Retail Leverage, Market Fragility, and the Risk of a Sudden Turn

Irrational Exuberance in the Modern Market

On December 5, 1996, then–Federal Reserve Chair Alan Greenspan posed a question that still echoes through financial markets:

“But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions…?”

Back then, Greenspan’s words seemed premature. Stocks climbed for years before the dot-com bubble burst. But when that reversal came, it wiped out trillions in paper wealth and altered the market’s course for a decade.

Fast-forward to today. The forces at work are larger, faster, and more interconnected than ever. Record household exposure to equities, extreme leverage, stretched valuations, and a culture of speculative trading have created an environment where even small shocks could have outsized consequences.

The Wealth Effect and the 12% Threshold

The “wealth effect” — the tendency for people to spend more when their investments and home values rise — works in both directions. Rising markets lift confidence and spending; falling markets can cut both sharply.

Federal Reserve research suggests that for U.S. households, a decline of roughly 12% in the stock market is enough to meaningfully slow consumer spending. Once losses reach that level, fear of further declines often kicks in, accelerating both market selling and cutbacks in everyday purchases.

That risk is amplified today. According to Gallup’s May 2025 survey, 62% of Americans now own stocks (directly or through retirement accounts) — matching the highest ownership rate seen before the Great Recession. A meaningful market pullback today wouldn’t just be a Wall Street problem; it would quickly reach Main Street.

Layers of Risk — Seen Over Time

The warning signs aren’t isolated; they overlap.

Leverage is extreme. Margin debt has surpassed $1 trillion, the highest level on record.1 While leverage magnifies gains in rising markets, it can also accelerate losses. Forced selling from margin calls can quickly turn a mild pullback into a sharp sell-off.

Housing is stretched. Home prices relative to incomes are near record highs, while mortgage rates remain at multi-decade peaks, putting ownership out of reach for many. According to Redfin’s April 2025 data, there are 490,000 more sellers than buyers, the largest gap since records began in 2013.

Source: Redfin Housing Market Report, April 2025; HousingWire, May 2025.

Redfin CEO Glenn Kelman put it plainly in September 2023:

“When the market shifts, there can be more sellers than buyers overnight — and that’s when prices start to move fast.”

Fiscal deficits are entrenched. The U.S. budget deficit now exceeds 6% of GDP despite a strong labor market.2 The Congressional Budget Office projects deficits above 5% of GDP for the next decade — levels rarely seen outside of recessions or wars.3 This chronic overspending drives heavy Treasury issuance, pushing rates higher and leaving less fiscal room to respond in a downturn.

When housing — the largest single asset for most Americans — and equities both stumble, the negative wealth effect can ripple quickly through the broader economy.

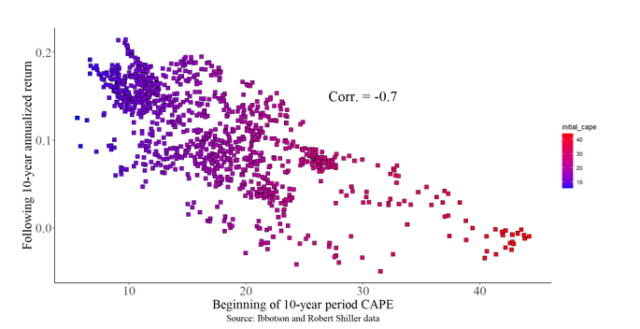

Valuations Are Extreme — The Buffett Indicator Speaks

The Shiller CAPE ratio sits near 38, a level reached only in 1929 and 1999. Historically, such peaks have led to inflation-adjusted 10-year returns of just 1% annually.

Source: CFA Institute, April 17, 2024.

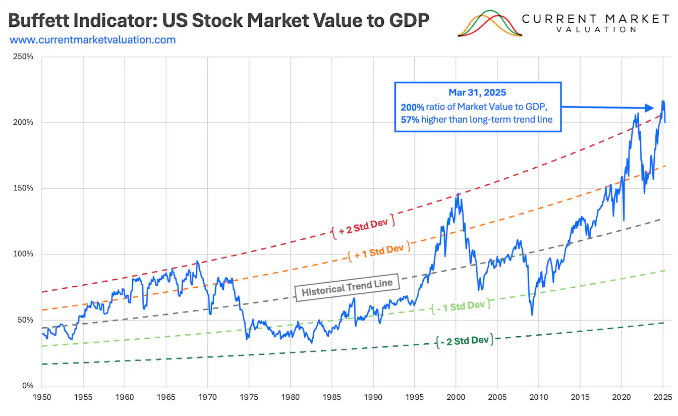

The Buffett Indicator, which compares the total U.S. stock market value to GDP, tells a similar story. In a 2001 Fortune interview, Warren Buffett called it “probably the best single measure of where valuations stand at any given moment.”

- 70–80% → market is cheap

- Over 100% → expensive

- Over 200% → “playing with fire”

Today, it’s around 200%, a level exceeded only in 2021 and the dot-com peak. At similar points in history, forward returns have been weak, and drawdowns severe.

Buffett’s own positioning underscores the risk: as of Q2 2024, Berkshire Hathaway held $277 billion in cash, over 30% of its market cap — its largest cash pile ever.

Source: CurrentMarketValuation.com, March 31, 2025.

