Regime change at the Fed

June flipped May's script. A changing of the guard at the Federal Reserve, Chair Warsh's hawkish FOMC debut, repriced markets away from rate cuts and toward the possibility of another hike, and the long-duration growth complex that had led all year bore the brunt. The S&P 500 fell -0.95% and the Nasdaq -2.75% in June, while small caps (Russell 2000 +3.74%) and the equal-weight S&P 500 (+2.38%) held up: a textbook rotation out of mega-cap technology and into value, financials, and defensives. Meanwhile, the spring's biggest geopolitical risk faded as the Iran conflict de-escalated, the Strait of Hormuz moved toward reopening, and crude oil dropped -16.82%, easing inflation concerns. Despite this increasingly disinflationary backdrop, investors embraced a more hawkish policy outlook, reflecting confidence that the new Fed leadership would prioritize inflation credibility over near-term easing. The takeaway: the macro backdrop remains fundamentally sound, but June marked the month the hawkish-Fed risk became the market's central focus.

- The Fed's regime change. Chair Warsh's first FOMC (June 16–17) put price stability first; the SEP raised 2026 median core PCE to 3.3% (from 2.7%) and cut unemployment to 4.3%; 9 members signaled hikes this year (5 expecting 2). Cuts were priced out; a hike entered the debate.

- Growth derated, leadership rotated. S&P 500 -0.95%, Nasdaq -2.75%; Russell 2000 +3.74%, S&P Equal-Weight +2.38%. Industrials +7.29%, Health Care +6.62% led; Communication Services -7.78%, Energy -5.06% lagged.

- Oil collapsed on de-escalation. WTI -16.82% as Hormuz reopening odds rose (~83% by year-end), removing the spring energy-shock premium.

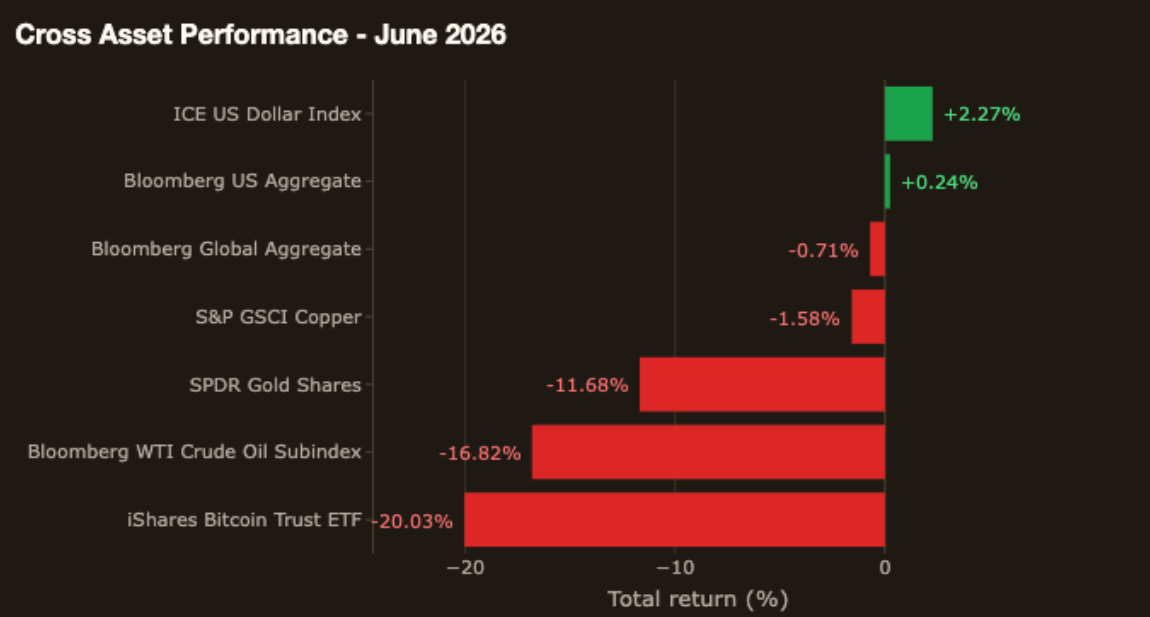

- Risk-off in the speculative tail. Bitcoin (IBIT) -20.03%, Gold -11.68%, while the US Dollar gained +2.27%, all consistent with a more hawkish Fed and higher real yields.

