A Risk-Off February: Policy and AI Crosscurrents Force a Rotation

February brought a distinct change in weather for global markets. If January was defined by "constructive differentiation," February felt more like a comprehensive risk audit. The optimism that carried us into the new year met a sobering reality as investors began to re-price policy uncertainty, a non-linear inflation path, and the mounting "winners and losers" narrative surrounding AI adoption.

The headline numbers in U.S. equities - a modest 0.9% dip for the S&P 500 - don't tell the full story. Beneath the surface, the internal signal was loud and clear: capital aggressively rotated away from duration-sensitive growth and into the safety of defensives and real assets. The month was shaped not by a single data point, but by the convergence of three heavy themes: renewed trade friction following a landmark Supreme Court ruling, late-month geopolitical friction in the Middle East, and a deepening debate over how AI will structurally disrupt labor and profit pools.

Noteworthy Developments: Shifting Risk Premiums

The repricing we saw in February wasn't a binary event; it was a slow burn catalyzed by several overlapping developments.

- Trade Policy Volatility: A major legal setback at the U.S. Supreme Court regarding tariff authority triggered a fast-moving attempt by the administration to reconfigure trade measures. This created a cloud of uncertainty for corporate planners trying to handicap inflation pass-through and potential global retaliation.

- The AI "Creative Destruction" Narrative: AI evolved from a simple productivity story into a macro "shocker." We saw genuine anxiety around which firms might be structurally displaced or margin-compressed by these tools, putting heavy pressure on software and payment names. While AI-hardware remained the market’s gravity center, other firms provided vivid signals of change through workforce actions explicitly framed around AI-driven efficiency.

- Geopolitical and Policy Static: Intensifying U.S.–Iran tensions late in the month lifted oil and reminded investors why traditional hedges matter. Simultaneously, the Fed remained "steady but sensitive." Officials consistently preached patience, leaving the market to wonder if tariff-related inflation persistence might delay the next leg of the easing cycle.

