A Tale of Two Markets: Yields Ease as Equities Search for Direction

November was a month of contrasts. While equity markets wrestled with bouts of volatility and uneven leadership, the more important story, in our view, was the market's growing confidence in the disinflation trend and the clearer path it sets toward easier monetary policy. Even without an official October CPI release, investors leaned on earlier data and alternative indicators to reaffirm the idea that inflation is continuing to cool. That shift helped pull long-term yields modestly lower and supported fixed income valuations.

Net-net, November played out as a tale of two markets: bonds found their footing as yields eased, while equities navigated a choppier backdrop marked by large-cap tech swings and lingering questions about the durability of the expansion.

November Highlights: Bonds Take the Lead

With the government shutdown resolved, some delayed economic releases resumed, but the October CPI report was canceled entirely. Markets instead relied on September inflation, PCE, and real-time indicators. Together, they painted a consistent picture: inflation has drifted toward the three percent range over recent months, and broader growth signals are cooling at a measured pace.

Against that backdrop, the 10-year Treasury yield drifted toward the 4.0% area by month-end. The move was not dramatic, but it was meaningful enough to create a supportive environment for high-quality fixed income.

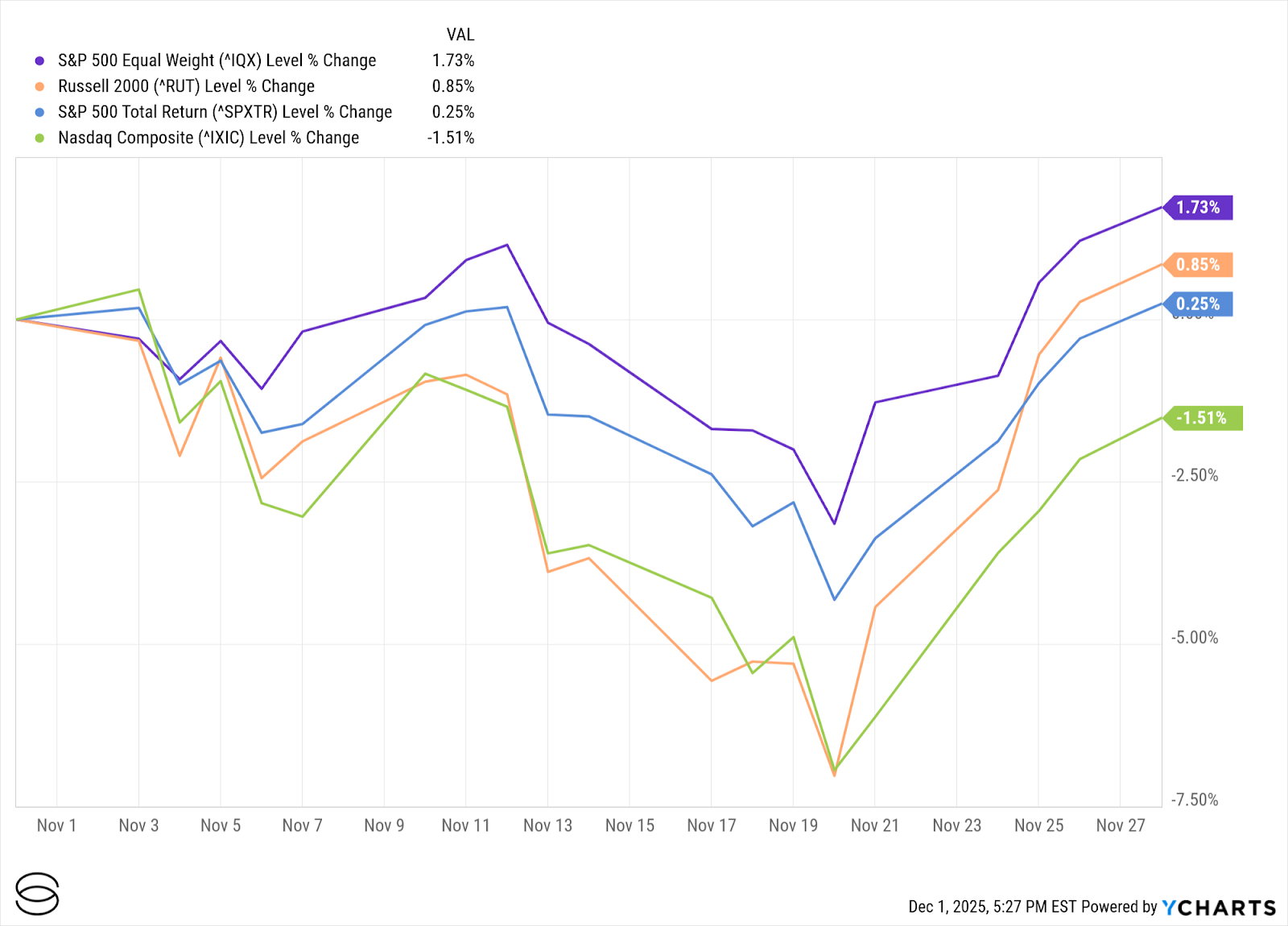

Equities, meanwhile, were more uneven. The S&P 500 ended roughly flat to modestly positive, but heightened volatility in large technology names left the Nasdaq softer and underscored how dependent major benchmarks remain on a narrow group of leaders.

Featured Theme: Cracks in Concentration

November's equity performance reinforced a theme we have highlighted for some time: the power and fragility of concentrated market leadership.

After a strong run, mega-cap tech and AI-linked companies saw a wave of profit-taking and valuation reassessment. The Nasdaq recorded its first monthly decline since March before staging a late-month recovery. The S&P 500 felt these cross-currents as pressure on the largest names offset steadier performance across several other sectors.

