October Highlights

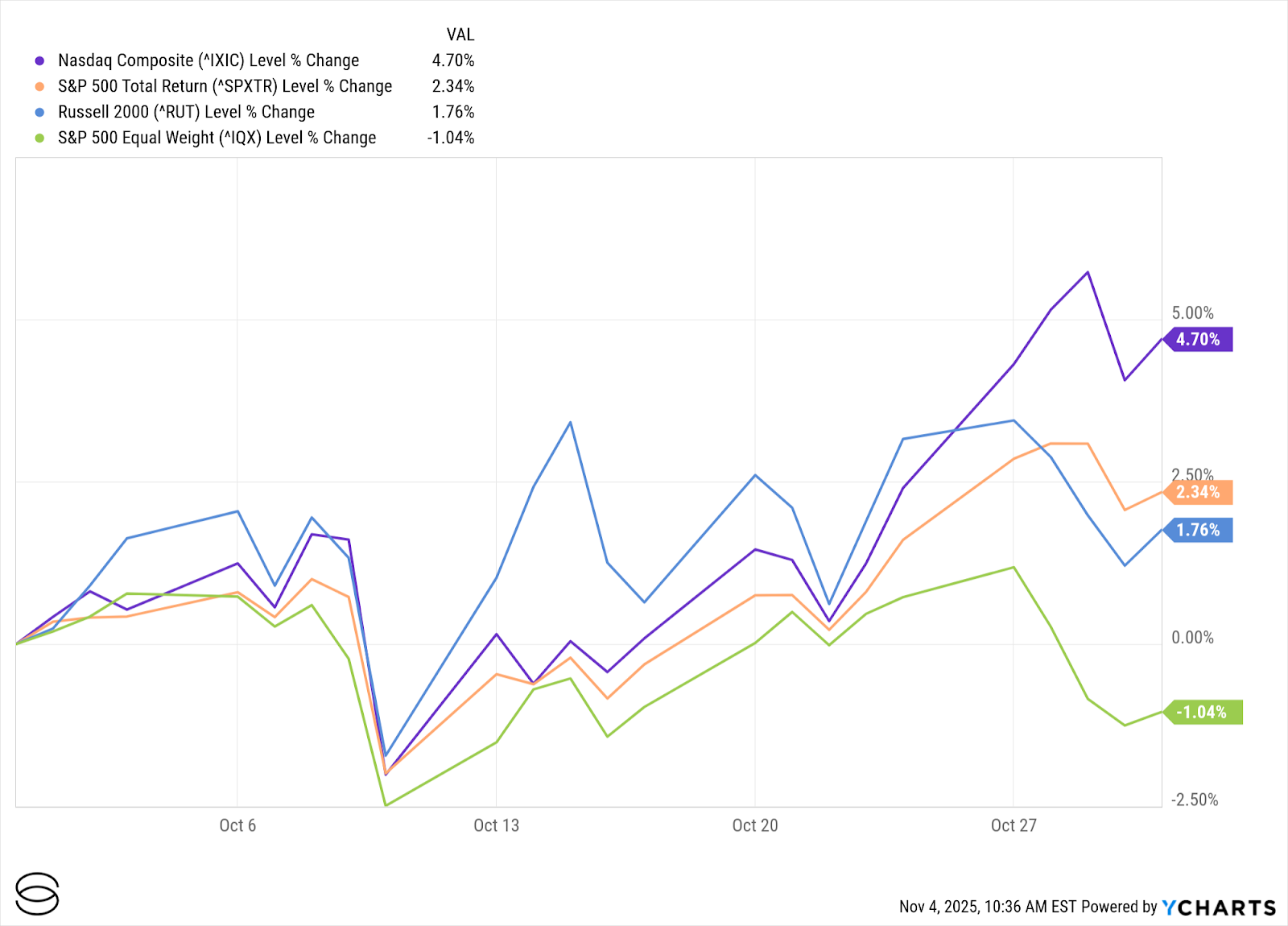

Markets extended their advance in October, fueled by broad-based, exceptional S&P 500 earnings reports, steady macroeconomic performance, and persistent investor hope for future monetary policy easing. The S&P 500 gained approximately +2.3%, while the Nasdaq rose +4.7%, notching fresh record highs for both indices.