U.S. Equities: Defensive Leadership and Valuation Scrutiny

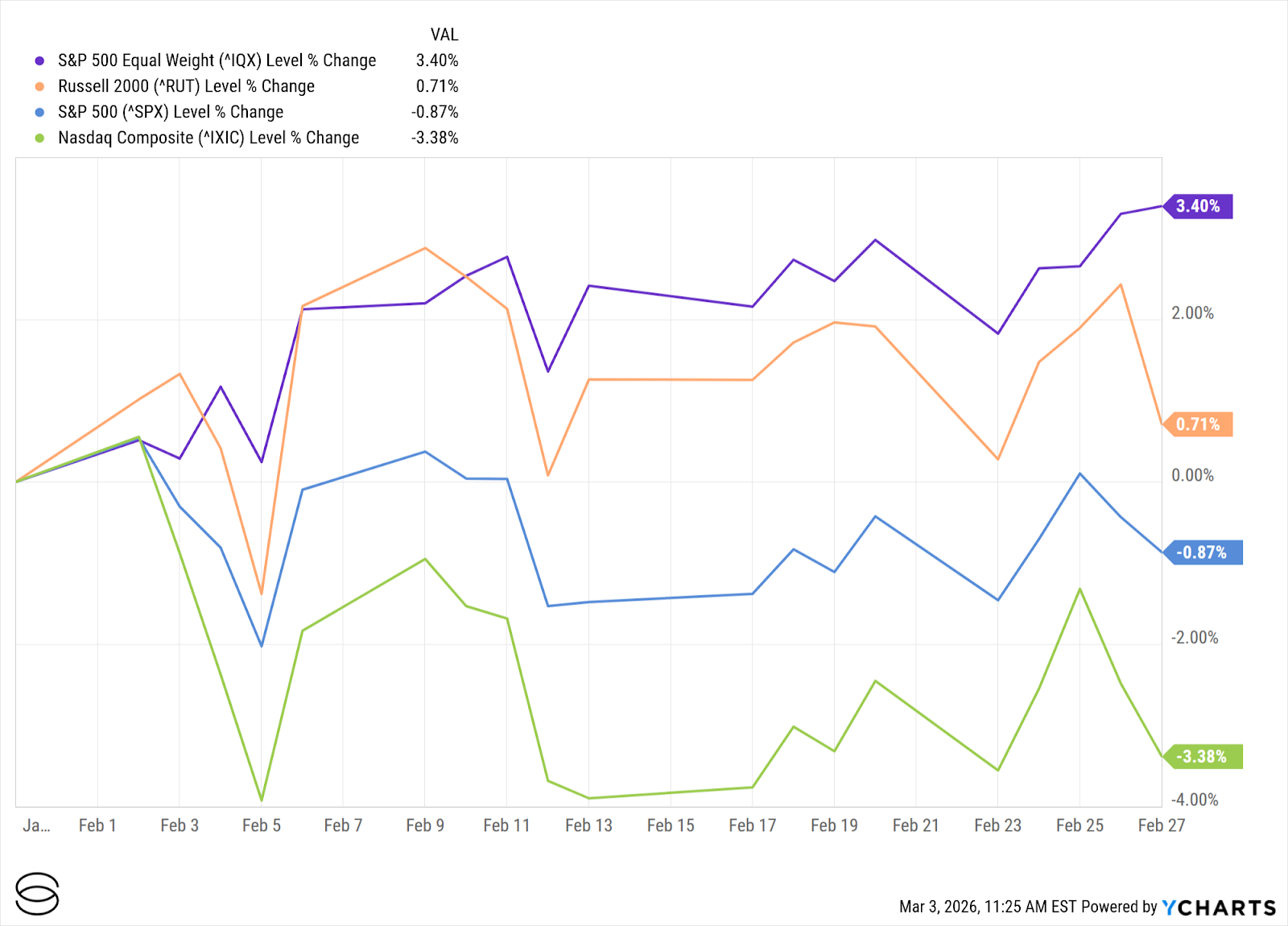

February’s tape was a study in divergence. The Nasdaq Composite was the clear laggard, sliding 3.4% as the market grew less tolerant of "growth at any price". Conversely, Small-caps showed surprising resilience; the Russell 2000 actually managed a +0.7% gain, even with late-month volatility.

Exhibit 1: U.S. Equity Performance (February 2026)

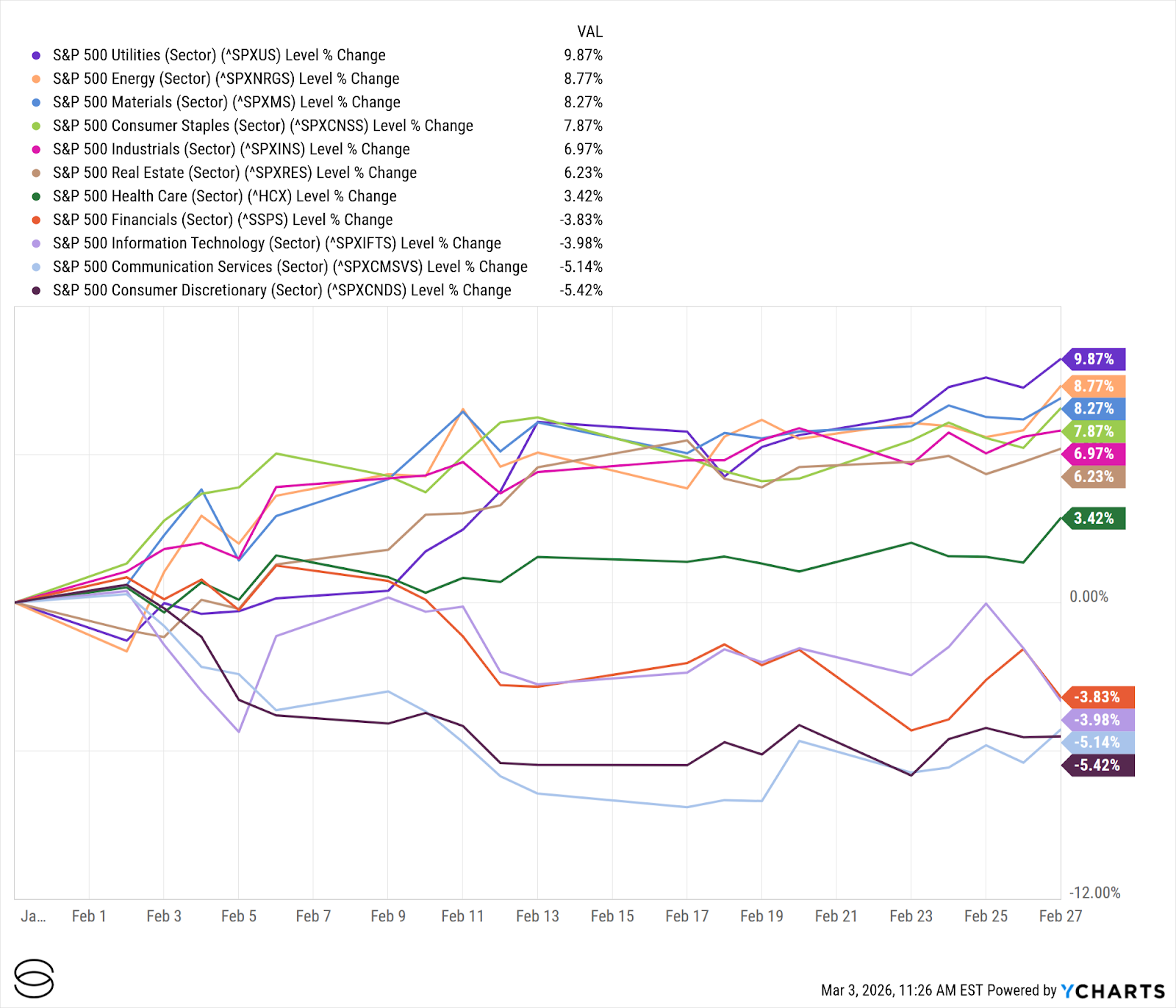

Sector performance told the most honest story. Leadership skewed heavily toward inflation hedges and defensives:

