Financial Planning in Your 20s: Building Wealth & Strong Financial Habits

Setting financial goals early influences how you handle money for years. While it may seem like you have time to figure things out, your 20s are one of the best times to establish good habits and make your money work for you. Starting early with financial planning creates a foundation that can significantly impact your long-term wealth.

In this article, we outline seven key steps for building financial security in your twenties:

- Define SMART financial goals that are specific, measurable, achievable, relevant, and time-bound

- Create a personalized budget that fits your lifestyle, potentially using the 50/30/20 rule as a starting point

- Build an emergency fund of 3-6 months of expenses, starting with $500-1,000

- Begin investing early, even with small amounts ($50-100 monthly), to maximize compound growth

- Manage debt strategically by prioritizing high-interest debt and building credit responsibly

- Start retirement savings now by contributing at least 5-15% of income to retirement accounts

- Prepare for major life milestones like home ownership and career advancement

The Power of Starting Early: Why Your 20s Matter for Building Wealth

Your 20s provide the longest possible runway for wealth accumulation. The earlier you begin your financial journey, the more significant the results, thanks to the unmatched power of time and compound interest.

The financial habits you establish now, such as budgeting consistently, saving strategically, and investing wisely, tend to become lifelong practices. However, many young adults are still working toward full financial stability, with only 44% of people aged 25-29 reporting complete financial independence. This number increases to 67% by ages 30-34, showing that independence is a gradual process for most.

Meanwhile, approximately 26% of young adults carry credit card debt, with average balances around $2,100, highlighting the importance of developing solid financial habits early.

Step 1: Define SMART Financial Goals That Drive Your Journey

Before diving into budgeting or investment strategies, clarify your financial goals. Effective financial planning begins with understanding what you're working toward, whether short-term objectives (saving for a vacation), mid-term goals (purchasing a vehicle), or long-term aspirations (retirement security).

The SMART goal framework provides structure to your financial planning process:

- Specific: Define exactly what you want to achieve (e.g., "Save $5,000 for a down payment")

- Measurable: Track progress with concrete numbers

- Achievable: Set realistic targets given your current income and expenses

- Relevant: Ensure goals align with your values and priorities

- Time-bound: Establish clear deadlines

Document your goals, review them quarterly, and adjust as your life circumstances evolve. Having well-defined objectives gives your money purpose and strengthens your commitment to financial discipline through purposeful financial planning.

Step 2: Create a Personalized Budget System That Actually Works

Contrary to popular belief, budgeting in your 20s isn't about restriction but intentionality and awareness. Understanding your cash flow patterns empowers you to direct your money toward what matters most. With today's rising costs of living, effective budgeting has become even more crucial for young adults.

Housing expenses have increased disproportionately to income growth, with rent and home prices outpacing earnings in most regions. This economic reality makes strategic budgeting more essential than ever before.

Budgeting Approaches for Different Financial Styles

The widely-recommended 50/30/20 rule provides a simple framework:

- 50% allocated to needs (housing, utilities, groceries, transportation)

- 30% for wants (entertainment, dining out, non-essential shopping)

- 20% toward savings and debt repayment

However, this structure may not suit everyone's circumstances. If you have irregular income or high fixed expenses in expensive metropolitan areas, consider zero-based budgeting (assigning every dollar a specific purpose) for greater precision. Those who prioritize flexibility might prefer value-based budgeting, which aligns spending with personal priorities while maintaining overall financial balance.

Regardless of your approach, the fundamental goal remains consistent: gain clarity about your money flow to make informed adjustments without guesswork.

Budgeting Tools and Apps Worth Checking Out

Modern budgeting apps simplify financial management for on-the-go young professionals:

- You Need a Budget (YNAB): Excellent for zero-based budgeting with powerful forecasting features, though it requires an initial learning investment

- Mint: Free comprehensive solution with automatic categorization, though customer support options are limited

- EveryDollar: Intuitive interface built around the envelope budgeting methodology

- PocketGuard: Particularly strong for tracking spending patterns and flagging potential overspending

Federal resources like MyMoney.gov offer free tools and educational materials for everyday financial management as part of your broader financial planning strategy.

Step 3: Build a Robust Emergency Fund for Financial Security

Establishing an emergency fund is a cornerstone of financial security in your 20s. This dedicated safety net prevents unexpected expenses from derailing your broader financial goals or forcing you into high-interest debt.

Begin with a starter fund, about $500 to $1,000, then work toward saving 3 to 6 months of basic expenses. Think rent, groceries, transportation, and bills. Set up automatic transfers of 5-10% from each paycheck to your emergency fund until you reach your target.

