The third quarter capped off a strong stretch for global markets, with major equity indices climbing to record highs. Resilient economic data, strong corporate earnings, and ongoing AI enthusiasm helped fuel the rally, while a notable shift in market leadership signaled growing confidence in the recovery. Inflation and tariff concerns remained in focus, but monetary easing and a revival in deal activity helped drive positive momentum across asset classes.

Exhibit 1: Positive momentum across asset classes in Q325

Featured Theme: Market Leadership Broadens – Rotation and Opportunity

The defining theme for Q3 was the broadening of market performance. After early-year dominance by mega-cap tech and AI leaders, gains spread to small-caps, materials, cyclical sectors, and international equities. This shift reflects changing investor psychology – from chasing winners to favoring selective, value-driven allocations as the economic backdrop stabilized.

Small-cap and cyclical rallies followed the Fed’s rate cut and receding trade frictions. International developed and emerging market stocks outperformed U.S. large caps, supported by a weaker dollar and accelerating capital flows. This broadening environment signals a maturing bull market and reinforces the merits of diversified, multi-asset allocations heading into Q4.

U.S. Equities

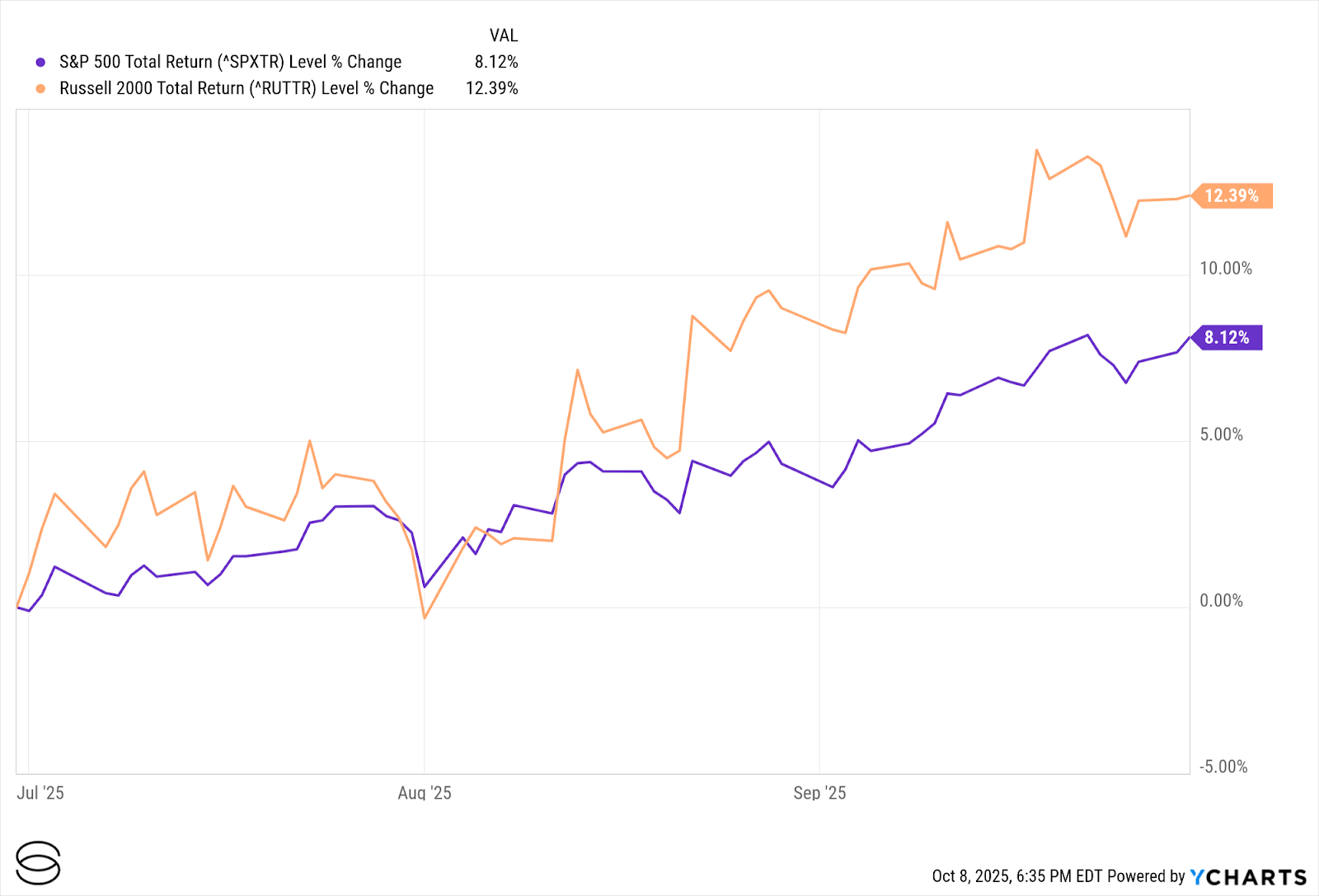

Major indices delivered impressive gains: Nasdaq surged +11.2%, S&P 500 +8.1%, Dow +5.2%, each reaching new all-time highs. While tech and communication services contributed, the standout was a leadership transition toward small caps (+12.4%) and cyclicals. The Fed’s September rate cut provided further momentum for risk assets and economic expansion.