- Bonds held up. Bloomberg US Aggregate +0.24%, Global Aggregate -0.71%. Quality duration proved resilient even as the front end repriced on the Fed.

Noteworthy developments

Rotation: the cost of a higher policy ceiling

The single story of June was rotation. A credible, inflation-first Fed lifts the discount rate on the longest-duration cash flows first, which is exactly why the AI/mega-cap-growth leaders (Comm Services, Discretionary, Tech) fell hardest while shorter-duration cyclicals and defensives (Health Care, Industrials, Utilities, Financials) gained. Small caps and the equal-weight index outperformed, a clear sign breadth improved even as the cap-weighted index fell. This is the constructive interpretation of a hawkish pivot: a re-rating of who leads, while the economy itself stayed sound.

U.S. equities: index down, breadth up, a rotation out of mega-cap growth

U.S. equities finished June with a split tape: the cap-weighted indexes fell, but participation underneath improved. The S&P 500 declined -0.95% and the Nasdaq -2.75% as investors repriced long-duration growth, while the Russell 2000 gained +3.74% and the equal-weight S&P 500 rose +2.38%, a clear sign the month's weakness stayed concentrated in a handful of mega-cap leaders rather than a broad retreat from risk.

Sector leadership told the same story. Industrials (+7.29%) and Health Care (+6.62%) led, alongside utilities and financials, while Communication Services (-7.78%) and Energy (-5.06%) lagged sharply. Communication Services and the long-duration growth complex absorbed most of the hawkish-Fed repricing; cyclicals and defensives held up far better.

The headline index declined, but breadth improved underneath. That is the profile of a rotation: a re-rating of leadership and valuations, with the underlying economy still intact.

- June returns (through 2026-06-30): S&P 500 -0.95% · Nasdaq Composite -2.75% · Russell 2000 +3.74% · S&P 500 Equal-Weight +2.38%.

- Sector leaders: Industrials +7.29%, Health Care +6.62%, Financials +4.37%, Utilities +2.71%, Real Estate +0.84%, Consumer Staples +0.50%.

- Sector laggards: Materials +0.02%, Information Technology -3.28%, Consumer Discretionary -4.69%, Energy -5.06%, Communication Services -7.78%.

- Takeaway: The market slipped, but it got healthier underneath: money rotated out of a handful of pricey tech names into health care, banks, industrials, and steadier dividend-payers.

International markets: mixed regionally, led lower by China

International equities mostly declined in June as a stronger U.S. dollar and a hawkish Fed repricing weighed on global risk appetite. The MSCI EAFE Index gained 0.09% while emerging markets slipped 1.36%, with Europe and China among the weaker regions.

The regional picture was mixed. India (+1.53%) and Korea (+0.33%) led gains, while China (-7.05%) lagged sharply. Taiwan (+1.27%) surrendered part of its earlier advance but still finished the month in positive territory. Germany (-3.17%) and Australia (-2.80%) also struggled as a stronger U.S. dollar and higher Treasury yields weighed on international markets.

For internationally diversified portfolios, June was a reminder that U.S. policy and currency moves still transmit quickly abroad, even when the underlying AI and semiconductor themes remain structurally relevant.

- Up: India +1.53%, Taiwan +1.27%, Korea +0.33%, EAFE +0.09%.

- Down: Japan -0.31%, Emerging Markets -1.36%, Canada -1.80%, Australia -2.80%, Mexico -3.10%, Germany -3.17%, China -7.05%; broad MSCI EAFE +0.09% and MSCI EM -1.36%.

- Takeaway: A stronger dollar weighed on most foreign markets; Taiwan gave back earlier gains but still finished positive, while India and Korea were the relative standouts and China lagged.