Keep this money in accounts offering both liquidity and modest returns, such as high-yield savings accounts (currently offering 3-5% APY), money market accounts, or short-term CDs (Certificate of Deposit). Having this safety net is foundational to any comprehensive financial plan.

According to Federal Reserve data, only 36% of young adults have sufficient emergency savings to cover three months of expenses. This vulnerability highlights why building this financial buffer should be prioritized early in your wealth-building journey.

Step 4: Begin Investing Strategically, Even With Limited Resources

You don't need thousands of dollars to begin. In fact, the earlier you start investing, the more time your money has to grow. Even $50-100 monthly can build substantial wealth over decades. Below, we'll cover beginner-friendly investment approaches and show how even small amounts make a sizable impact over time.

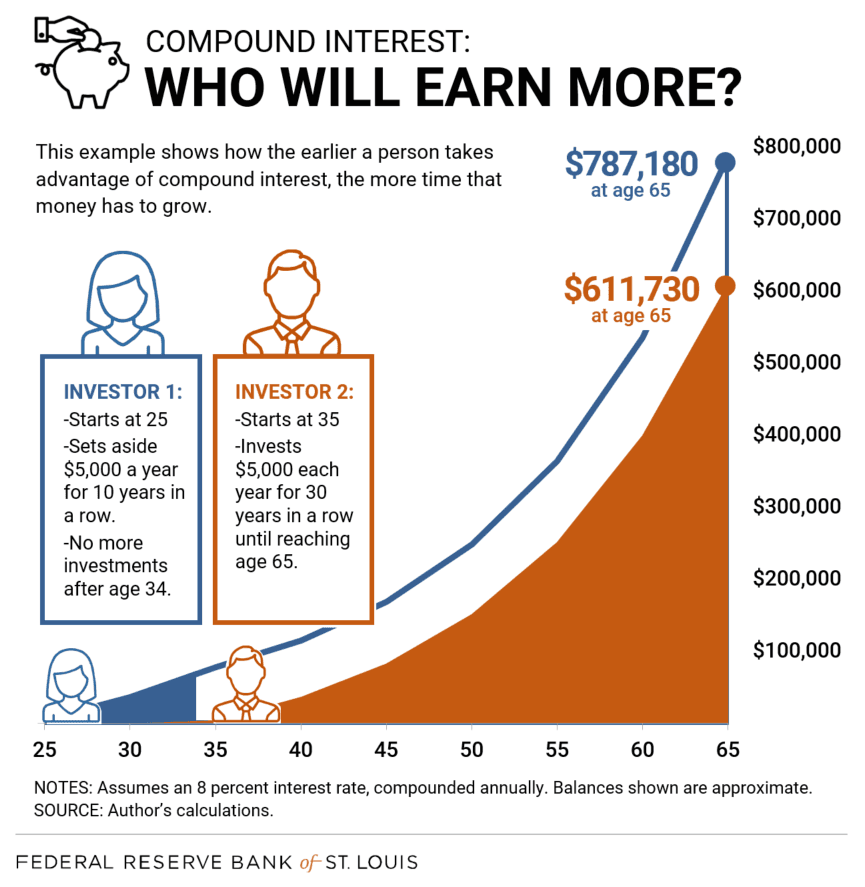

The Exponential Power of Compound Interest

Compound interest rewards time in the market more than initial investment size. When you establish investment habits early, your returns generate their own returns, creating powerful exponential growth.

Consider this compelling illustration: with an 8% interest rate, investing just $5,000 a year at age 25 and stopping at age 35, you’d have $787,000 by age 65. Delay that same investment strategy until 35, you’d have to invest $5,000 annually for the next 30 years to reach $612,000 by 65.

This mathematical reality demonstrates why even modest investments during your 20s can significantly outperform larger contributions started later. Time truly becomes your most valuable investment asset.

Beginner-Friendly Investment Vehicles

Several account types make entering the investment landscape accessible for those just starting their financial journey:

- 401(k): If your employer offers a matching contribution, prioritize this option first, as it represents immediate, guaranteed returns on your investment

- Roth IRA: Ideal for long-term growth potential, especially beneficial if you're currently in a lower tax bracket than you expect to be during retirement

- Traditional IRA: Offers potential tax advantages now, with taxes applied to withdrawals during retirement

- Brokerage Account: Provides flexibility for goals outside traditional retirement timelines, such as travel funds or home down payments

Each account type supports different investment strategies aligned with your specific time horizons and financial objectives. Remember that simply beginning the investment process often represents the most significant hurdle to overcome.

Step 5: Implement Strategic Debt Management

Not all debts carry equal weight in your financial picture. Developing a nuanced approach to debt management shapes your long-term financial health. Whether managing student loans, credit card balances, or both, a structured plan prevents overwhelm and accelerates progress.