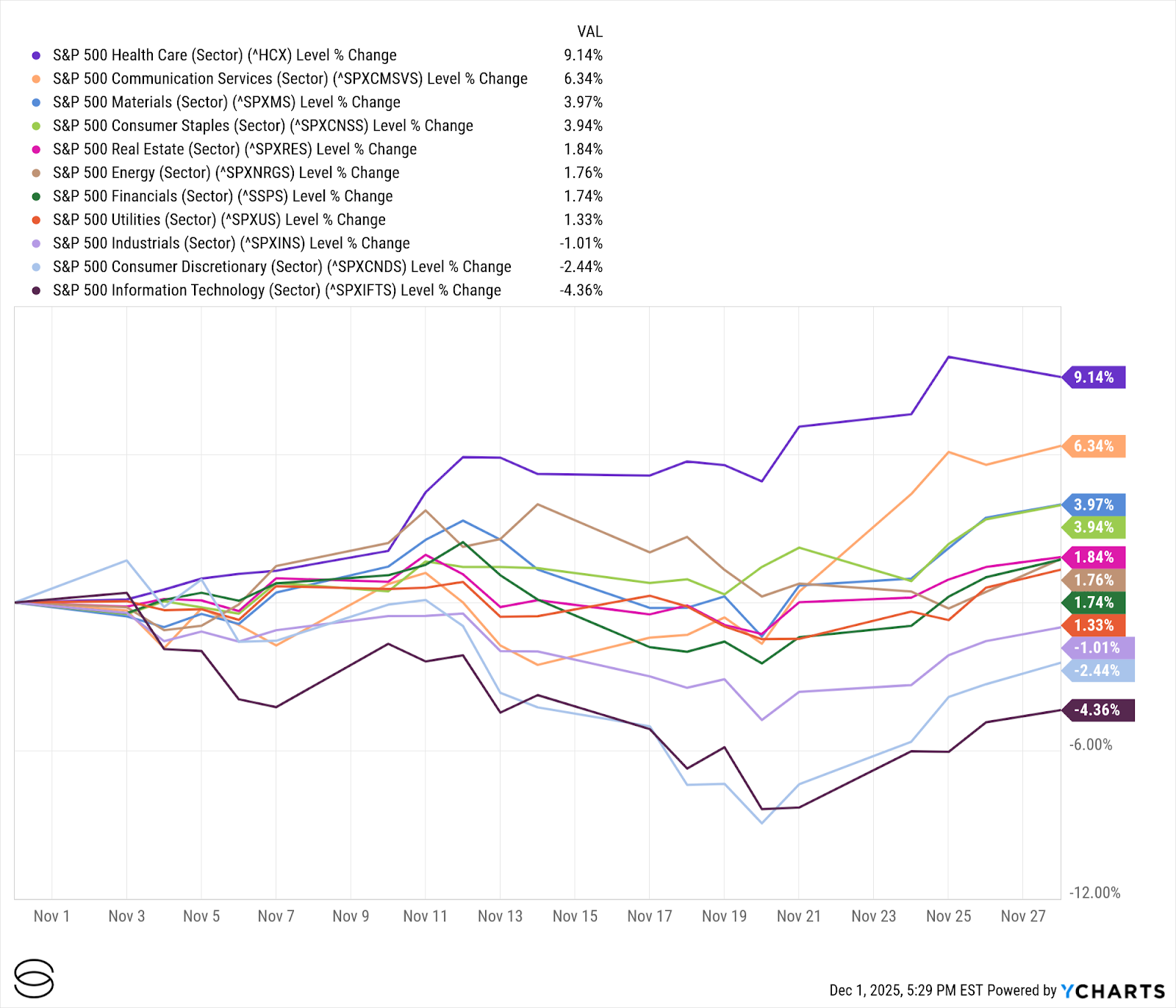

Beneath the headline numbers, rotation was meaningful. Health care delivered one of its strongest months in years. Rate-sensitive sectors like utilities and consumer staples also outperformed, while high-momentum growth groups lagged as investors paused to reassess how much future AI demand is already priced in.

U.S. Markets

U.S. large-caps essentially paused in November after strong gains earlier in the quarter, leaving full-year returns comfortably positive. But the calm on the surface masked wide dispersion underneath.

Growth and quality factors remained supportive over the longer horizon, although November showed that even the most durable leaders are not immune when positioning becomes crowded. Leadership also began to rotate: health care set new highs, while several technology names cooled as investors debated how far ahead of fundamentals the AI surge has gotten.

Small and mid-caps were choppier, reflecting ongoing sensitivity to financing costs and the growth outlook. Even so, late-month trading hinted at healthier breadth as investors selectively re-engaged with cyclicals, financials, and industrials tied to a still resilient domestic economy.