Macro signals showed continued resilience despite a significant data vacuum. While the much-anticipated October Jobs Report was delayed due to the government shutdown, private-sector employment surveys showed a softening labor market. The most crucial official data point available was inflation: Core CPI moderated to 3.0% year-over-year (September data). While earnings resilience drove equity market gains, Gold suffered a sharp mid-month correction, and yields remain elevated in the face of uncertain policy.

Featured Theme: Corporate Earnings Flex Their Muscle

Tech Leaders and the S&P 500 Deliver Resilient Growth

The Q3 earnings season demonstrated robust corporate health, exceeding expectations across the board and confirming the durability of the earnings cycle. With nearly two-thirds of the S&P 500 having reported by month-end:

- 83% of companies beat EPS estimates, a beat ratio significantly above the 5-year average of 78% (Source: FactSet Earnings Insight, Oct 2025).

- 79% of companies beat revenue estimates, marking the highest sales surprise ratio in four years (Source: FactSet Earnings Insight, Oct 2025).

- The blended (actual and estimated) Earnings Growth Rate for the S&P 500 stood at +10.7% year-over-year, marking the fourth consecutive quarter of double-digit growth (Source: FactSet Earnings Insight, Oct 2025).

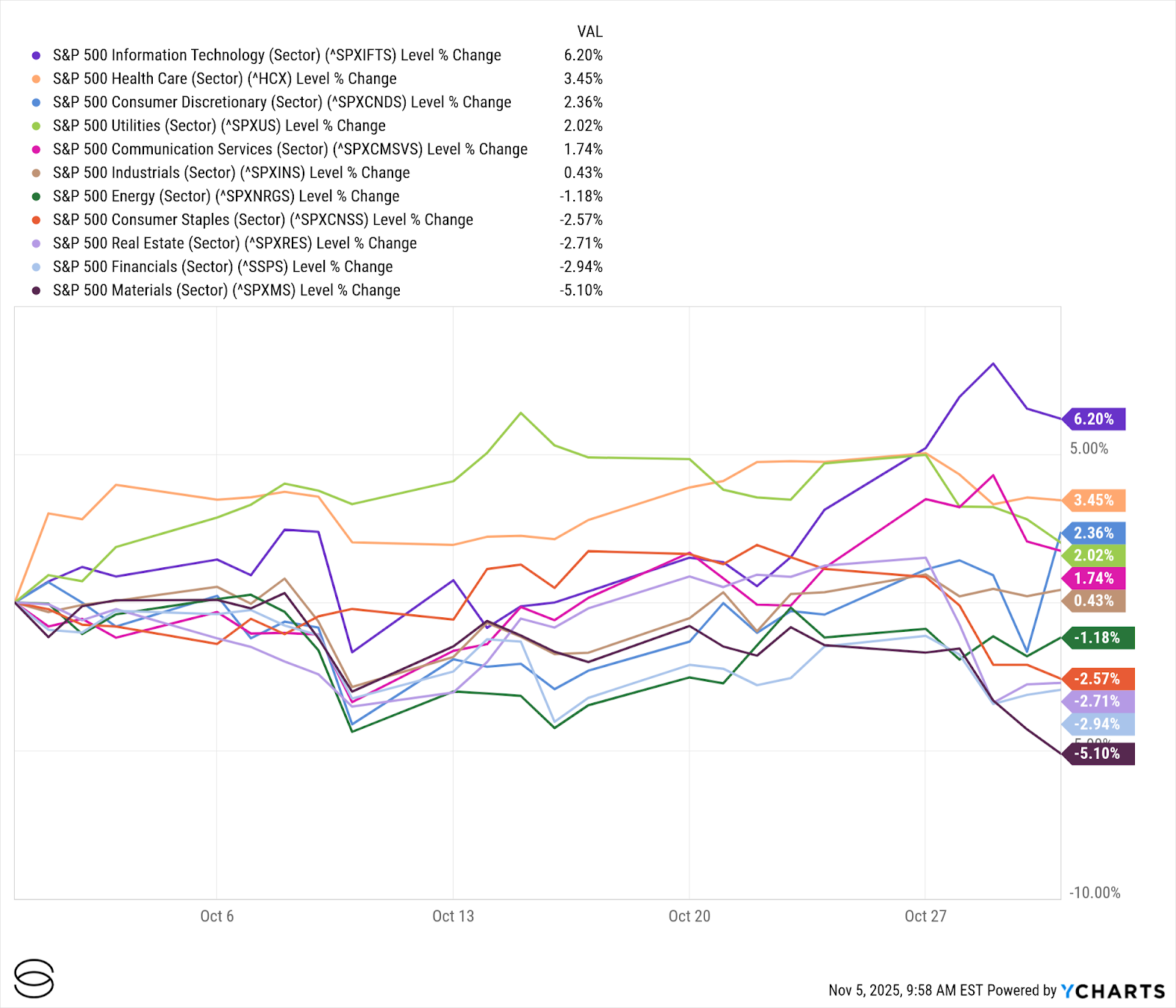

The Technology and Consumer Discretionary sectors were the largest contributors to this upside. The Magnificent Seven tech stocks again played an outsized role. Amazon’s Q3 profit came in at $1.95 per share (versus $1.57 expected), and Apple posted $1.85 EPS for its fiscal Q4. The market's positive momentum coming into the Q4 was validated by broad-based corporate profitability.

Featured Theme: Cautiously Constructive

Navigating Policy Shifts and a Historic Data Vacuum

The market's "cautiously constructive" mood was defined by a historic divergence: robust corporate earnings provided confidence, but a government shutdown-induced data vacuum severely limited visibility into the macroeconomy.