Fixed income: the Fed repriced the front, the long end held

Fixed-income markets held up better than equities in June. The Bloomberg U.S. Aggregate Index returned +0.24% and the Global Aggregate -0.71%, suggesting that high-quality duration proved resilient even as the Federal Reserve turned more hawkish.

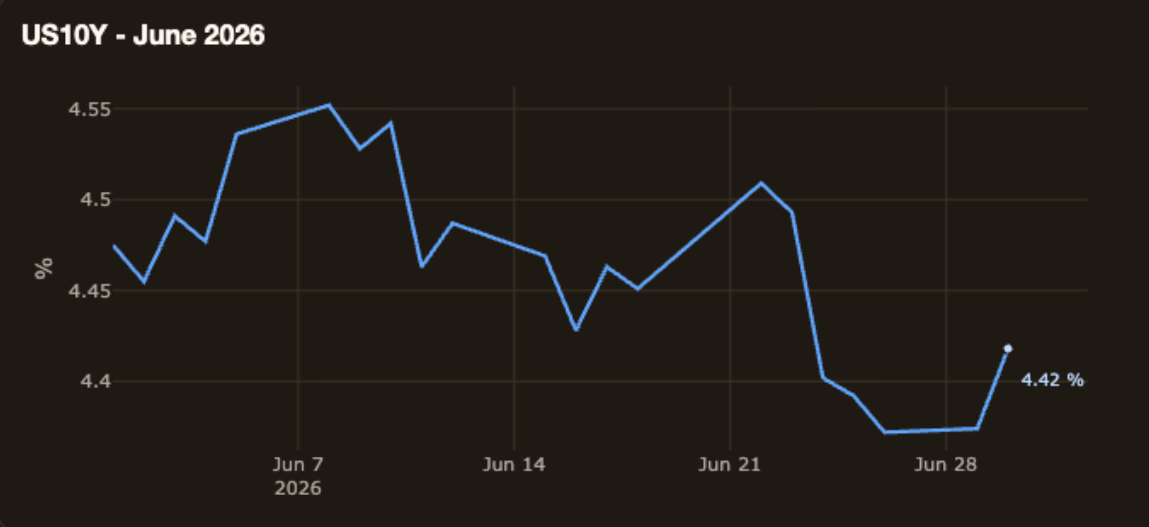

The yield-curve story was nuanced. Chair Warsh's FOMC debut pushed the front end higher and supported a stronger dollar, but the 10-year Treasury eased to roughly ~4.46% by month-end, with 2s10s near ~+0.30pp. The market repriced near-term policy risk without fully breaking the long end: a mild flattening rather than a broad bond selloff.

On the income side, the month reinforced the “hold to earn” message: bonds did their job as ballast even as growth stocks derated.

- Bloomberg US Aggregate +0.24%, Global Aggregate -0.71%.

- The 10-year stood at ~4.46% (2026-06-30) with 2s10s ~+0.30pp: the hawkish Fed lifted the front end, but the long end held, a mild flattening.

- Takeaway: The Fed's tougher tone pushed short-term yields up, but longer-term rates held steady, so high-quality bonds still paid you to wait.

Commodities: oil cracks as the Middle East calms

Commodities and cross-asset markets reflected June's twin forces: Middle East de-escalation pulling energy lower, and a hawkish Fed lifting the dollar and pressuring the speculative complex.

WTI crude fell -16.82%, the month's most important disinflationary development, as the Strait of Hormuz risk premium drained. Gold (-11.68%) and Bitcoin (-20.03%) also declined, consistent with higher real yields, a firmer dollar (+2.27%), and fading geopolitical urgency. Copper (-1.58%) was roughly flat to slightly negative, a modest read on global industrial demand.

In plain terms: the drop in oil is relief at the pump and for inflation expectations, even as the Fed's tougher tone kept pressure on non-yielding assets.

- WTI crude -16.82%; S&P GSCI Copper -1.58%.

