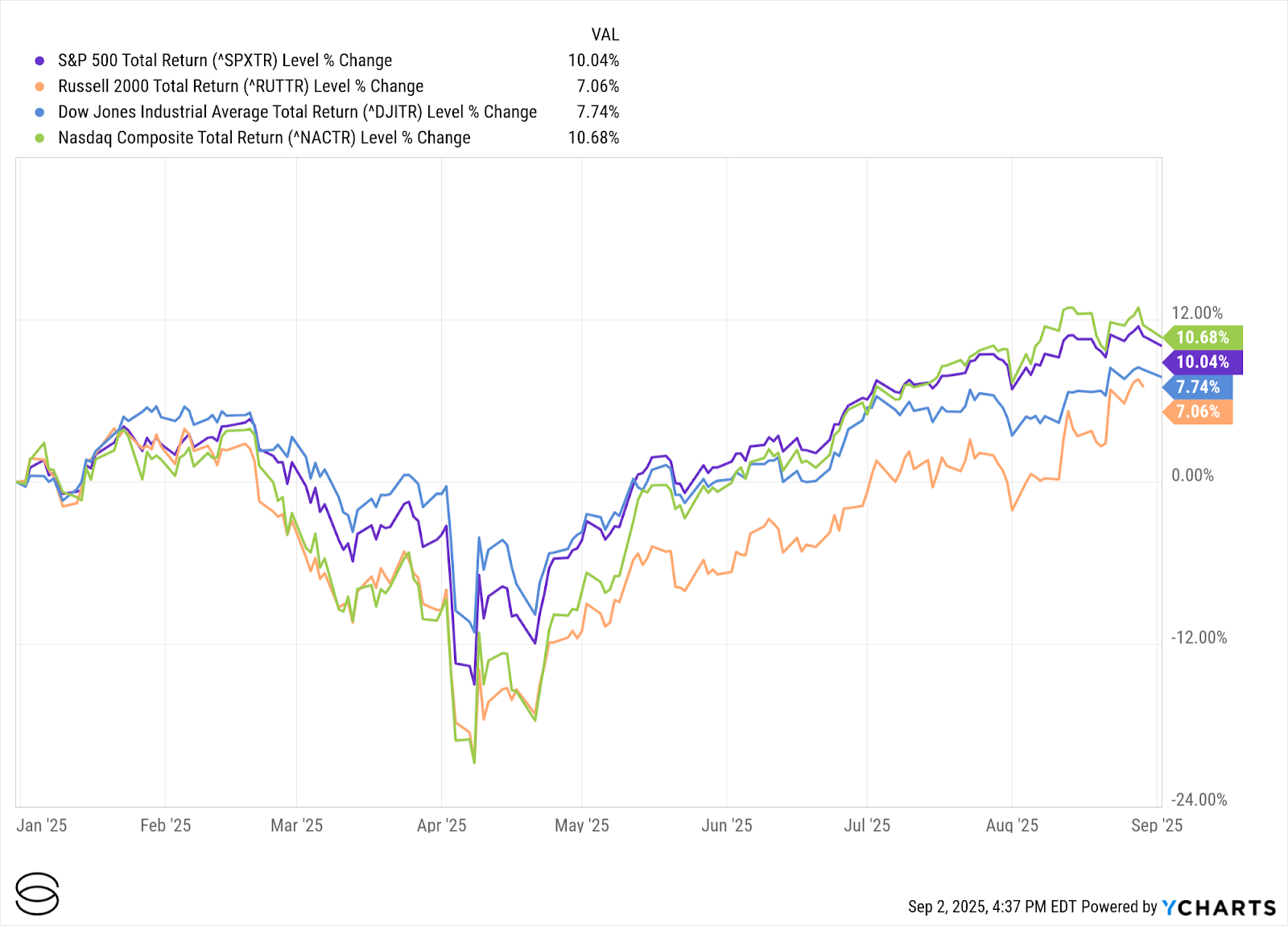

The Nasdaq Composite surged mid-month, reaching 21,681 on August 12th, supported by strength in technology and growth shares. Gains moderated late in the month as AI-related earnings disappointed. The Dow added about 1-2%, setting record closes on August 22nd and 28th before retreating slightly.

Despite these advances, the final week saw softer performance across the board: the S&P slipped 0.1%, the Nasdaq 0.2%, and the Dow 0.3%, as inflation concerns resurfaced.