Exhibit 2: Small cap takes the lead in Q3

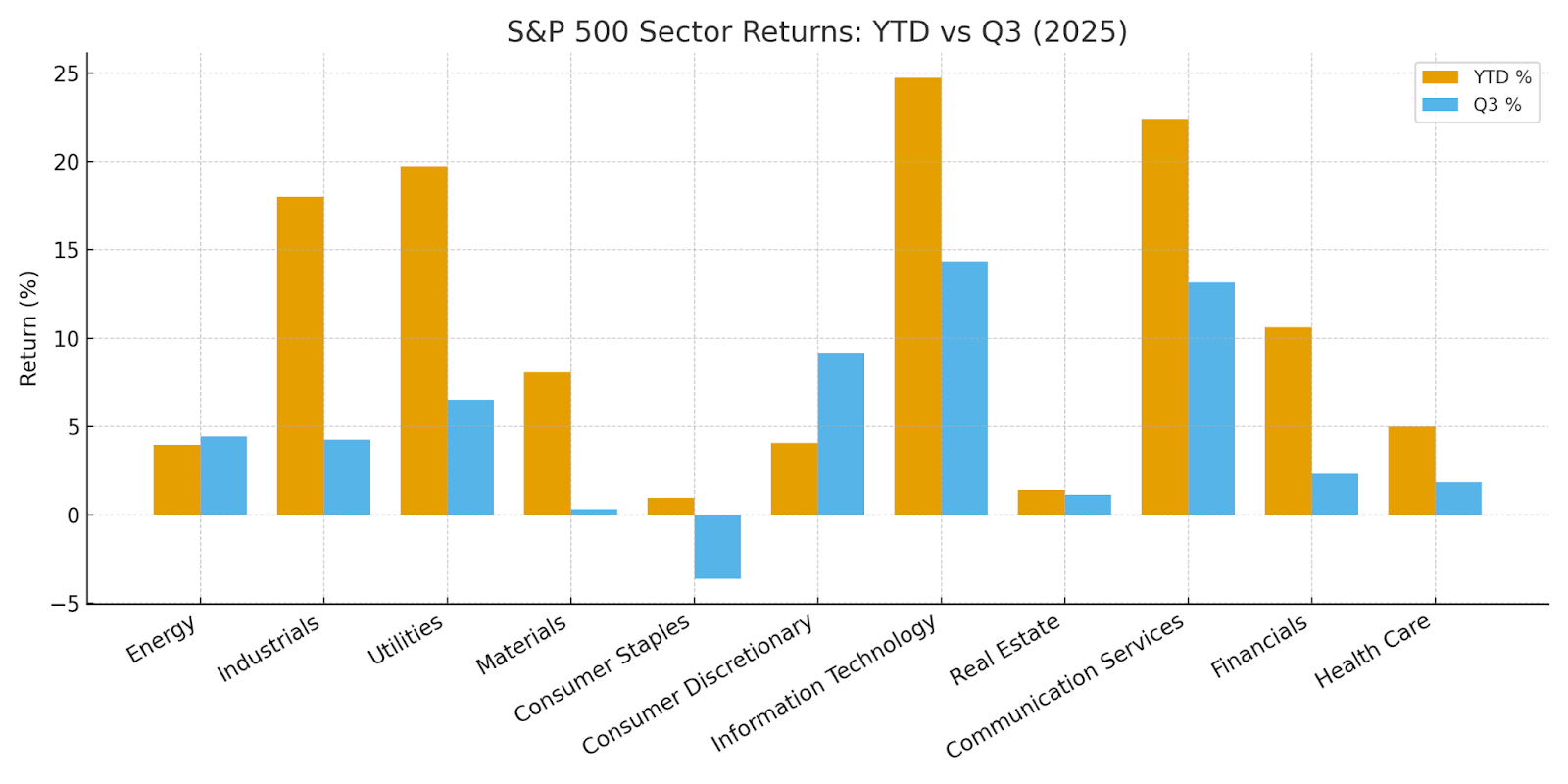

Exhibit 3: Bar chart of sector returns (YTD through Sept and Q3 2025)

M&A and Corporate Strategy: Deals Are Back

Corporate dealmaking resurged, topping $1 trillion in Q3, with large-cap tech, private equity, and strategic industrials at the forefront. Boards appeared more comfortable allocating capital for structural growth, scale, and supply chain flexibility. This trend supports the positive earnings narrative and indicates open access to capital.

Exhibit 4: Notable M&A Deals in Q3 2025

Cross-Asset Performance

Bonds posted modest gains in Q3, with the Bloomberg Global Aggregate Index rising 0.6% as falling yields and the Fed’s September rate cut supported fixed income broadly. Investment-grade credit outperformed slightly, helped by healthy demand and tightening spreads.

Commodities diverged: gold surged 17% to record highs above $3,800/oz, driven by geopolitical risk and central bank demand, while oil dipped 0.8% amid mixed supply signals. Bitcoin rallied 5.5% as institutional interest and regulatory clarity boosted sentiment.

The quarter rewarded diversified portfolios, with credit, hedges, and select real assets playing a constructive role.

International & Emerging Markets

Emerging markets (+11%) led developed markets (+7.4%), driven by AI momentum and thawing trade relations, especially in China. Performance varied across developed markets: European equities lagged due to manufacturing headwinds (notably Germany), despite resilience in Spain and Poland; Japanese equities wrestled with yen strength. These patterns underscore the importance of selective global allocation.

Economics & Policy