- The Scarcity of Data: While the essential September Core CPI reading of 3.0% provided a crucial inflation anchor, all major sentiment indicators were delayed (GDP, Retail Sales, PCE). This scarcity forced the Federal Reserve to navigate policy with limited visibility, making their dovish messaging all the more critical.

- Labor Market Proxy: With the official Jobs Report delayed, investors were forced to rely on secondary sources. ADP reported that private sector employment declined by 32,000 jobs in September 2025, marking the steepest drop since March 2023 and the first consecutive monthly losses since 2020. The decline was broad-based, led by significant losses in leisure and hospitality, professional business services, and financial activities. Annual pay growth for job-stayers held steady at 4.5%.

- The Soft-Landing Mandate: The available data – easing core inflation and resilient, albeit slowing, consumption – nonetheless provided the technical justification for the Fed's pivot to easing. These trends supported the view that the economy is decelerating without derailing.

- The Cautionary Note: Despite the market optimism, Consumer Confidence slipped to a two-year low of 94.6. This signaled that households were feeling pressure from accumulated inflation and high borrowing costs, providing a necessary cautionary counter-signal to the high equity valuations.

These factors together cemented the Federal Reserve’s belief that its future easing path must remain strictly data-dependent, even as market expectations for additional rate cuts shifted decisively higher.

U.S. Markets

The S&P 500 delivered its sixth consecutive monthly gain, driven by strength across tech, health care, and consumer discretionary sectors. Equal-weight S&P 500 and Russell 2000 indices underperformed mega-cap benchmarks (-1.0% and +1.8%, respectively), reversing September’s short-lived widening market breadth.

Of S&P 500 constituents reporting, about 83% surpassed EPS estimates and 79% topped revenue forecasts, reinforcing the durability of U.S. corporate profitability.