- Gold -11.68% (higher real yields, stronger dollar, fading geopolitical bid).

- Cross-asset context: US Dollar +2.27% and Bitcoin -20.03%.

- Takeaway: Oil fell sharply as the Middle East de-escalated, easing inflation and gas prices, while gold and crypto pulled back.

Macro

Growth: the economy kept expanding, even as growth stocks sold off

June's market action looked scary on the surface, but the hard data told a different story. Hard data still pointed to an economy that was growing, even as high-frequency trackers cooled: the Weekly Economic Index averaged 2.67% year to date (through 2026-06-20), and the Atlanta Fed's GDPNow model estimated roughly 1.2% for 2026Q2 as the quarter closed (as of 2026-07-01). That pace is positive though cooled from spring estimates. It points to an economy that is still expanding, well short of a recession, even if it is no longer running hot.

What changed in June was how the market priced growth rather than growth itself. Chair Warsh's hawkish Federal Reserve debut lifted the discount rate on long-duration assets, and the mega-cap technology leaders that had carried the index all year fell hardest. Meanwhile, small caps gained meaningfully, cyclicals and defensives rose, and the equal-weight S&P 500 finished positive. That split is exactly what you would expect when multiples compress rather than when the business cycle turns.

The distinction matters. Payroll and spending data through May still pointed to a resilient labor market and consumer. The June equity drawdown stayed concentrated in a handful of expensive growth names rather than the broad economy.

- Takeaway: The economy is still growing: June's stock pullback was about interest rates and valuations rather than a sign that the expansion is ending.

Inflation: still above target, but moving in the right direction

Inflation remained the Fed's central problem in June, but the trajectory improved. Headline CPI stood at 4.27% in May 2026, and the Cleveland Fed's June 2026 nowcast eased toward ~3.92% (as of 2026-06-30), still well above the Fed's 2% target but no longer accelerating. The distinction between “high” and “high and getting worse” is the one that matters for policy and for portfolios, and June leaned toward the former.

The Fed's own projections confirmed the stickiness. At the June FOMC, the Summary of Economic Projections raised the median 2026 core PCE forecast to 3.3%, up from 2.7%. Futures markets repriced accordingly, with investors moving from debating rate cuts to debating whether the next move could be a hike.

The wildcard was energy. As the Iran conflict de-escalated and crude fell roughly -16.82% in June, a meaningful wartime risk premium drained from oil. That is a genuine disinflationary tailwind for gasoline, goods prices, and household budgets heading into the summer.

- Takeaway: Inflation is still too high for comfort, but it is easing rather than re-accelerating, and the drop in oil is giving households and the Fed a bit more breathing room.

Financial conditions: a credible, hawkish Fed repriced the path

The defining macro event of June was a regime change at the Federal Reserve rather than any single data print. Chair Warsh's first FOMC meeting (June 16–17) sent an unambiguous message: price stability comes first. Markets heard it clearly.

The SEP showed 9 members signaling rate hikes this year, with 5 expecting 2 increases. The median unemployment projection was revised down to 4.3%, while core PCE was revised up, a combination that leaves little room for near-term easing. Rate-cut expectations faded, and the debate shifted to whether the Fed might need to hike if inflation does not cooperate.

Fed Funds futures (Monetary Policy dashboard, ZQ strip) price ~0.9 hike into Dec 2026 (implied FF ~3.90% vs SOFR ~3.68%) and ~1.0 hike through Dec 2027 (~3.92%).

The market response was immediate: the front end repriced higher, the U.S. dollar gained ~2.5%, and long-duration growth assets derated. Yet broad financial-conditions gauges remained accommodative (Chicago NFCI ~-0.50, St. Louis Financial Stress ~-0.64 as of 2026-07-02): policy is restrictive, conditions are not.

- Takeaway: The Fed just told the market it will prioritize inflation over supporting stocks: financial conditions are still easy enough to keep the economy going, but the Fed has lowered the ceiling on how much risk the market can take.