Global growth remains resilient, with the International Monetary Fund (IMF) revising its 2025 outlook upward to 3.0%, supported by improved policy settings and positive surprises in several economies. Importantly, in September the Federal Reserve delivered its first interest rate cut since Dec-2024 – lowering the federal funds rate by 25 basis points to a target range of 4.00%–4.25% – as policymakers responded to signs of a softening labor market and slowing economic momentum.

Consumer spending, which rose 0.6% in August after a flat July, remains a key growth engine but is beginning to show early signs of caution – especially in discretionary categories1. With mortgage rates still averaging 6.4–6.5% and the Conference Board’s Consumer Confidence Index dropping below 95 in September (lowest level since April 2025), households may be tightening budgets and prioritizing essentials over nonessential purchases.

Abroad, Europe and China remain subdued, but the consensus does not signal imminent recession, supporting the “soft-landing” narrative: below-trend yet resilient growth, vulnerable to shocks.

Geopolitics

U.S.-China negotiations, ongoing Middle East tensions, and persistent hostilities in Ukraine continued shaping market sentiment. Easing trade frictions and new bilateral agreements created tactical opportunities, while elevated demand for safe-haven assets highlighted remaining uncertainties.

Looking Ahead

Markets enter Q4 with positive momentum from central bank action, strong earnings, and broader participation. Nonetheless, fiscal, tariff, and geopolitical risks will keep volatility elevated. Disciplined risk management and broad diversification remain essential as upcoming data clarify the outlook.