Exhibit XX: October 2025 Performance – The Return of Mega-cap Tech

Exhibit XX: October 2025 Performance – Individual GICS Sectors

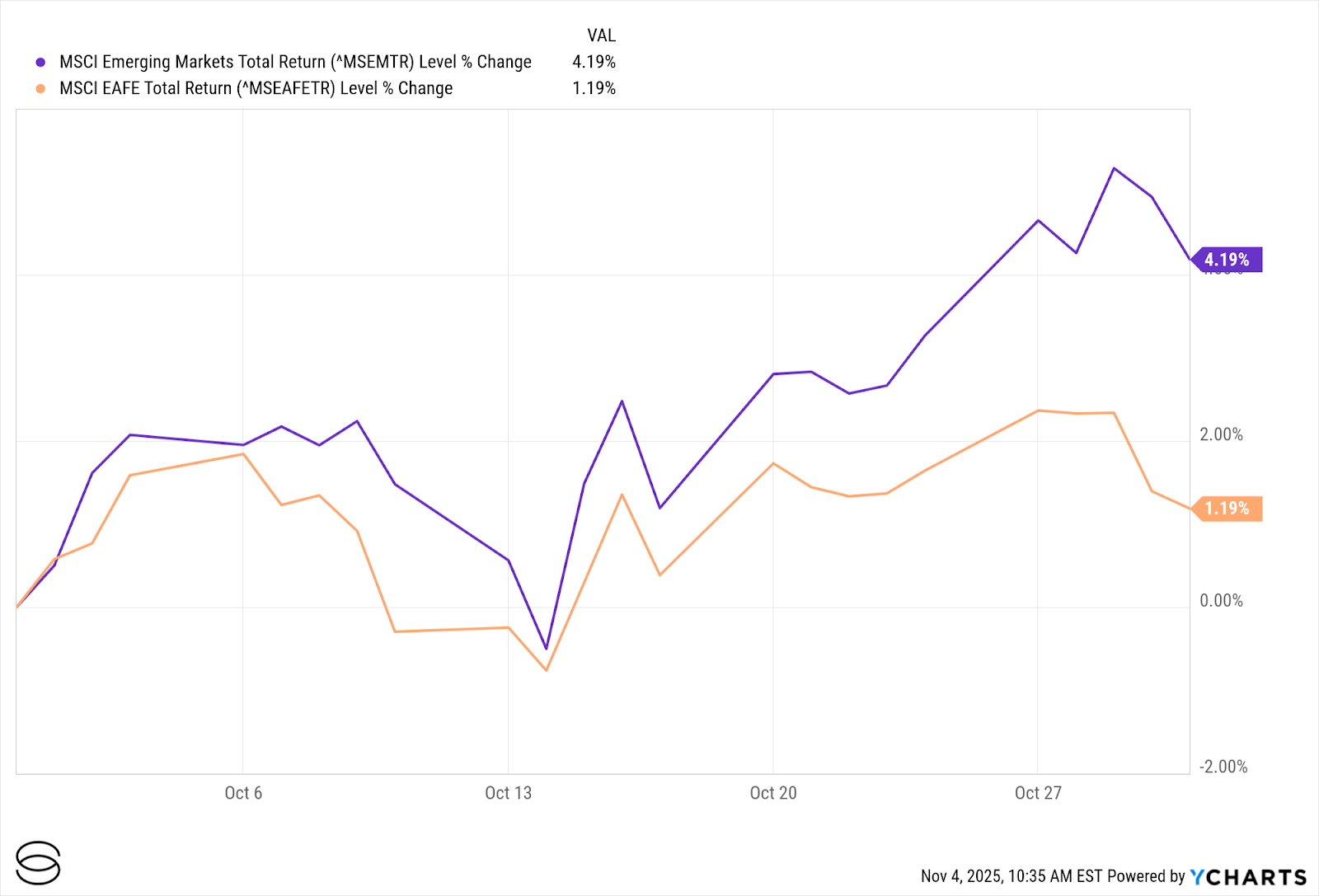

International Developed & Emerging Markets

Emerging markets led Non-U.S. returns, advancing 4.2% as Chinese stimulus chatter buoyed sentiment. Developed ex-U.S. markets lagged (1.2% for the MSCI EAFE Total Return Index) due to Europe’s industrial challenges and yen strength headwinds in Japan.

