Are dividends taxed the same way for every investor? Not quite.

That difference can affect how much of your investment income you actually keep.

Many people focus on dividend yield—how much income an investment pays—without realizing how taxes quietly shape their after‑tax return. A dividend that appears attractive on paper can feel quite different once taxes are factored in.

This guide explains the taxation of dividends, with a clear breakdown of qualified dividends vs. ordinary income. By the end, you’ll have a better understanding of how dividend income works and how to make more tax‑aware investment decisions.

Key Takeaways

- Two Main Categories: Dividends are classified as either ordinary (taxed at your standard federal income tax rate of up to 37%) or qualified (taxed at lower long-term capital gains rates of 0%, 15%, or 20%).

- The Holding Period Rule: To receive the lower qualified tax rate, you must generally hold the stock for more than 60 days during the 121-day period surrounding the ex-dividend date.

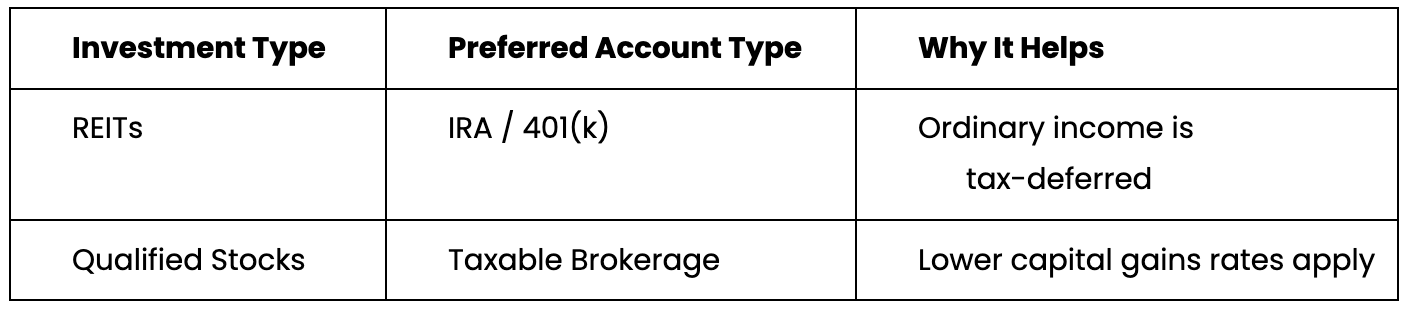

- Asset Location Strategy: To minimize tax drag, consider holding assets that pay ordinary dividends (such as REITs) in tax-advantaged accounts (IRAs/401(k)s), while keeping qualified dividend stocks in taxable brokerage accounts.

- Tax Reporting: Your specific breakdown is found on Form 1099-DIV, where Box 1a shows your total ordinary dividends and Box 1b indicates the portion eligible for preferential tax rates.

- Reinvestment Myth: Automatically reinvesting dividends (DRIPs) does not defer taxation; the IRS treats reinvested dividends as taxable income in the year they are paid.

Qualified vs. Ordinary Dividend Taxation

Not all dividends are taxed the same way. Some are taxed at your regular income tax rate; others qualify for lower, more favorable rates. Understanding this distinction is one of the easiest ways to better understand your tax picture as an investor.

Let’s start with why this gap exists and why it matters.

Understanding the Tax Rate Gap: Preferential vs. Ordinary Rates

Ordinary dividends are taxed like your paycheck. That means they fall under standard federal income tax brackets, which range from 10% up to 37%, depending on your income.

Qualified dividends are different. They are taxed at long‑term capital gains rates—0%, 15%, or 20%—which are typically lower than most ordinary income tax brackets.

For higher-income investors, it is also important to consider the 3.8% Net Investment Income Tax (NIIT). This additional tax can apply to both qualified and ordinary dividends once certain income thresholds are met, increasing the effective tax rate on your investment income.

Furthermore, don’t forget that most states also tax dividend income. While federal law distinguishes between qualified and ordinary dividends, many states tax all dividends at their standard income tax rates. Depending on where you live, these state taxes can further reduce your after-tax return, making specific asset location even more critical.