Exhibit 1: U.S. Equity Performance

Exhibit 2: U.S. Equity Sector Performance

Developed International and Emerging Markets

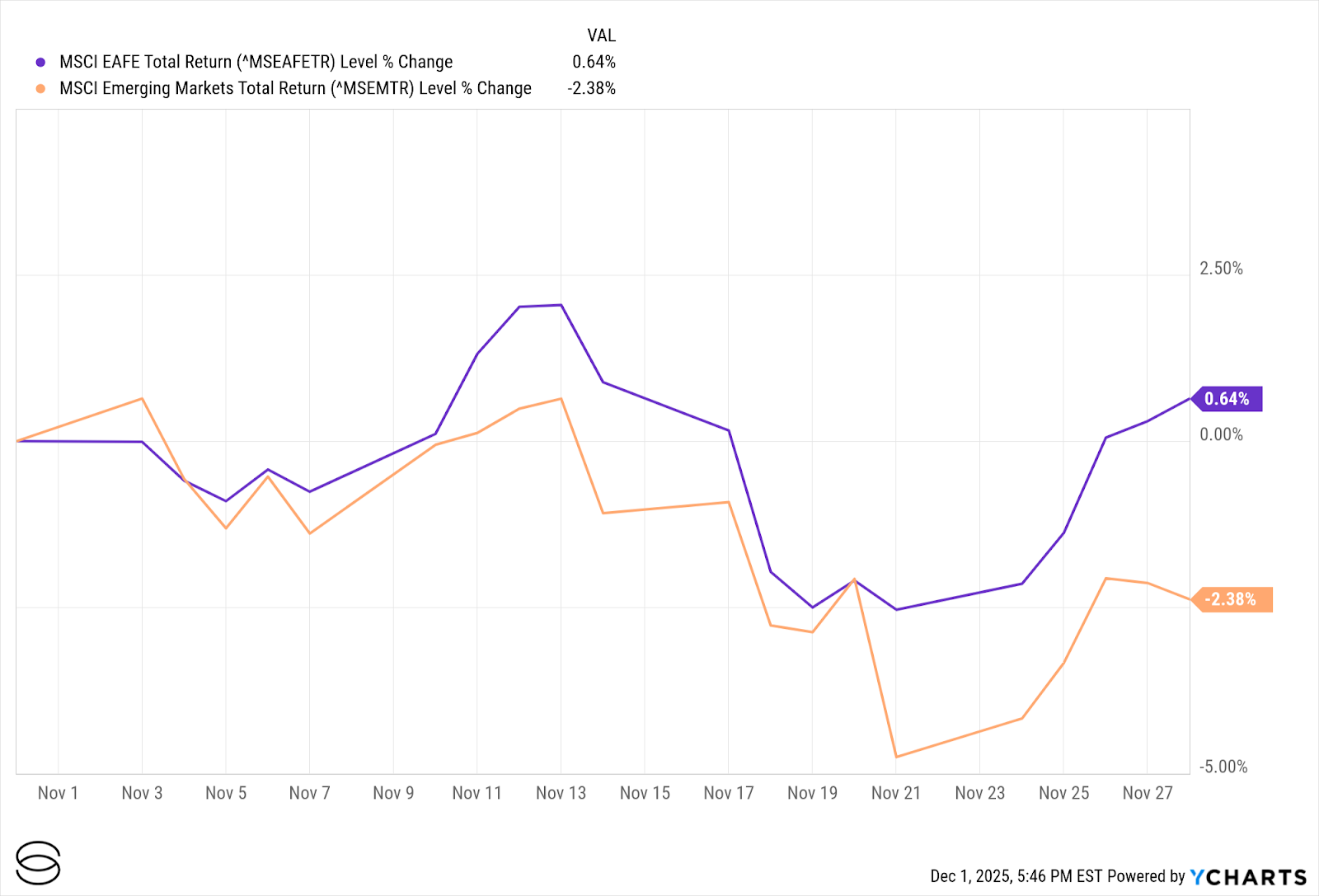

Developed international markets posted mixed but generally positive results, helped by a softer dollar and incremental progress on inflation across Europe and other major economies. Earnings revisions have stabilized in several regions, giving international allocations a firmer footing even as policy and political risks remain in focus.

Emerging markets were more uneven. Concerns around China's growth trajectory, softer commodity prices, and idiosyncratic political risks weighed on sentiment. At the same time, the prospect of a gentler global rate environment continues to provide support. We are watching closely for areas where valuations, policy flexibility, and structural growth drivers are starting to align.