Here's a strategic framework for tackling your debt effectively.

What to Pay Off First: Credit Cards or Student Loans?

Credit card debt typically comes with much higher interest rates than student loans. On average, federal student loan rates are around 6.53%, while credit card APRs (Annual Percentage Rate) average 24.35%. That difference adds up quickly.

For most individuals, the mathematically optimal approach (the "avalanche method") focuses on eliminating the highest-interest debt first while maintaining minimum payments on other obligations. For those motivated by psychological wins, the "snowball method" targets the smallest balances first, then redirects those payments toward larger debts as each is eliminated.

While no single approach works universally, the key is committing to a consistent strategy that aligns with your personal motivation style and financial situation.

Building Credit Strategically in Your 20s

Your credit history significantly impacts your financial opportunities, and your 20s represent the ideal time to establish strong credit foundations. A robust credit profile facilitates rental applications, loan approvals, and even certain employment opportunities.

Focus on these key credit-building principles:

- Maintain low credit utilization (ideally below 30% of available credit)

- Establish perfect payment history by never missing due dates

- Regularly monitor your credit reports for accuracy

- Diversify your credit mix gradually over time

If you're new to credit, consider secured credit cards or becoming an authorized user on a responsible family member's account as entry points. Additionally, monitor your debt-to-income ratio (DTI), as lenders use this metric to evaluate your ability to manage additional credit obligations.

Step 6: Establish Retirement Savings Habits Early

While retirement may seem distant during your 20s, beginning retirement planning now creates tremendous financial advantages. Early contributions benefit from decades of potential growth, allowing you to build substantial retirement assets without requiring aggressive saving rates later in life.

Below we examine appropriate contribution targets and account selection strategies for early-career professionals.

How Much Should You Be Saving?

In your 20s, even small amounts add up. A common rule of thumb is to save at least 15% of your income toward retirement. If that's not doable yet, start with as little as 5% and gradually increase by 1-2% annually until you reach your target.

Prioritize employer-sponsored retirement plans that offer matching contributions, effectively providing immediate returns on your investment. Once you've maximized any available match, consider supplementing with individual retirement accounts that offer tax advantages aligned with your current financial situation and future expectations.

Roth IRA vs. 401(k): What’s the Difference?

Both Roth IRAs and 401(k) plans offer valuable but distinct benefits for retirement savers.

Employer-sponsored 401(k) plans allow pre-tax contributions, reducing your current taxable income while deferring taxes until withdrawal. The higher contribution limits ($22,500 in 2023) and potential employer matching make these powerful wealth-building tools.

Roth IRAs, funded with after-tax dollars, offer tax-free growth and qualified withdrawals in retirement. With income eligibility requirements and lower contribution limits ($6,500 in 2023), these accounts are particularly advantageous for early-career professionals expecting income growth over time.

Early in your career when you're likely in a lower tax bracket, Roth accounts often provide optimal long-term tax efficiency. As your income increases, diversifying across both pre-tax and after-tax retirement vehicles creates valuable tax flexibility for your future self.

Read our guide to IRAs vs. 401(k)s for more information.

Step 7: Prepare Strategically for Major Life Milestones

Your 20s provide the perfect opportunity to begin planning for significant life transitions, whether purchasing property, changing careers, or merging finances with a partner. Proactive planning for these milestones reduces financial stress and expands your options when these moments arrive.

For prospective homebuyers, begin systematically building your down payment fund. While 20% down payments avoid private mortgage insurance (PMI), many first-time buyer programs require substantially lower amounts. Nevertheless, larger down payments reduce monthly obligations and total interest paid over the life of your mortgage.

If you're unsure about your housing timeline, utilize rent-versus-buy calculators to analyze whether homeownership aligns with your current financial situation and lifestyle preferences. This analysis should incorporate not just monthly payment comparisons but also opportunity costs, maintenance responsibilities, and potential appreciation scenarios.

Common Financial Pitfalls to Avoid in Your 20s

Even well-intentioned individuals can unknowingly undermine their financial progress through common oversights. Awareness of these potential missteps helps you navigate your financial journey more effectively.

Lifestyle inflation, increasing spending proportionately with income growth, represents one of the most significant barriers to wealth accumulation. Instead, direct your new income toward savings and investments to accelerate your financial progress.

Other common pitfalls include:

- Excessive discretionary spending without budgetary guardrails

- Neglecting retirement contributions during early earning years

- Maintaining insufficient emergency reserves

- Overreliance on credit cards for lifestyle maintenance

- Making emotional investment decisions rather than following a strategic plan

Recognizing these potential traps allows you to implement preventive measures that protect your financial foundation and support long-term financial planning objectives.