Consider this qualified dividend tax rate example: If you earn $1,000 in ordinary dividends and you’re in the 24% tax bracket, you could owe about $240 in federal taxes. If those same dividends are qualified and taxed at 15%, your tax bill drops to $150 without changing the investment.

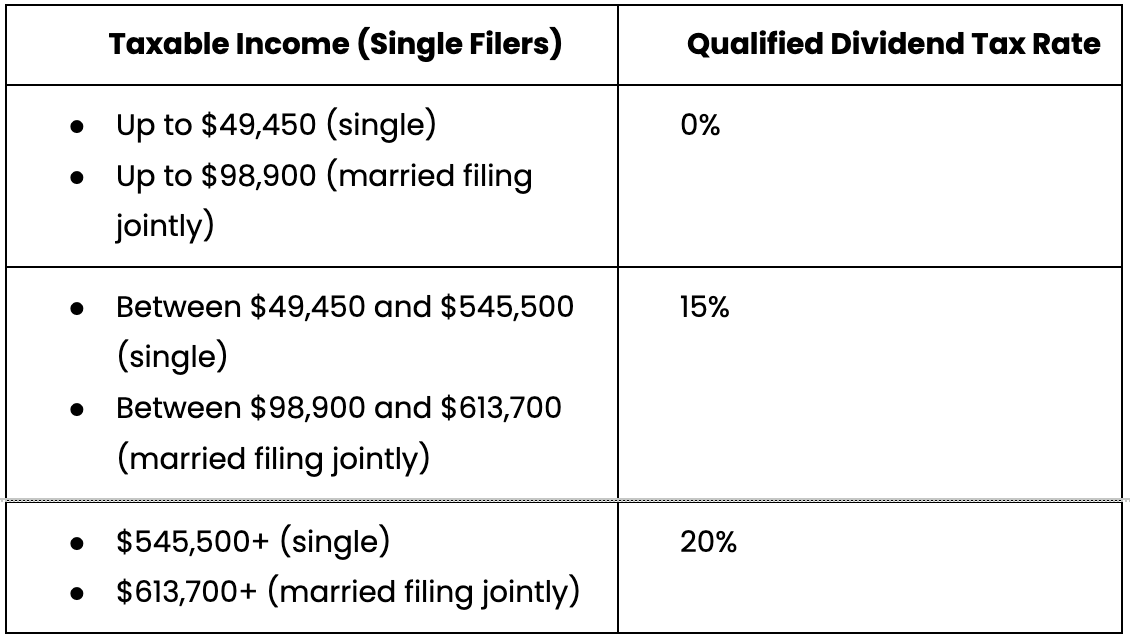

2026 Tax Rate Thresholds for Single Filers

The dividend tax rate for qualified dividends depends on your total taxable income. For single filers in 2026, the thresholds look like this:

The “61‑Day” Holding Period Rule and Eligibility

Whether qualified dividends are taxed at lower rates often comes down to how long you hold the investment.

To qualify, you must hold the stock for more than 60 days during the 121‑day period that begins 60 days before the ex‑dividend date.

To put things in perspective: If you buy a stock right before it pays a dividend and sell it a few weeks later, that dividend likely won’t qualify. Even though it came from a qualifying company, it would be taxed as ordinary income.

This rule applies to dividends from U.S. companies and qualified foreign corporations, making holding period awareness important for active traders. Even long‑term investors can be caught off guard if they rebalance or sell too quickly after a dividend is paid.

Qualified Foreign Corporations and Treaty Benefits

Dividends from foreign companies can receive qualified treatment if specific rules are met. Generally, the company must be based in a country with a comprehensive U.S. tax treaty or trade on a major U.S. exchange.

It’s also common for foreign governments to withhold taxes—sometimes up to 30%—before the dividend ever reaches you. You might see a $100 dividend reduced to $70 before it hits your account, depending on the country.

Even when treaty benefits apply, the standard holding period rules determine whether the dividend is qualified.

Dividend Tax Planning and Optimization Strategies

Knowing how dividends are taxed is helpful. Using that knowledge intentionally can reduce tax drag and improve after‑tax returns. Here are some strategies that align with that approach.

Strategic Asset Location: Taxable vs. Tax‑Advantaged Accounts

Where you hold dividend‑producing investments matters.