Earnings Resilience

According to FactSet, nearly 81% of S&P 500 companies beat their EPS expectations during Q2 reporting season, well above the long-term average of ~66%. Revenue beats were more modest at ~60%, underscoring that earnings strength has been driven primarily by margin discipline rather than robust top-line growth. Companies have leaned on cost control, headcount management, and tighter capital spending to protect profitability. As a result, aggregate S&P 500 earnings grew about +12% year-over-year, with technology, communication services, and health care leading the way.

US Market Performance

Featured Theme: Record Highs and Rising Caution

August reminded investors that record highs can mask fragility beneath the surface. The S&P 500, Nasdaq, and Dow all set fresh milestones, underscoring the resilience of corporate earnings and the durability of investor appetite for growth. Yet under the hood, positioning and sentiment pointed to more caution than the headlines suggest.

Hedge funds reduced leverage and were net sellers through much of the month, reflecting unease about stretched valuations and seasonal risks. Volatility gauges such as the VIX stayed subdued, but history tells us September often delivers sharper swings. The late-month pullback in technology stocks - particularly AI-related names - highlighted how quickly leadership can wobble when expectations are high.

This divergence between market levels and investor behavior speaks to the tension driving September’s outlook: the tug of record-high equity benchmarks versus the gravity of slowing growth, sticky inflation, and looming policy decisions. For investors, the lesson is not to chase momentum blindly but to prepare for a more volatile path forward.

US Economy & Macro Snapshot

Inflation remained elevated. According to the Cleveland Fed’s Inflation Nowcast indicator, August CPI is tracking near 2.7% year-over-year, Core CPI at 3.0%, and Core PCE at 2.9%. Further, Flash PMI surveys for August showed the sharpest rise in input prices in three years, with firms passing on tariff-related costs to customers.