- Winners: Utilities (+9.9%), Energy (+8.8%), and Consumer Staples (+7.9%) led the way.

- Laggards: Technology (-4.0%), Communication Services (-5.1%), and Consumer Discretionary (-5.4%) felt the brunt of the "risk audit" .

Exhibit 2: U.S. GICS Sector Performance (February 2026)

This rotation aligns perfectly with the month’s dominant drivers: tariff fears (favoring pricing power), geopolitical risk (supporting oil), and AI-related anxiety weighing on platforms that have yet to prove their moat against new tools.

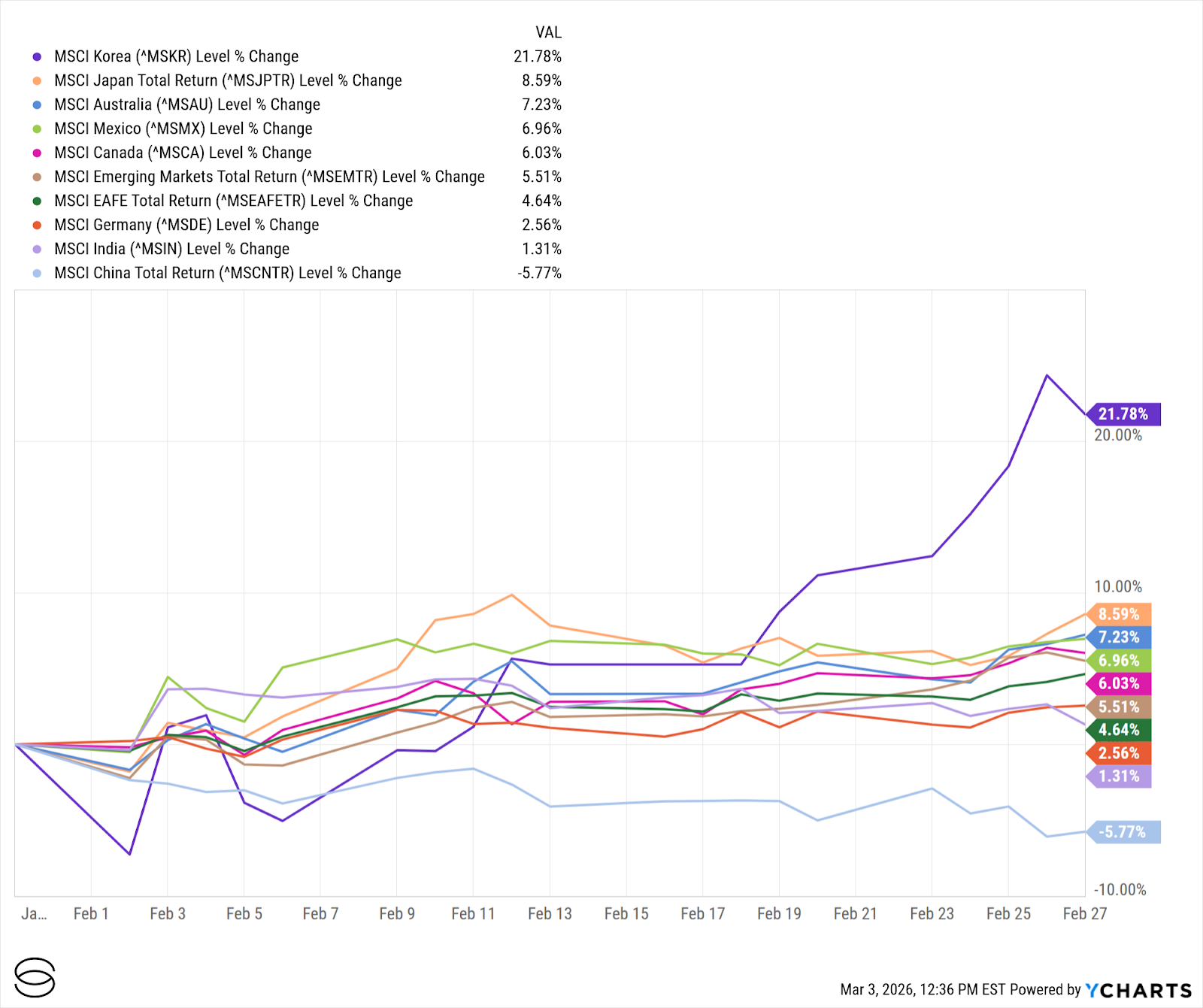

International Markets: A Case for Diversification

Outside the U.S., the tone was surprisingly firmer. Both MSCI EAFE and MSCI Emerging Markets rose 4.6% and 5.5%, respectively. This relative outperformance is a reminder of the value of diversification; these benchmarks benefited from a different sector mix that lacked the high concentration of U.S. mega-cap tech - the very area under the most scrutiny this month. However, the "tariff channel" remains a two-sided risk. Global markets are currently handicapping second-order effects in currency and supply chains, particularly if producer prices begin to reflect new trade frictions.

Exhibit 3: International Equities Performance (February 2026)

Fixed Income and Commodities: The Safe-Haven Bid

Bond markets offered a more definitive signal than equities in February, as the Treasury curve responded to a more complex global backdrop. The 10-year yield fell nearly 30 bps to 3.97%, while the 2-year dropped 15 bps. While domestic data played a role, this move could have also been a reflection of investors taking risk off the table against an increasingly tense geopolitical climate - specifically the friction in the Middle East.

In credit, spreads widened as this cautious mood took hold. The ICE BofA U.S. High Yield spread moved to 3.12%, signaling a more measured appetite compared to the optimistic "everything rally" that characterized late 2025. Commodities responded most directly to these headlines; Crude Oil was the month’s standout, buoyed by the U.S.–Iran tensions, which in turn reinforced the robust outperformance we saw in the Energy equity sector.

Exhibit 4: Cross-Asset Performance (February 2026)

Economy and Policy: A "High-Information" March Ahead

The data releases in February reinforced a "cooling, but not cool enough" narrative. January payrolls came in at 130,000, while the unemployment rate held at 4.3%. Wage growth remained firm at 3.7% YoY, which is exactly the kind of "sticky" data that keeps the FOMC cautious.

Inflation is moving in the right direction (CPI at +2.4% YoY), but it's not a straight line. The stronger-than-expected PPI reading at month-end raised concerns about the "tariff pipeline," an important nuance for the Fed given the linkage to forthcoming PCE measures. Meanwhile, growth showed signs of softening, with Q4 GDP revised to 1.4% (impacted by the U.S. Government shutdown in late 2025).