What We’re Watching Heading Into Q4

- Potentially Slowing Economic Growth: Activity is moderating in the U.S. and globally, with softer consumer spending as higher borrowing costs and cautious sentiment persist, especially heading into the holiday season. Growth in Europe and China is subdued. While below-trend, a sharp downturn is not expected.

- Sticky Inflation and Policy Response: Inflation has moderated but remains vulnerable in the near-term to new tariff shocks. The Fed is expected to continue easing rates, though persistent core inflation and global price pressures may limit flexibility.

- Monetary and Fiscal Dynamics: Monetary easing is expected but could underwhelm market hopes. Fiscal stimulus supports growth, but deficits remain a concern for major developed economies.

- Market Valuations and Concentration Risk: U.S. equity market valuations are high compared to historical levels and concentrated in mega-cap tech; smaller caps offer better value but carry risk if market leadership falters.

- Long-Term Bond Yields and Credit: Higher yields affect borrowing and sentiment, even as monetary policy eases. Credit remains resilient but merits continued monitoring.

- Tariffs, Trade, and Geopolitics: High uncertainty persists around tariffs and international policy. Geopolitical frictions or escalations could disrupt supply chains or risk appetite.

- Housing and Real Estate: Low turnover, elevated mortgage rates, and sluggish building are key cyclical checks.

- Earnings, Guidance, and Holiday Season: Q3 earnings guidance and Q4 consumer confidence are critical. Misses in guidance or weak holiday sales could provoke swift market response.

Important October Dates

October will be eventful – some releases may be delayed by the U.S. government shutdown. Watch for:

- Oct 3 – September Jobs Report: NFP, Unemployment Rate, Labor Force Participation, Avg Hourly Earnings

- Oct 15 – September CPI/Core CPI: Shelter, Energy & Food

- Oct 16 – Retail Sales: Headline/Core, GDP Control Group

- Oct 17 – Housing Starts & Permits: Detailed MoM/unit breakdown

- Oct 30 – Q3 Advance GDP (First Estimate)

- Oct 31 – September PCE Inflation: Headline/Core PCE, Personal Income, Spending

- Mid-October – Q3 Earnings Season Kickoff: Major banks/tech report. Earnings guidance will be key: reaffirmed outlooks could extend gains, but misses may be punished quickly.

Bottom Line

Q3 2025 reinforced a constructive risk environment with expanding market breadth, resilient economic trends, and evolving policy dynamics. The coming quarter will be pivotal in determining the durability of the “soft-landing” narrative and the sustainability of broad-based market strength.

Anshul Sharma is Chief Investment Officer at Savvy Wealth, where he oversees the firm’s investment strategy, portfolio design, and platform innovation. He partners across product, marketing, and operations teams to deliver portfolios that take a methodological approach to balance customization with scalability for advisors and their clients. Before joining Savvy, Anshul spent nearly two decades at Bank of America, where he managed the Chief Investment Office’s Sustainable Model Portfolio Suite, launched new proprietary offerings, and, as Head of Alternative Investment Strategy, provided guidance and thought leadership to advisors around hedge fund, private market, and real asset strategies. He began his career as an Investment Strategist at U.S. Trust, designing multi-asset portfolios for high-net-worth and institutional clients. Anshul holds a Master of Financial Engineering from UC Berkeley and a Bachelor of Computer Engineering from Lehigh University. Outside of work, he is an avid tennis player, enjoys time with his wife, two sons, and their Bernedoodle, and is an auto enthusiast who loves cooking and travel.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Inc. is a technology company. Savvy Advisors, Inc. is an SEC registered investment advisor. For purposes of this article, Savvy Wealth and Savvy Advisors together are referred to as “Savvy”. All advisory services are offered through Savvy Advisors, while technology is offered through Savvy Wealth. The views and opinions expressed herein are those of the speakers and authors, and do not necessarily reflect the views or positions of Savvy Advisors.

Sources:

1. U.S. Bureau of Economic Analysis, as of Sept. 2025