Investments that generate ordinary dividends, such as REITs, are often better placed in tax‑advantaged accounts like IRAs or 401(k)s. This defers taxes that would otherwise be due each year.

Stocks that pay qualified dividends are often more tax‑efficient in taxable brokerage accounts. Here, they can benefit from lower dividend tax rates.

Over time, keeping more of each dividend invested can compound into a meaningful difference.

Maximizing the 0% Tax Bracket through Income Management

For investors with taxable income under $49,450, qualified dividends may be taxed at 0% at the federal level. A retiree with modest income who holds qualified dividend‑paying stocks in a taxable account could receive dividend income without owing federal tax on it.

Managing income sources, such as the timing of Roth conversions or withdrawals, can keep dividends in lower tax brackets. Such coordination is especially beneficial for retirees or investors with flexible income streams.

Selecting Tax‑Efficient Investment Vehicles (ETFs vs. Mutual Funds)

ETFs tend to be more tax‑efficient than traditional mutual funds. One reason is lower portfolio turnover, which usually results in fewer taxable distributions.

Funds with low turnover also tend to distribute a higher percentage of qualified dividends. In taxable accounts, ETFs or index funds can curb unexpected tax bills. Year‑end tax season becomes more predictable, particularly for newer investors.

Tax‑Loss Harvesting and Dividend Timing

Tax‑loss harvesting allows investors to sell investments at a loss to offset gains or reduce taxable income. This can lower the tax owed on dividends.

Timing matters, too. As mentioned, selling a stock before meeting the 61‑day holding rule can turn a qualified dividend into ordinary income. This often happens unintentionally when investors trim positions or rebalance shortly after receiving a dividend. In more complex situations, professional guidance can assist with coordinating timing decisions.

Specific Investment Vehicle Taxation

Different investment types generate income that’s taxed in different ways. Knowing what to expect can help avoid unwelcome surprises.

Common Stocks and the Standard Holding Period

Most dividends from U.S. common stocks qualify for lower tax rates if they meet the 61‑day holding rule. These are the most common sources of qualified dividends for individual investors.

Owning individual stocks also gives you direct control over how long you hold them.

REITs and the 199A Pass‑Through Deduction

REIT dividends are usually taxed as ordinary income, not qualified dividends. Some portions may qualify for the Section 199A pass‑through deduction.

Due to this tax treatment, REITs are often held in tax-deferred accounts. However, it is worth noting that some real estate investments can have a portion of distributions classified as return of capital, which is not immediately taxable and instead reduces cost basis. Because of that, the optimal placement of a particular investment can vary depending on its specific tax characteristics.

Master Limited Partnerships (MLPs) and Return of Capital

MLP distributions are typically considered a return of capital, meaning they are not subject to immediate taxation. Instead, they reduce your cost basis.

The trade‑off: added complexity, including special tax forms and potential taxes when the investment is sold.

International Equities and Foreign Tax Credits

Foreign stocks may pay qualified dividends if treaty requirements are met. However, taxes are typically withheld before the dividend is paid.

Foreign tax credits can sometimes offset these taxes, depending on your situation. This is one area where individual circumstances carry sizable weight, and small details can change the outcome.

Municipal Bonds: The Federal Tax‑Exempt Advantage

Interest from municipal bonds is generally exempt from federal income tax. In some cases, state and local tax exemptions may also apply.

Unlike corporate dividends, muni bond interest offers tax‑free income. This can be appealing for investors in higher tax brackets.

Tax Form Reporting and Compliance

The most effective tax strategy requires accurate reporting. Understanding how dividend income flows through tax forms reduces errors, prevents underreporting, and makes sure you receive the tax treatment you expect.

Decoding Form 1099‑DIV: Box 1a vs. Box 1b

Form 1099‑DIV summarizes your dividend income for the year and is issued by your brokerage, typically by early February. It’s also where the distinction between ordinary dividends vs. qualified dividends becomes clear.

- Box 1a (Ordinary Dividends) shows the total amount of dividends you received, regardless of how they’re taxed.

- Box 1b (Qualified Dividends) identifies the portion of Box 1a that qualifies for lower long‑term capital gains tax rates.