Exhibit XX: October 2025 Performance – International Equities

Cross‑Asset Performance

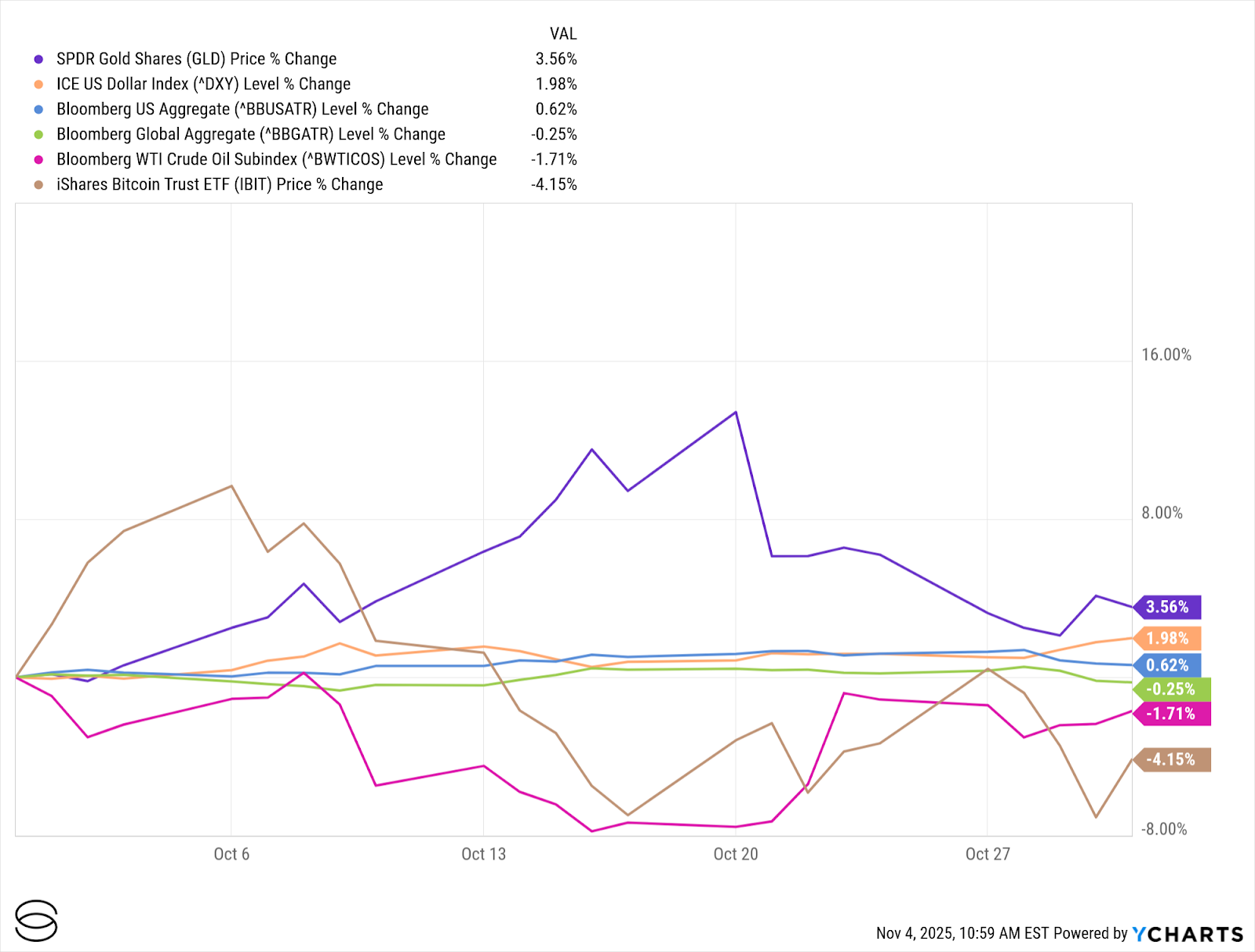

Fixed income returns were generally flat, with the Bloomberg Global Aggregate Bond Index up about +0.9% for the month. October saw ongoing volatility in interest rates: U.S. 10-year Treasury yields briefly touched 4.6% before retracing to close near 4.4%, while investment-grade corporate spreads widened and then tightened again to multi-month lows as equity volatility eased. Credit spreads also narrowed across both high-grade and high-yield bonds, reflecting renewed investor appetite for credit risk and hopes for additional rate cuts from the Federal Reserve. Despite this, global government bond sectors faced modest price pressure in developed markets, and Japanese 10-year yields rose to their highest level since 2013 amid shifting Bank of Japan guidance.

Gold experienced a dramatic, yet short-lived, reversal in October. After posting its best monthly surge in years during September, gold bullion continued to climb, hitting a fresh all-time high near $4,380 per ounce around the middle of the month. It then underwent a sharp correction, plunging over 8%% from that peak before stabilizing near $3,800/oz to end the month with a modest overall gain. We suspect this selling was driven primarily by profit-taking on technical factors together with a strengthening soft-landing narrative, which temporarily reduced the urgency for defensive assets.

Other commodities also showed weakness during October. Oil fell -1.7% on news of record U.S. shale production and concerns over weakening global industrial demand from Europe and China. Bitcoin also declined, falling -4.2% for the month.

Exhibit XX: October 2025 Performance – Fixed Income and Commodities

Economy & Policy

The U.S. government shutdown has remained in effect throughout October (now 36 days in length, at the time of writing), becoming the longest in U.S. history as Congress struggled to reach a bipartisan funding deal. This protracted closure has impacted sectors reliant on federal input and delayed the release of key government economic reports.

Inflation remains the critical wildcard, especially given the scarcity of data. The lone official inflation release available – the September Core Consumer Price Index (CPI) report—confirmed that price pressures are moderating, with a reading of 3.0% year-over-year (y/y). However, because the government shutdown delayed the release of the Personal Consumption Expenditures (PCE) Index (the Fed's preferred inflation gauge), the central bank lacked its primary tool for assessing underlying price trends. This limited visibility has complicated the Fed's decision-making, forcing it to rely on only a partial picture of the U.S. consumer and business environment.