Inflation vs Fed Funds

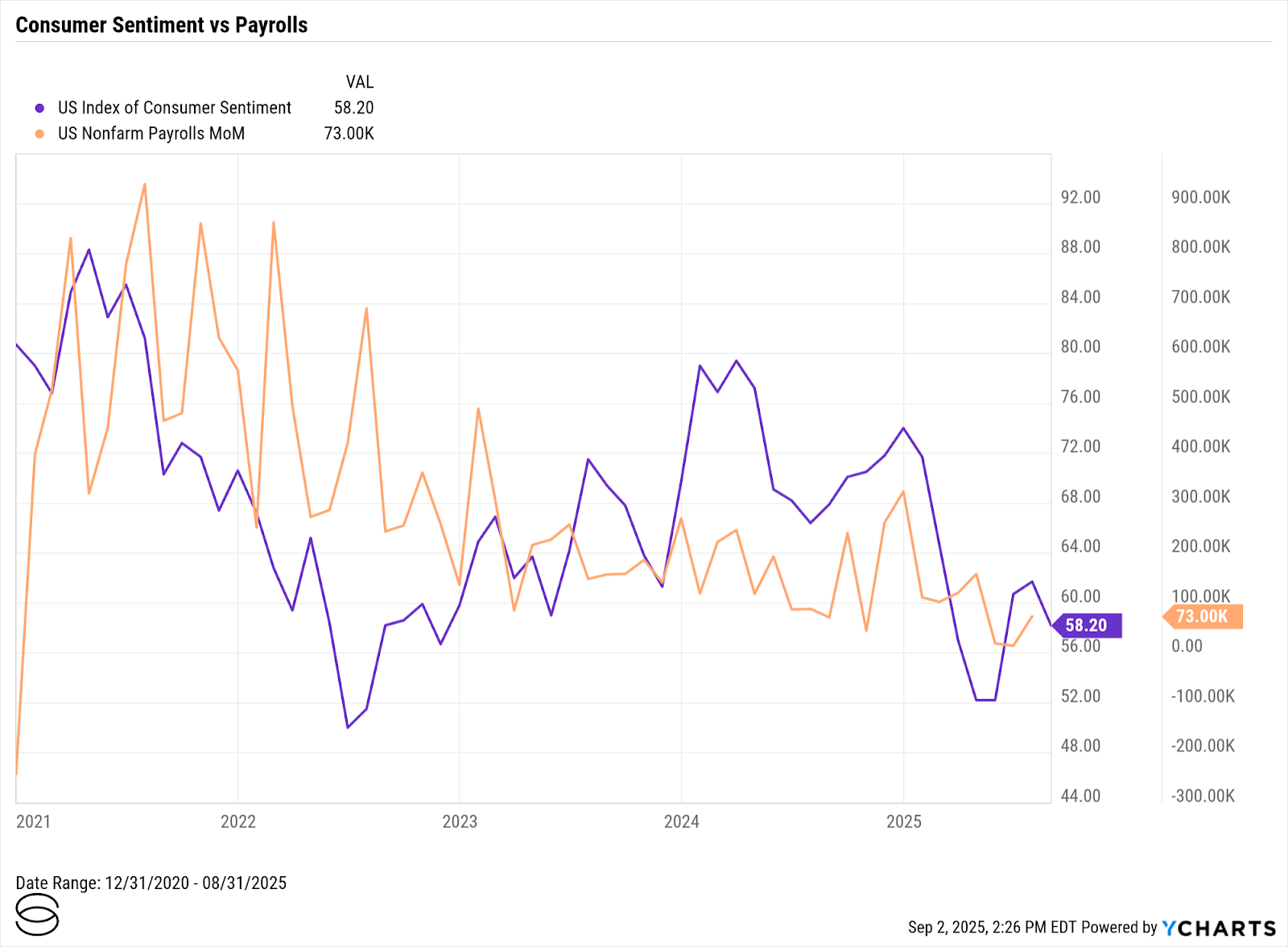

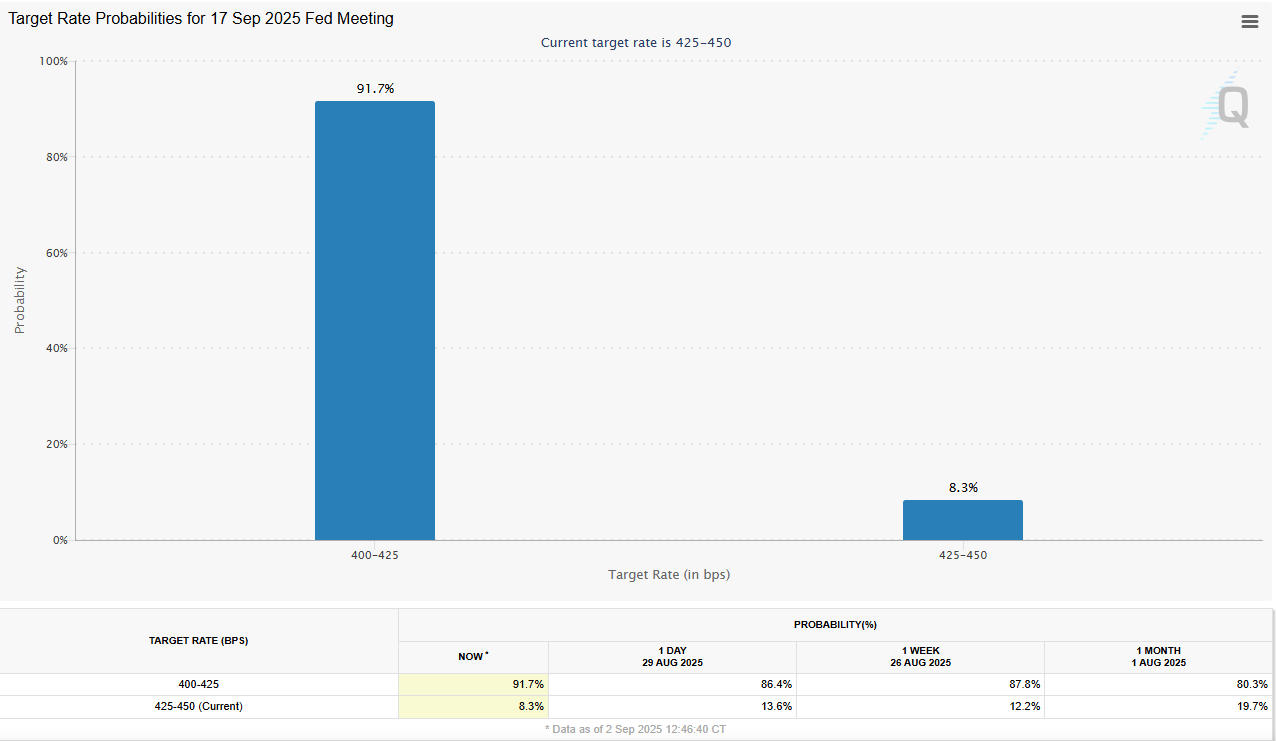

The University of Michigan’s Consumer Sentiment index fell to 58.2 from 61.7 in July, while inflation expectations rose to 4.8% (1-year) and 3.5% (longer-term). At the same time, the labor market softened further: job growth has averaged just 35,000 per month in recent months. These data have increased expectations for a September rate cut, though the Fed remains divided on timing.