If Box 1a shows $5,000 but Box 1b shows $3,500, only that $3,500 is eligible for preferential tax treatment. The remaining $1,500 is taxed as ordinary income. Reviewing both boxes helps you estimate your actual after‑tax dividend income.

Distinguishing Dividend Income (1099‑DIV) from Compensation (1099‑NEC)

Form 1099‑DIV reports income earned from investments you own, such as stocks, ETFs, and mutual funds. Form 1099‑NEC reports income earned from work performed as an independent contractor or freelancer.

Both types of income are taxable, but their treatment is quite different. Dividend income may qualify for lower tax rates. 1099‑NEC income is subject to ordinary income tax and self‑employment taxes. Confusing the two can lead to reporting errors or inaccurate tax estimates.

Filing Procedures: Form 1040 and Schedule D

Reported on Form 1040, dividend income contributes to your annual total taxable income.

Qualified dividends receive special treatment through IRS worksheets that apply lower capital gains tax rates. Those calculations are reflected alongside Schedule D, even though dividends themselves don’t always appear on the form.

Most tax software can automatically import 1099-DIV data, apply the correct rates, and support e-filing, even for more complex dividend income.

Leveraging Tax Software and CPAs

Tax software like TurboTax or H&R Block can handle dividend income tax calculations for many investors by:

- Identifying qualified vs. ordinary dividends

- Applying the correct tax rates automatically

- Importing data directly from brokerage forms

For straightforward portfolios, this is often enough.

Investors with large portfolios, foreign dividends, multiple accounts, or advanced planning needs may benefit from working with a CPA. A professional ensures compliance and offers optimization guidance that software may not surface on its own.

Bringing It All Together: What Dividend Taxes Really Mean for You

The big ideas to remember:

- Qualified dividends can significantly reduce your tax bill compared to ordinary income.

- Holding periods and where assets live materially affect after-tax returns.

- Different investment types generate dividends taxed in very different ways.

- Clear, accurate reporting is about compliance and is part of smart tax planning.

The next steps to take:

- Remember that asset location is not one-size-fits-all; it should be tailored to the specific investment’s tax characteristics and your overall financial plan.

- Take a fresh look at where your dividend-producing investments are held.

- Confirm which dividends qualify for preferential tax treatment.

- Coordinate dividend income with other income sources to manage tax brackets.

- Seek professional guidance if your portfolio, income, or tax situation is more complex.

FAQs

Do you pay taxes twice on dividends?

No, individual investors are not taxed twice on dividends. While companies pay corporate tax on profits before issuing dividends, shareholders only pay tax once at the individual level. This is a common concern, but for personal tax filing, dividends are taxed only when you receive them.

Are dividends taxed if reinvested?

Yes. Dividends are taxed in the year they are paid, even if you reinvest them automatically through a dividend reinvestment plan (DRIP). The IRS treats reinvested dividends the same as cash dividends for tax purposes.

What happens if you don't report dividends on taxes?

Unreported dividends can trigger IRS notices, penalties, and interest. Brokerages report dividend income directly to the IRS, so mismatches are easy to spot. Even small amounts should be reported to avoid problems later.

Is it better to reinvest dividends or get cash?

It depends on your goals. Reinvesting dividends can help grow wealth over time through compounding. Taking cash may make sense if you need income, such as during retirement. The tax treatment is the same either way in taxable accounts.

How do the rich avoid taxes on stocks?

Wealthy investors often use strategies like holding investments long term, borrowing against assets instead of selling, using tax-advantaged accounts, and carefully managing income timing. These approaches focus on deferring or reducing taxes legally, not avoiding them outright.

With over a decade of experience, Jason Craine helps families achieve their financial goals through personalized, comprehensive planning. His career in finance began in 2010 and includes a diverse background in banking, investment management, accounting, and insurance. In 2019, he relocated to Wichita to open Mariner Wealth Advisors’ first office in the area, where he has built a successful planning practice. He holds a B.S. in Business Administration from William Jewell College, is a Certified Financial Planner™ (CFP®), and maintains several additional industry credentials. Outside of work, he is active in the community, serving on the boards of Exploration Place, the Andover YMCA, and the Financial Planning Association of Kansas, as well as contributing to his local elementary school council.

Contact a Savvy advisor

Contact a Savvy advisor