Despite the lack of available data, the Federal Reserve cut rates by 25 bps to a target range of 3.75% - 4.00% at its October meeting, citing “uncertainty about the economic outlook” and elevated risks to employment. Additional cuts were signaled as a possibility, but divided opinions on the committee – and persistent inflation – could keep the rate path more clouded than markets expect.

Trade tensions and tariff concerns lingered in the headlines. Although a breakthrough on a few major sticking points between the U.S. and China was announced toward the end of the month (e.g., retaliatory tariffs, agricultural commodities, and rare earth elements). Legal challenges to the Executive Branch’s tariff authority remained pending in the courts.

Policy Watch: Reverse Repo Flows and Liquidity

Sizable Repo Flows Signal Liquidity Reallocation

A major liquidity event unfolded at month-end on October 31st, when the Federal Reserve’s reverse repo and standing repo markets saw record activity. Many banks and money market funds scrambled for cash to meet month-end and quarter-end obligations and regulatory requirements. The rules require them to show sufficient assets and liquidity on their books at the end of each reporting period.

Put simply, banks borrowed nearly $50 billion overnight from the Fed while large institutional investors simultaneously put about $52 billion on deposit. Normally, these flows balance out, but this time the amounts were unusually large, and short-term interest rates spiked above the Fed’s usual range.

The cause for this was straightforward. Major players needed quick cash for reporting, and not enough was circulating in the system because ongoing “quantitative tightening” has been pulling liquidity. The result was a brief but notable cash crunch.

The Fed’s backstops worked as intended, markets stayed orderly, and conditions normalized quickly once month-end pressure had passed.So, while headlines flagged this as a sign of market stress, what really happened is much more typical: it’s like lots of people rushing to the ATM on payday, and the bank making sure there’s enough cash available. Ultimately, this episode showed the Fed’s tools worked as intended to keep the financial system steady, even when liquidity got tight for a day or two.

What to Watch Next

- Nov 5: October Jobs Report – crucial for Fed timing.

- Nov 12: November CPI/Core CPI – will inflation cool or persist?

- Nov 14: Retail Sales & Consumer Confidence – signs of consumer fatigue?

- Mid-November: Q3 Corporate Earnings Season concludes.

- Ongoing: Trade/tariff developments, U.S.-China relations, fiscal/macro policy.

Bottom Line

October proved the market's underlying resilience, showing it could thrive on strong earnings even when faced with a policy-driven data blackout. While the rally remains robust, the month signaled critical risks to manage: sticky inflation and political gridlock. The sharp correction in gold and the widening consumer confidence gap remind us that systemic risks have not vanished. Heading into Q4, we advocate for balanced diversification—leaning into sectors with demonstrated earnings visibility while prioritizing liquidity and credit quality in fixed income to guard against potential volatility.

Anshul Sharma is Chief Investment Officer at Savvy Wealth, where he oversees the firm’s investment strategy, portfolio design, and platform innovation. He partners across product, marketing, and operations teams to deliver portfolios that take a methodological approach to balance customization with scalability for advisors and their clients. Before joining Savvy, Anshul spent nearly two decades at Bank of America, where he managed the Chief Investment Office’s Sustainable Model Portfolio Suite, launched new proprietary offerings, and, as Head of Alternative Investment Strategy, provided guidance and thought leadership to advisors around hedge fund, private market, and real asset strategies. He began his career as an Investment Strategist at U.S. Trust, designing multi-asset portfolios for high-net-worth and institutional clients. Anshul holds a Master of Financial Engineering from UC Berkeley and a Bachelor of Computer Engineering from Lehigh University. Outside of work, he is an avid tennis player, enjoys time with his wife, two sons, and their Bernedoodle, and is an auto enthusiast who loves cooking and travel.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Inc. is a technology company. Savvy Advisors, Inc. is an SEC registered investment advisor. For purposes of this article, Savvy Wealth and Savvy Advisors together are referred to as “Savvy”. All advisory services are offered through Savvy Advisors, while technology is offered through Savvy Wealth. The views and opinions expressed herein are those of the speakers and authors, and do not necessarily reflect the views or positions of Savvy Advisors.