Exhibit 3: International Equity Performance

Cross-Asset Performance

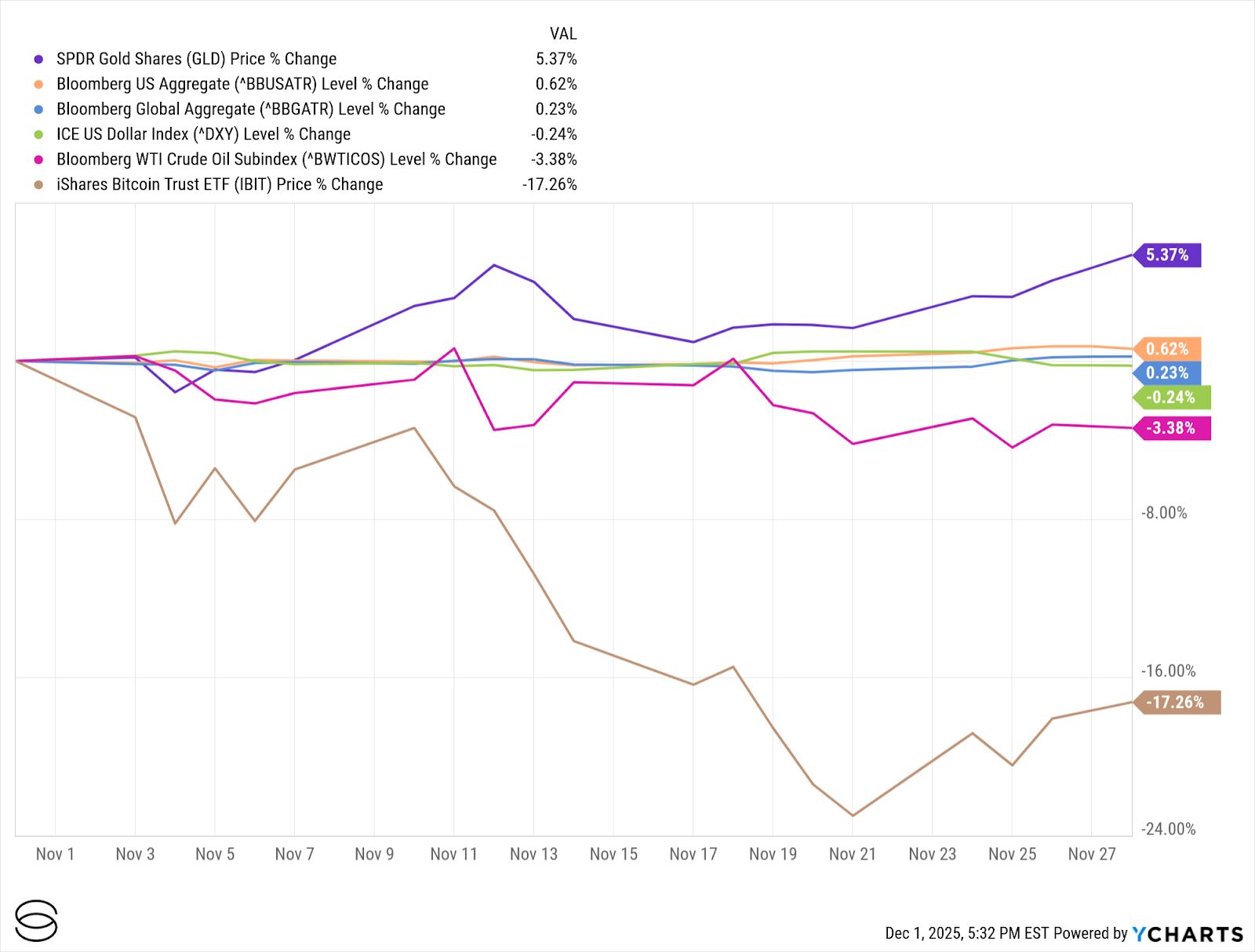

Fixed income was one of the brighter spots in November. Modest declines in yields translated into positive total returns across many global bond benchmarks. Duration exposure, particularly in higher-quality sovereigns and investment-grade credit, offered useful ballast against equity volatility.

Commodities were more mixed. Gold benefited from lower real yields and a weaker dollar, while crude oil drifted lower on concerns about oversupply and softer industrial demand. Together, these moves reinforced an environment where inflation pressures are easing but growth remains steady rather than robust.

Exhibit 4: Cross-Asset Performance

Economy and Policy

With the shutdown resolved early in the month, markets regained access to some delayed data, though the October CPI reading was ultimately canceled. Investors turned to earlier releases, real-time indicators, and corporate earnings commentary to understand the trajectory of prices and demand.

