Employee Benefits for Your Business: SEP or SIMPLE IRAs?

SEP vs. SIMPLE IRA plans are typically compared with traditional 401(k) options, particularly for small businesses looking to offer meaningful retirement benefits without the high costs or paperwork. Retirement plans have become an increasingly valuable part of employee benefits, with more companies recognizing the need to remain competitive in attracting and keeping workers.

Statistics show that only 54% of employees working at businesses with fewer than 50 workers had access to a defined contribution plan in 2024, compared to 47% in 2020. This highlights the growing adoption among small businesses. SEP and SIMPLE IRAs stand out as accessible and flexible ways to provide retirement savings, offering tax advantages and a straightforward setup for employers.

In this article, you’ll learn:

- SEP IRAs are funded only by employers, with high contribution limits (up to $70,000 or 25% of pay in 2025) and flexibility to change contributions each year.

- SIMPLE IRAs allow both employer and employee contributions, require annual funding, and include new “super” catch-up contributions for workers ages 60–63 under SECURE 2.0.

- Eligibility: SEP IRAs require employees to be 21+, earn at least $750, and have worked three of the last five years; SIMPLE IRAs are for businesses with ≤100 workers.

- Setup and administration are easier than 401(k)s—SEP IRAs need no annual IRS filing, while SIMPLE IRAs require yearly employee notices.

- Tax benefits: Both offer deductible contributions and tax-deferred growth, with SECURE 2.0 providing valuable startup and contribution credits for small businesses.

- When to choose a SEP IRA: If income is unpredictable and you want employer-only control.

- When to choose a SIMPLE IRA: If you want steady employer contributions and active employee participation.

- Best practices include tracking deadlines (Oct. 1 setup for SIMPLE IRAs, tax deadline for SEPs), giving employee notices, and keeping clear records.

What Are SEP and SIMPLE IRAs?

A simplified employee pension (SEP) IRA is a retirement plan funded only by the employer. It allows for higher contributions compared to other small business options. This makes it appealing for owners who desire flexibility in how much they contribute every year.

A SIMPLE IRA, or Savings Incentive Match Plan for Employees, is designed for businesses with 100 or fewer workers. Both the employer and employees can contribute, giving workers more control over their own retirement savings.

Like a 401(k), SEP and SIMPLE IRAs are IRS-qualified plans that grow tax-deferred until withdrawal, offering a simple way for small businesses to provide retirement benefits.

Related Article: IRA vs. 401(k): A Comparison of Retirement Savings Vehicles

How SEP IRAs Work for Employers

A SEP IRA gives you a way to provide retirement savings without a complicated setup. Contributions come only from the employer, and the plan rules are straightforward. Below, we’ll look at contribution limits, who qualifies, and how to set one up.

Contribution Limits and Rules

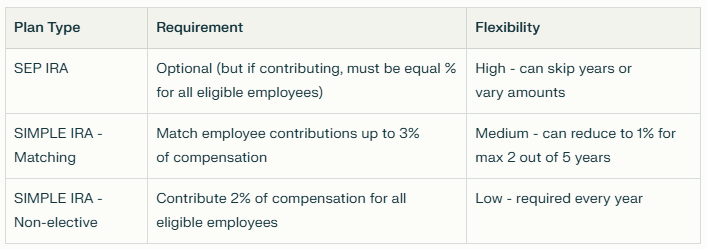

A SEP IRA has some of the highest contribution limits of any small business retirement plan. For 2025, the maximum contribution is $70,000 or 25% of an employee’s compensation, whichever is less. Contributions are only funded by the employer, as employees cannot add their own money. Whenever a contribution is made, the employer must give the same percentage of pay to all eligible employees. This setup makes SEP IRAs especially useful for self-employed individuals and those who want flexibility in how much they contribute every year.

SIMPLE IRAs, on the other hand, allow employee contributions and now include “super” catch-up contributions for workers ages 60-63 under the SECURE 2.0 Act, offering $5,250 instead of the standard catch-up amounts.

Eligibility Requirements

To qualify for a SEP IRA, employees must meet a few basic rules. They need to be at least 21 years old, earn $750 or more in competition, and have worked for the business in at least three of the last five years. These requirements also apply to part-time and seasonal workers, which means more employees are often included than with other plans. Employers can make the rules more lenient, such as lowering the minimum age, but they cannot make them stricter.

Setup and Administration

Setting up a SEP IRA is simple. Employers can use IRA Form 5305-SEP or a financial institution’s version to begin. One advantage is that there are no annual IRS filings or nondiscrimination tests, which keeps ongoing work to a minimum. Contributions, however, do need to be recorded and shared with employees so everyone knows what was added to their accounts. This balance of flexibility and low paperwork makes the SEP IRA a good option for many small businesses.

Related Article: Individual Retirement Accounts (IRAs): What They Are and How to Open One

SEP vs. SIMPLE IRA: Key Differences

When weighing a SEP vs. SIMPLE IRA, it’s good to look at how the two compare side by side. Both are easier to manage than a 401(k), but they differ in how contributions are made, the flexibility employers have, and the tax credits available for small businesses.