Consumer Sentiment vs Payrolls

Trade & Tariff Developments

Tariff policy added another layer of complexity. The removal of the de minimis exemption took effect on August 29, broadening tariff coverage on consumer imports. Companies such as Procter & Gamble (P&G) plan to raise prices on roughly one-quarter of their U.S. product portfolios beginning in August 2025, with mid–single-digit increases on household staples like cleaning and personal care products. Legal challenges also mounted: a federal appeals court ruled that the administration exceeded its authority in imposing broad tariffs, though enforcement remains in place pending appeal.

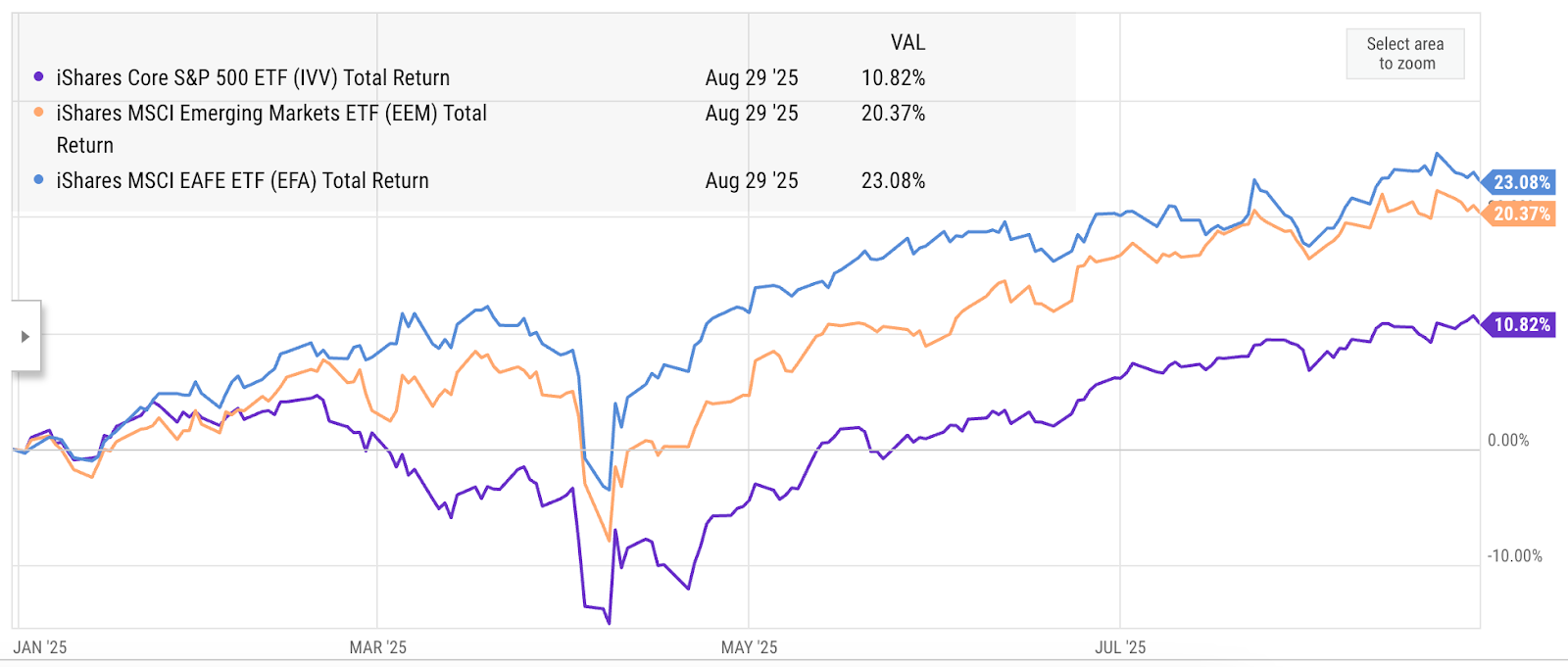

International Developed and Emerging Markets

In developed markets, the eurozone faced headwinds from softer PMI data and persistent weakness in Germany’s manufacturing sector. Japan’s equity market struggled under renewed yen strength, while political uncertainty in France and higher UK borrowing costs kept investors cautious.