At its late October meeting, the Federal Reserve lowered its target range to 3.75% to 4.00% and adopted a more dovish tone, citing cumulative tightening and the lagged impact of prior hikes. Fed communication in November echoed this stance: patient, data dependent, and increasingly comfortable with continued disinflation.

Policy Watch: Where Do Rates Go From Here?

Heading into year-end, the market's conviction is strengthening that the Fed is done hiking and is moving gradually toward an easing bias. Futures markets showed a high probability of a December rate cut, dipping mid-month as commentary turned more cautious, then climbing back into the roughly 80 to 90 percent range by month-end.

This pricing leaves limited room for upside surprises. A reacceleration in inflation or a sudden tightening in the labor market would force markets to recalibrate expectations, creating pressure on longer-duration assets and the most rate-sensitive corners of the equity market.

Key Dates to Watch in December

December 13: November CPI and Core CPI

This is the first full set of inflation data since the shutdown. Investors will be watching whether disinflation continues at a steady pace, especially in shelter and services.

December 18: Federal Reserve Meeting and Updated Dot Plot

The final Fed meeting of the year will offer fresh guidance on policymakers' expectations for growth, inflation, and the timing of rate cuts in 2026.

Mid-December: Retail Sales and Holiday Spending Trends

Consumer strength remains central to the outlook, and November and early December spending patterns will provide important signals heading into the new year.

Late December: PCE Inflation

The Fed's preferred inflation measure will help validate whether the broader disinflation trend remains intact.

Final Week of December: Liquidity and Technicals

Thin trading conditions, year-end rebalancing, and tax management can create short-term volatility even when fundamentals are stable.

Conclusion: A Month That Clarified the Path Ahead

November was a reminder that this stage of the cycle is defined less by dramatic surprises and more by transition. Equity markets worked through shifts in leadership and intermittent volatility, while the steady progress on inflation helped anchor expectations that the most aggressive phase of tightening is behind us.

Yields eased, fixed income regained some footing, and sector leadership broadened modestly beneath the surface. Uncertainties remain around growth, policy timing, and the durability of earnings, but the broader backdrop continues to move toward greater balance: slower inflation, a more patient Federal Reserve, and a market narrative that is gradually diversifying beyond a handful of themes.

As we head into December, attention turns to the upcoming inflation reports and the final Federal Reserve meeting of the year. Together, these events will help shape how markets interpret the early part of 2026. For now, November's crosscurrents point to a market that is recalibrating rather than retreating as investors digest the contours of an economy that is moving steadily toward a post-tightening environment.

Anshul Sharma is Chief Investment Officer at Savvy Wealth, where he oversees the firm’s investment strategy, portfolio design, and platform innovation. He partners across product, marketing, and operations teams to deliver portfolios that take a methodological approach to balance customization with scalability for advisors and their clients. Before joining Savvy, Anshul spent nearly two decades at Bank of America, where he managed the Chief Investment Office’s Sustainable Model Portfolio Suite, launched new proprietary offerings, and, as Head of Alternative Investment Strategy, provided guidance and thought leadership to advisors around hedge fund, private market, and real asset strategies. He began his career as an Investment Strategist at U.S. Trust, designing multi-asset portfolios for high-net-worth and institutional clients. Anshul holds a Master of Financial Engineering from UC Berkeley and a Bachelor of Computer Engineering from Lehigh University. Outside of work, he is an avid tennis player, enjoys time with his wife, two sons, and their Bernedoodle, and is an auto enthusiast who loves cooking and travel.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Inc. is a technology company. Savvy Advisors, Inc. is an SEC registered investment advisor. For purposes of this article, Savvy Wealth and Savvy Advisors together are referred to as “Savvy”. All advisory services are offered through Savvy Advisors, while technology is offered through Savvy Wealth. The views and opinions expressed herein are those of the speakers and authors, and do not necessarily reflect the views or positions of Savvy Advisors.