Key Dates to Watch in March 2026

- March 6: February Employment Situation Report

- March 11: February CPI Inflation Data

- March 13: February PCE Inflation (The Fed's preferred gauge)

- March 17–18: Federal Reserve Policy Meeting (FOMC)

The Bottom Line

February moved us from January’s “constructive differentiation” into a more defensive, policy-sensitive phase. The convergence of trade policy volatility, AI-driven valuation scrutiny, and late-month geopolitical friction forced a pivot toward balance-sheet durability and real-asset resilience.

March is shaping up to be a high-information month. The upcoming labor and inflation prints, coupled with the evolving U.S.–Iran situation, will likely determine whether February’s risk-off move was a tactical pause or a more durable regime shift for 2026. Investors will be watching closely to see if geopolitical risk premia remain embedded in energy prices or if a de-escalation allows for a return to the fundamental "differentiation" seen at the start of the year.

Anshul Sharma is Chief Investment Officer at Savvy Wealth, where he oversees the firm’s investment strategy, portfolio design, and platform innovation. He partners across product, marketing, and operations teams to deliver portfolios that take a methodological approach to balance customization with scalability for advisors and their clients. Before joining Savvy, Anshul spent nearly two decades at Bank of America, where he managed the Chief Investment Office’s Sustainable Model Portfolio Suite, launched new proprietary offerings, and, as Head of Alternative Investment Strategy, provided guidance and thought leadership to advisors around hedge fund, private market, and real asset strategies. He began his career as an Investment Strategist at U.S. Trust, designing multi-asset portfolios for high-net-worth and institutional clients. Anshul holds a Master of Financial Engineering from UC Berkeley and a Bachelor of Computer Engineering from Lehigh University. Outside of work, he is an avid tennis player, enjoys time with his wife, two sons, and their Bernedoodle, and is an auto enthusiast who loves cooking and travel.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Inc. is a technology company. Savvy Advisors, Inc. is an SEC registered investment advisor. For purposes of this article, Savvy Wealth and Savvy Advisors together are referred to as “Savvy”. All advisory services are offered through Savvy Advisors, while technology is offered through Savvy Wealth. The views and opinions expressed herein are those of the speakers and authors, and do not necessarily reflect the views or positions of Savvy Advisors.