Emerging markets outperformed, buoyed by renewed hedge-fund buying, especially in Chinese equities. India and Mexico also drew flows, with both economies showing resilience to U.S. tariff pressures. The MSCI All-Country World Index gained ~2.5%, while the Bloomberg Global Aggregate Bond Index added 1.5%.

Global Equity Outperformance YTD

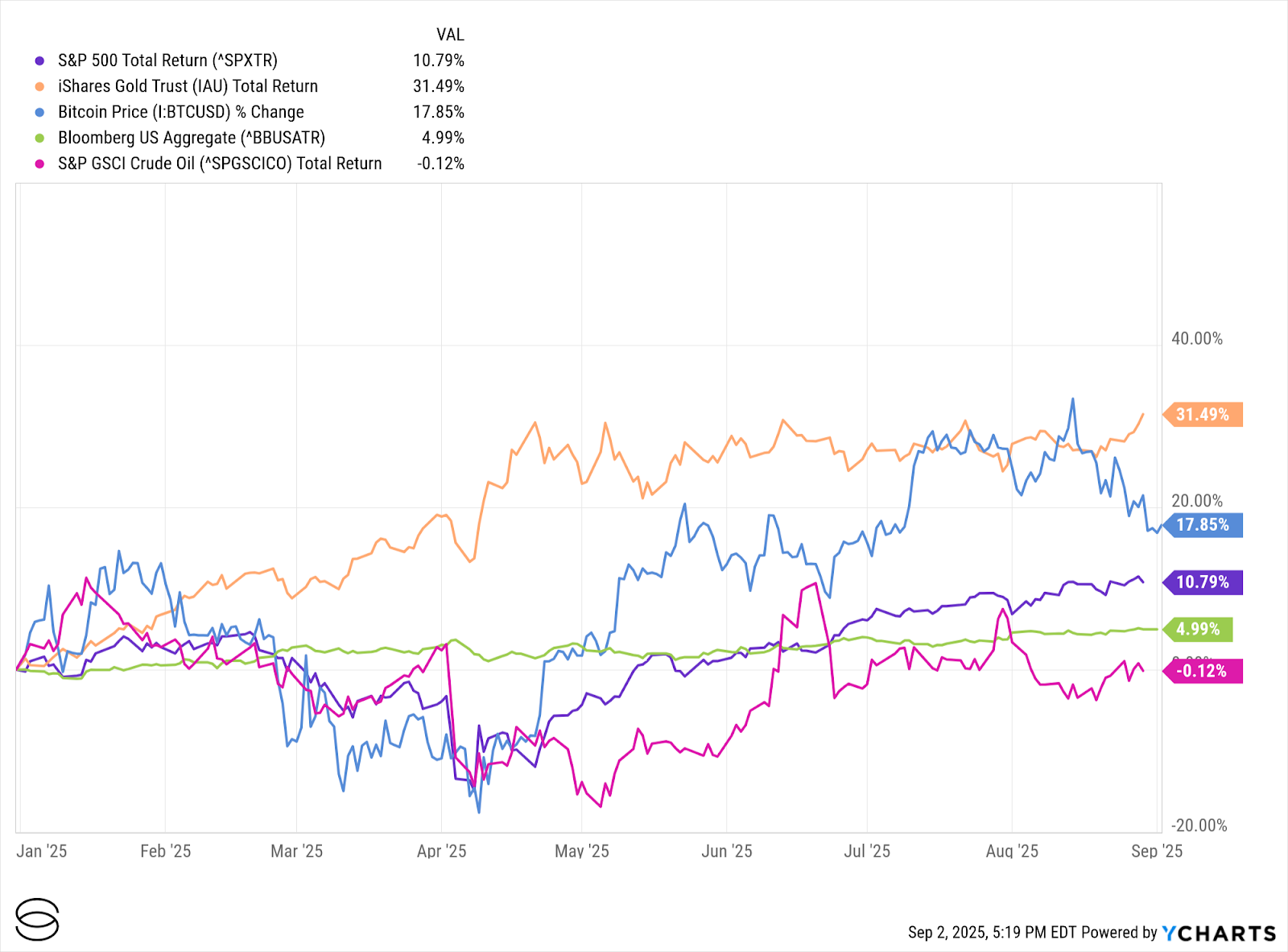

Fixed Income & Commodities

U.S. Treasury yields pulled back through August - with the 10-year note falling roughly 14 basis points to 4.22%, signaling market confidence in impending rate cuts. A steepening yield curve supported attractive returns, with around 88% of dollar bonds gaining (including 90% of investment-grade and 81% of high-yield issues) as risk appetite rose and rate-cut expectations firmed. Meanwhile, the Treasury maintained auction sizes but ramped up long-end buybacks to support liquidity. Abroad, sovereign yields in the UK and Japan trended higher, deepening cross-border spillover concerns. Overall, positioning became more cautious as hedge funds trimmed leverage and markets braced for heightened volatility.