Contribution Flexibility

One of the most significant differences between a SEP IRA and a SIMPLE IRA is how contributions are handled. With a SEP IRA, only the employer contributes, and they can decide each year if they want to contribute and how much. This makes it a good choice for those with variable income. By contrast, a SIMPLE IRA requires the employer to contribute annually, either by matching employee contributions up to 3% of pay or by giving a flat 2% contribution for all eligible workers. Employees also get to choose how much of their own pay they want to defer into the plan.

Tax Benefits and Credits

Both SEP and SIMPLE IRAs offer tax-deductible contributions for employers and tax-deferred growth for employees. These plans also benefit from recent changes under the SECURE Act 2.0, which expanded credits for small businesses. Eligible companies with 50 or fewer employees can now receive a 100% tax credit, up to $5,000 annually for three years, to cover retirement plan startup costs. On top of that, they might receive up to $1,000 per employee in credits for employer contributions during the first two years. These provisions make SEP and SIMPLE IRAs cost-effective ways for small businesses to offer retirement benefits while taking advantage of meaningful tax savings.

Related Article: Your Guide to Small Business Taxes for Beginners

Which Plan is Best for You?

Both SEP and SIMPLE IRAs give you a practical way to provide retirement benefits, but the best choice depends on your income patterns, employee needs, and how much control you want over contributions. Below, we’ll break down when each plan makes sense.

Choose a SEP IRA If…

A SEP IRA is a good fit if you’re self-employed or run a small business where income isn’t always consistent. You decide how much to contribute each year. You have flexibility during lean years and can contribute more when revenue is strong. This option also works well for owners who want complete control over funding retirement benefits without employee contributions.

A 2023 study of 703 small businesses found that 46% offered retirement plans while 54% did not. The two main obstacles were revenue stability/business size concerns and perceived administrative costs.

Choose a SIMPLE IRA If…

A SIMPLE IRA is often the better choice if you want employees to actively contribute toward their retirement. It also provides predictable employer obligations because you’ll be required to either match employee contributions or give a flat 2% contribution. This makes it a simple plan for those with a steady income who prefer a “set it and forget it” approach once that plan is in place.

Best Practices for Setup and Compliance

Once you’ve chosen a SEP or SIMPLE IRA, you need to follow the correct steps and stay consistent with deadlines. These plans are simple to maintain, but missing a key date or forgetting employee notices can create avoidable problems.

Implementation Timeline

The deadlines for setting up each plan are different. A SEP IRA can be opened and funded by your business’s tax filing deadline, including extensions. A SIMPLE IRA, on the other hand, must be set up by October 1st of the year you want it to start. Beyond setup, employers need to keep track of payroll, schedules, contribution deposits, and employee notices so they stay on track every year.

Avoiding Frequent Oversights

Even though SEP and SIMPLE IRAs are straightforward, problems still happen. With a SEP IRA, one of the most frequent issues is excluding eligible employees or missing the funding deadline. For SIMPLE IRAs, employers sometimes forget the annual employee notice or miscalculate the matching percentage. Across both plans, poor documentation or using the wrong forms also causes trouble. Keeping clear records and setting reminders for deadlines keeps the plan running well.

SIMPLE vs. SEP for Small Business Retirement Planning

Choosing between a SIMPLE IRA and a SEP IRA comes down to how you earn money, how involved you want employees to be, and how predictable you’d like contributions to be. Both options give you a way to offer retirement benefits without the higher costs and administration of a 401(k).

Key Takeaways:

- A SEP IRA is funded only by the employer and offers high contribution limits with year-to-year flexibility.

- A SIMPLE IRA allows both employer and employee contributions, with required annual funding.

- Both plans are IRS-qualified, tax-deferred, and easier to manage than a traditional 401(k).

- SECURE Act 2.0 tax credits make these plans even more attractive for small businesses.

- The best choice depends on your income patterns, business size, and goals for employee participation.

Next Steps:

- Review your business income to decide if flexibility or predictability is more important.

- Compare your workforce size and growth plans to ensure you choose the plan that fits long-term.

- Talk with a financial advisor or tax professional to understand how each plan impacts your taxes.

- Consider setting up reminders for contribution deadlines and employee notices so you’re always compliant.

Ready to decide between a SEP or SIMPLE IRA? Connect with Savvy Wealth today to explore your options and choose a retirement plan that fits both your business and your employees’ future.

Brian Jellig, CFP® is a Principal Wealth Advisor from San Diego, California, specializing in retirement portfolio strategies and income planning. His passion lies in simplifying the complexities of investments, finances, and retirement for his clients. After working with clients for almost ten years, he loves the journey of helping them endeavor to reach financial success for their families.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy. All advisory services are offered through Savvy Advisors, Inc. (“Savvy Advisors”), an investment advisor registered with the Securities and Exchange Commission (“SEC”).

Works Cited