Geopolitics: the spring's biggest fear eased, and oil fell sharply

For most of the spring, geopolitics was the market's primary anxiety. The Iran conflict and the threat to the Strait of Hormuz fed directly into energy prices, inflation expectations, and Fed policy uncertainty. June brought a meaningful shift in that narrative.

A ceasefire framework emerged with a phased reopening of Hormuz, and markets began pricing a high probability of normalization by year-end (~83% on prediction markets). As the wartime risk premium drained, WTI crude fell roughly -16.82%, the single largest cross-asset move of the month outside of the speculative complex.

The strategic risk has not disappeared, but for June the energy-to-inflation-to-Fed transmission chain that dominated the spring went quiet.

- Takeaway: The Middle East risk that worried markets all spring eased in June and pulled oil prices down, which is good news for inflation and gas prices, as long as the truce holds.

Key dates to watch in July 2026

Growth

- Jul 1: ISM Manufacturing PMI.

- Jul 2: Nonfarm Payrolls, Unemployment Rate.

- Jul 6: ISM Non-Manufacturing PMI.

- Jul 16: Retail Sales.

Inflation

- Jul 14: Core CPI, CPI.

Financial conditions

- Jul 29: Fed Interest Rate Decision.

The bottom line

June was the month the market took the new Fed at its word. A hawkish Warsh pivot derated the long-duration growth leaders, but the damage was contained and constructive underneath: breadth improved, small caps and value rose, and the collapse in oil is a meaningful disinflationary offset. The economy is still expanding and financial conditions remain easy: this looks like a re-rating of leadership rather than a growth scare. But with a Fed now anchored on inflation and a hike back on the table, the market's tolerance for an inflation or earnings disappointment has narrowed. Constructive on the economy, rotated in leadership, and increasingly deferential to the Fed.

Anshul Sharma is Chief Investment Officer at Savvy Wealth, where he oversees the firm’s investment strategy, portfolio design, and platform innovation. He partners across product, marketing, and operations teams to deliver portfolios that take a methodological approach to balance customization with scalability for advisors and their clients. Before joining Savvy, Anshul spent nearly two decades at Bank of America, where he managed the Chief Investment Office’s Sustainable Model Portfolio Suite, launched new proprietary offerings, and, as Head of Alternative Investment Strategy, provided guidance and thought leadership to advisors around hedge fund, private market, and real asset strategies. He began his career as an Investment Strategist at U.S. Trust, designing multi-asset portfolios for high-net-worth and institutional clients. Anshul holds a Master of Financial Engineering from UC Berkeley and a Bachelor of Computer Engineering from Lehigh University. Outside of work, he is an avid tennis player, enjoys time with his wife, two sons, and their Bernedoodle, and is an auto enthusiast who loves cooking and travel.

Ani Vedere is a Senior Research Analyst at Savvy Wealth, where he works across macro research, portfolio construction, and investment technology. He partners closely with the Chief Investment Officer and cross-functional teams spanning product, engineering, and design to develop scalable investment solutions, advisor-facing tools, and research workflows that help advisors deliver better outcomes for clients. Prior to joining Savvy, Ani was an Investment Analyst at a registered investment advisor, where he managed model portfolio implementation across hundreds of client accounts and built automated research and portfolio monitoring systems using Python and AI. Before that, he spent four years at a discretionary global macro hedge fund conducting multi-asset research, developing systematic investment frameworks, and building analytics to support portfolio management and trading decisions. Ani holds a Bachelor of Science in Finance from the University of Connecticut. Outside of work, he enjoys spending time outdoors, watching movies (in theatres!), reading, and writing. Fair warning: ask him about markets or macroeconomics, and you may end up in a much longer conversation than you planned.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Inc. is a technology company. Savvy Advisors, Inc. is an SEC registered investment advisor. For purposes of this article, Savvy Wealth and Savvy Advisors together are referred to as "Savvy". All advisory services are offered through Savvy Advisors, while technology is offered through Savvy Wealth. The views and opinions expressed herein are those of the speakers and authors, and do not necessarily reflect the views or positions of Savvy Advisors.