Financial Milestones to Target by Age

While financial journeys vary considerably, establishing age-based benchmarks provides a helpful orientation for your progress. These milestones represent general guidelines rather than rigid requirements.

By age 25, aim to establish:

- A functioning budget system that works with your lifestyle

- An initial emergency fund covering at least one month of expenses

- Active participation in employer retirement plans (if available)

- A credit score above 700

By age 27-28, work toward:

- Consistent retirement contributions of at least 10% of income

- A structured debt repayment plan with high-interest debt eliminated

- An emergency fund covering 3+ months of expenses

- Specific savings for medium-term goals

By age 30, consider targeting:

- Retirement savings equivalent to one year's salary

- Defined investment strategy beyond retirement accounts

- Substantial progress toward major financial goals (home down payment, etc.)

- Comprehensive insurance coverage (health, disability, life if needed)

For context, Bureau of Labor Statistics data indicates median weekly earnings of $784 for workers aged 20-24 and $1,136 for those 25-34, providing benchmarks against which to measure your income progression.

Tools That Make Managing Money Easier

Digital resources simplify financial management for young adults navigating increasingly complex financial landscapes. These tools reduce friction in maintaining good financial habits and provide valuable insights for decision-making.

For comprehensive budgeting and expense tracking, applications like YNAB, Mint, and EveryDollar offer automated categorization and progress visualization. Credit monitoring services such as Credit Karma, Experian, or those provided by your financial institution help you track your credit development and identify improvement opportunities.

Additionally, explore financial calculators for specific planning scenarios (retirement projections, loan amortization, etc.) and consider participating in free online personal finance courses to expand your financial literacy through platforms like Khan Academy or Coursera.

Developing a Personalized Financial Strategy

Financial management shouldn't feel overwhelming. By systematically implementing focused improvements, you can build a robust financial foundation that supports current lifestyle needs and future aspirations. Identify your highest-priority financial area (saving, investing, debt management, or retirement planning) and direct your initial attention there.

Remember that financial progress isn't linear; adaptability and consistency matter more than perfection. As your income, goals, and life circumstances evolve, regularly revisit your financial strategy to ensure continued alignment with your priorities.

The habits and decisions you establish during your 20s create powerful momentum that compounds throughout your lifetime, making this decade particularly influential in shaping your long-term financial trajectory.

Key Takeaways:

- Your 20s are the best time to start financial planning

- Small steps now can lead to long-term financial independence

- Budgeting, saving, and investing early creates good habits

- Paying off debt with a plan on hand frees up future income

- Planning for big goals keeps you prepared

Action Items:

Frequently Asked Questions

How much money should you save in your 20s?

Aim to save 25% of income across emergency funds, retirement, and specific goals. Start with 10% if needed. By 30, have your annual salary saved for retirement and 3-6 months for emergencies. Personalize your plan based on your situation.

How much does the average 30-year-old have saved?

The median retirement savings for Americans under 35 is about $13,000, varying by education and location. Focus on consistent saving habits rather than comparing to averages. The most prepared 30-year-olds have savings equivalent to their annual salary.

What is the 50/30/20 rule?

A budgeting framework allocating after-tax income: 50% for needs (housing, utilities), 30% for wants (dining out, entertainment), and 20% for savings and debt repayment. Adjust percentages based on your specific situation while maintaining financial balance.

How much money should you have saved when you're 25?

Aim to save 50% of your annual income by 25. This includes a $5,000-$10,000 emergency fund and 5-10% of lifetime earnings and retirement contributions. Focus on consistent habits rather than specific numbers.

Does a 401 (k) count as savings?

Yes, a 401(k) does count as savings, but it's a specific type of retirement savings. While general savings (like emergency funds) are meant for short-term access, a 401(k) is designed specifically for long-term retirement savings with tax advantages and potential employer matching contributions.

Hi there! I’m Sandee Mapp, a Wealth Advisor from San Diego, California, specializing in holistic financial planning, portfolio management, and retirement planning. My passion for financial advising stems from the positive impact a financial advisor had on my life.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy. All advisory services are offered through Savvy Advisors, Inc. (“Savvy Advisors”), an investment advisor registered with the Securities and Exchange Commission (“SEC”).

Works Cited

- Data Sheet: Young Adult Financial Well-Being

- How Does the Well-Being of Young Adults Compare to Their Parents?

- Economic Well-Being of U.S. Households in 2024

- The Demographics of Household Debt in America

- Average Credit Card Interest Rate in US Today

- Usual Weekly Earnings of Wage and Salary Workers, Second Quarter 2025

- Here's how much money you should have saved by age 30