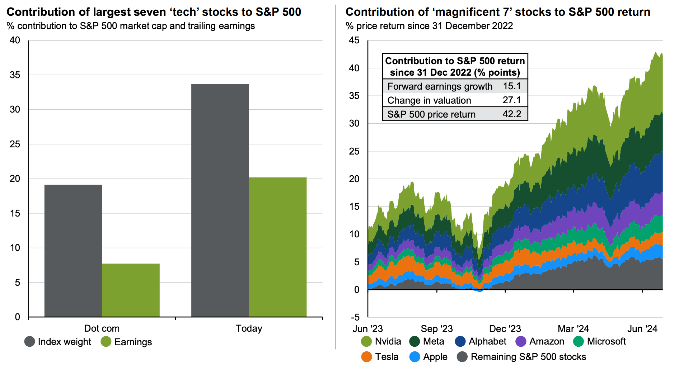

The S&P 500’s Narrow Base

Despite its name, the S&P 500 is far from broad-based. The Magnificent 7 — Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta, and Tesla — now account for 35.4% of the index as of August 2025, nearly triple their combined share in 2015.

Source: J.P. Morgan Guide to the Markets via JustETF, late 2024.

Bank of America’s Michael Hartnett warns:

“When market breadth is this narrow, the market’s leadership is less a sign of broad confidence and more a sign of crowding — and crowded trades tend to unwind violently.”

The Gamification of Investing

Investing today is faster, louder, and more speculative. Zero-commission apps, fractional shares, and social media hype have turned markets into something resembling a casino floor, where speed and excitement often outweigh fundamentals.

In 2021, GameStop’s meteoric rise — more than 1,500% in weeks — was driven not by earnings but by online memes and a rallying cry of “to the moon.”5 As The New York Times reported on January 27, 2021:

“The phrase ‘to the moon’ became a rallying cry for the legions of day traders pushing up the price of GameStop and other stocks.”

One reason speculative behavior has lasted so long is the longest credit expansion in U.S. history. Years of ultra-low rates and pandemic stimulus have kept liquidity abundant, suppressing volatility and reinforcing a buy-the-dip mindset.

Why Small Drops Can Become Big Ones

Market declines often start small. A 3% dip becomes 6%, then 12% — the threshold where the wealth effect starts to bite and selling pressure accelerates.

In today’s leveraged, concentrated market, even isolated events can have an outsized impact. Last week, Eli Lilly (LLY) — a $600+ billion blue-chip — plunged nearly 14–18% after disappointing trial results for its obesity drug orforglipron.5 Despite reporting Q2 revenue growth of 38% and beating earnings expectations, the drug’s results fell short of investor hopes, erasing over $150 billion in market value in weeks.

If a company of Lilly’s size can lose that much, that fast, the implications for a narrow, crowded market are obvious. Once confidence cracks, forced selling, ETF outflows, and evaporating liquidity can turn a manageable decline into a rout.

Full Circle: From Exuberance to Caution

Greenspan’s question from 1996 — how do we know when exuberance has gone too far? — is as relevant today as ever.

Technology, passive flows, and gamified speculation make cycles faster and more interconnected. The wealth effect means even modest declines can quickly spill into the real economy.

And with valuations stretched, market leadership narrow, and the credit cycle at historic length, the room for error is razor-thin.

As Buffett warned in 2001:

“Only when the tide goes out do you discover who’s been swimming naked.”

Right now, the tide is high — but history shows it can recede without warning.

I'm Joshua, a financial advisor from Reno, Nevada. As someone who co-founded and built a trust company and investment advisory firm from the ground up, I’m passionate about sharing the lessons I've learned on my financial journey of 30+ years to guide and empower clients to secure their financial futures. Using active macroeconomic quantitative and tax avoidance strategies, I mitigate risk and help families achieve lasting financial independence, acting as guardians for future generations. Trust, consistency, and accessibility are at the heart of all my long-lasting client relationships.

Joshua Barone is an investment advisor representative with Savvy Advisors, Inc. (“Savvy Advisors”). Savvy Advisors is an SEC registered investment advisor. Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy. All investments involve risk, including loss or principal investment.

Ancora West Advisors, LLC dba Universal Value Advisors (“UVA”) is an investment advisor firm registered with the Securities and Exchange Commission. Savvy Advisors, Inc. (“Savvy Advisors”) is also an investment advisor firm registered with the SEC. UVA and Savvy are not affiliated or related.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy. All investments involve risk, including loss of principal. Alternative investments and private placements involve a high degree of risk and can be illiquid due to restrictions on transfer and lack of a secondary trading market. They can be highly leveraged, speculative and volatile, and an investor could lose all or a substantial amount of an investment. Alternative investments may lack transparency as to share price, valuation and portfolio holdings. Prospective investors are advised that investment in a private fund or alternative investment strategy is appropriate only for persons of adequate financial means who have no need for liquidity with respect to their investment and who can bear the economic risk, including the possible complete loss, of their investment. All advisory services are offered through Savvy Advisors, Inc., an investment advisor registered with the Securities and Exchange Commission (“SEC”).

Reference:

1 https://www.barrons.com/advisor/articles/investor-margin-trading-white-hot-market-45278699

2 https://bipartisanpolicy.org/blog/visualizing-cbos-budget-and-economic-outlook-2025/

3 https://www.crfb.org/papers/analysis-cbos-march-2025-long-term-budget-outlook