Gold extended its rally to fresh highs, reflecting demand for safe havens amid questions around Fed independence and trade policy. Oil gained about 1.5%, while Bitcoin rebounded above $109,000.

Cross-Asset Class YTD Performance

What to Watch Next

Fed & Economic Releases

- Sept 5: August Jobs Report, including NFP, Unemployment, Earnings - critical for rate-cut odds.

- Sept 11: August CPI & Core CPI release - key for Fed’s inflation outlook.

- Sept 12: August PPI - upstream view of inflation pressures.

- Sept 16: Retail Sales - gauge of consumer strength.

- Sept 16-17: FOMC Meeting - potential first rate cut; tone and dot-plot guidance will set expectations.

- Sept 18-25: Housing Starts, Permits, and New Home Sales - important checks on rate-sensitive sectors.

- Sept 27: PCE & Core PCE - the Fed’s preferred inflation measure.

- Ongoing: Commentary and signals from Fed Governor Waller and other FOMC members.

Fiscal and Political Risk

- End of Sept: Risk of partial U.S. government shutdown if funding lapses.

- Ongoing: Heightened trade tensions with India, and repercussions in EM markets.

International Spotlight

- Sept 9: UN General Assembly opens amid geopolitical shifts.

- UK Sovereign Yields and fiscal reforms: UK gilt yields surged to multi-decade highs in late August, underscoring investor unease about inflation and debt sustainability.

- ECB & BOJ Signaling: The ECB (European Central Bank) strikes a more cautious tone on inflation persistence, while the BOJ (Bank of Japan) hints at more tolerance for rising yields. Both signaled that central banks are still navigating credibility tests in balancing growth, inflation, and political expectations.

Fed Cut Probabilities (Source CME FedWatch)

Together, these economic releases and political milestones will set the tone for September. With rate-cut expectations building, fiscal deadlines approaching, and geopolitical tensions simmering, markets may need to balance August’s resilience with the seasonal reality that September often brings greater volatility.

Mike has been in the wealth management industry for 10 years, beginning his career at BNY Mellon’s Silicon Valley office. There, he learned the intricacies of wealth management and discovered his passion for helping families achieve their financial goals. He later became a Portfolio Manager at an ultra-high net worth RIA in Boston, where he honed his skills in developing custom investment strategies for clients. Inspired by Savvy’s mission to bring a tech-focused energy to the wealth management industry, Mike joined the firm in July 2022 to drive the launch and continued evolution of their advisory capabilities. At Savvy, Mike has played a key role in developing, launching, and managing the in-house investment solution, Savvy Wealth Investment Management (“SWIM”). He also leads Savvy’s Client Experience Team, partnering closely with associates and advisors and aimed at producing best-in-class services for their clients. Mike is a graduate of Northeastern University and holds his Certified Financial Planner™ (CFP®) designation. He resides in New York with his wife, Alex, and their golden retriever, Bondi.

David Gao is an investment professional at Savvy with deep expertise in portfolio management and trading strategies. He graduated with honors from the University of Utah’s David Eccles School of Business, earning dual degrees in Finance and Economics. Before joining Savvy Wealth, David led trading operations exceeding $1 billion at Campbell Wealth Management, where he also designed and implemented an options covered call strategy. At United Capital Family Office, he played a key role in portfolio allocation, leveraging proprietary algorithms and advanced risk management techniques. He began his career at Goldman Sachs, where he built a strong foundation in investment research and analytics.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Inc. is a technology company. Savvy Advisors, Inc. is an SEC registered investment advisor. For purposes of this article, Savvy Wealth and Savvy Advisors together are referred to as “Savvy”. All advisory services are offered through Savvy Advisors, while technology is offered through Savvy Wealth. The views and opinions expressed herein are those of the speakers and authors, and do not necessarily reflect the views or positions of Savvy Advisors.

Sources:

1 FactSet Earnings Insight – Q2 2025 (week of August 30, 2025)

2 Hedge funds still cautious on U.S. stocks going into fragile September | Reuters

3 University of Michigan, Survey of Consumers (August 2025 release)

4 August 2025: 88% of Dollar Bonds Rally as Yields Drop Amid Rate Cut Bets