AI Is Quietly Creating Disinflation/Deflation in the U.S. Economy

The Quiet Force Behind Falling Inflation

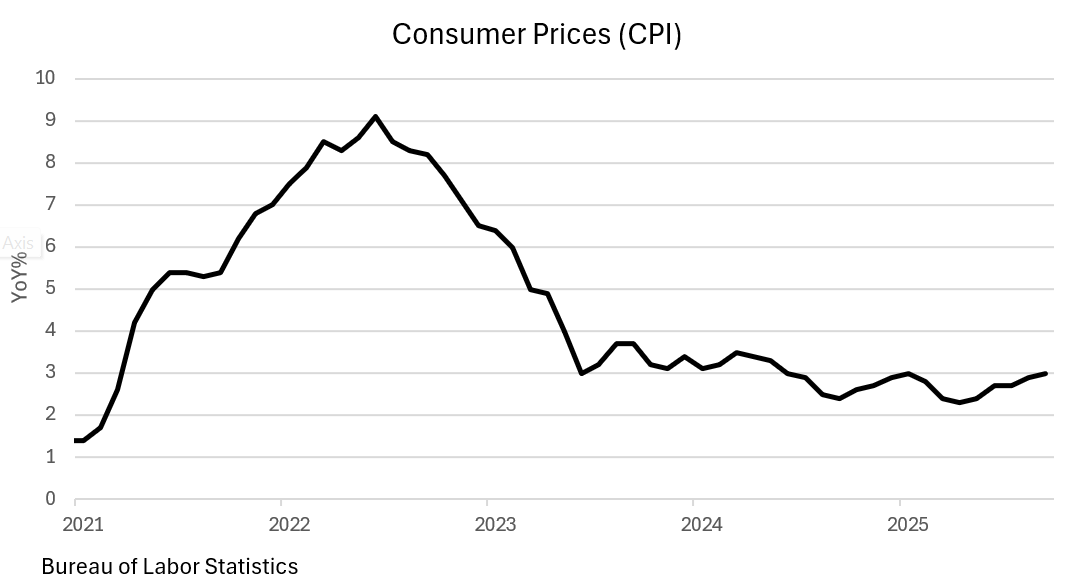

While policymakers debate whether inflation has truly returned to target, a deeper structural transformation is underway.

Artificial intelligence — the most general-purpose technology since electrification — is quietly generating structural disinflation/deflation across the U.S. economy.

This isn’t policy-induced moderation. It’s technology-led equilibrium: inflation declining because supply is expanding faster than demand.

As the International Monetary Fund (IMF) noted in AI’s Promise for the Global Economy (Sept 2024):

“AI is our best chance at relaxing the supply-side constraints that have contributed to slowing growth, new inflationary pressures, and rising costs of capital… AI has the potential to produce a major sustained surge in productivity.”

That supply-side expansion — not a collapse in demand — is pulling down the inflation baseline.

How AI Produces Disinflation

AI suppresses inflation by attacking its core drivers — labor costs, production inefficiencies, and service bottlenecks.

Productivity and Cost Compression

AI substitutes digital processing power for human labor, cutting the economy’s marginal cost of output.

A 2023 McKinsey & Company report, The Economic Potential of Generative AI, estimated that:

“Generative AI could enable labor productivity growth of 0.1 to 0.6 percent annually through 2040, depending on the rate of technology adoption.”

The Federal Reserve Bank of Dallas confirmed this in June 2025, writing that “access to AI increases productivity more for less-experienced workers.”

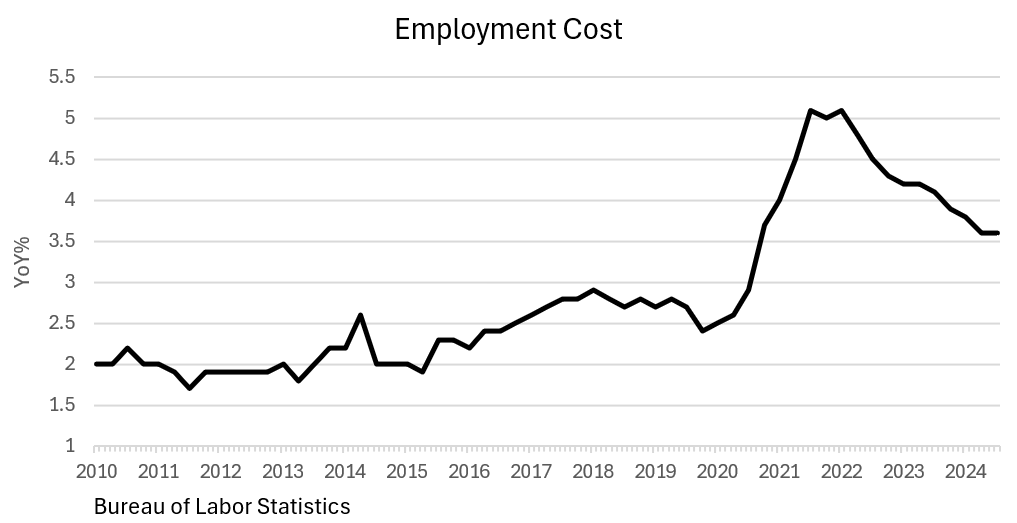

That dynamic reduces unit labor costs, the backbone of services inflation.

Predictive analytics and AI-optimized logistics are simultaneously trimming waste and transport costs by 5–12 percent, creating a deflationary drag across manufacturing and retail sectors.1

In services — where inflation typically sticks — AI is beginning to unwind the rigidity.

According to McKinsey’s State of AI 2025, a majority of firms report material cost reductions in white-collar functions from generative AI deployment.

These efficiency gains together translate into an estimated 0.5 to 0.7 percentage-point annual drag on CPI, enough to re-anchor long-run inflation near 1.8 percent.

Quality, Competition, and “Good Disinflation”

AI also raises product quality and competitive pressure simultaneously.

Better design, fewer defects, longer product lifespans — these are hidden forms of hedonic deflation, where real value rises faster than prices.

And once one company achieves efficiency through AI, the competitive equilibrium forces others to match it, propagating disinflation across the sector.

As EY economist Lydia Boussour told Reuters in late 2023:

“If companies can generate strong productivity growth, they will not be so inclined to pass elevated input costs onto consumers.”

This is “good deflation” — lower prices from efficiency, not contraction.

The Physical Counterweight: Infrastructure and Energy Inflation

The only inflation still visible in the AI economy is physical.

Data centers, power systems, and semiconductor manufacturing are capital-intensive, not consumer-facing, and create localized cost pressures.

Each hyperscale data center consumes 50–100 megawatts of power, about the load of a medium-sized city.

The International Energy Agency (IEA) warned in April 2025:

“Global electricity consumption from data centers is set to more than double by 2030… In the United States, power consumption by data centers is on course to account for almost half of the growth in electricity demand between now and 2030.”

These effects are concentrated in Virginia, Texas, Oregon, and Georgia, where grid congestion has driven wholesale electricity prices up 10–18 percent year-over-year.

Nationally, though, the CPI energy index remains flat.

Tier IV data center build-out costs have surged 35 percent since 2020, and power-distribution equipment by 45 percent, inflating producer prices but leaving consumers largely untouched.

AI’s Next Disinflationary Wave: Job Destruction, Tokenized Labor, and Demographic Reality

The first wave of AI disinflation came from cost efficiency.

The next will come from labor substitution — and it will collide directly with U.S. demographic realities.

Demographic Tailwinds for Disinflation

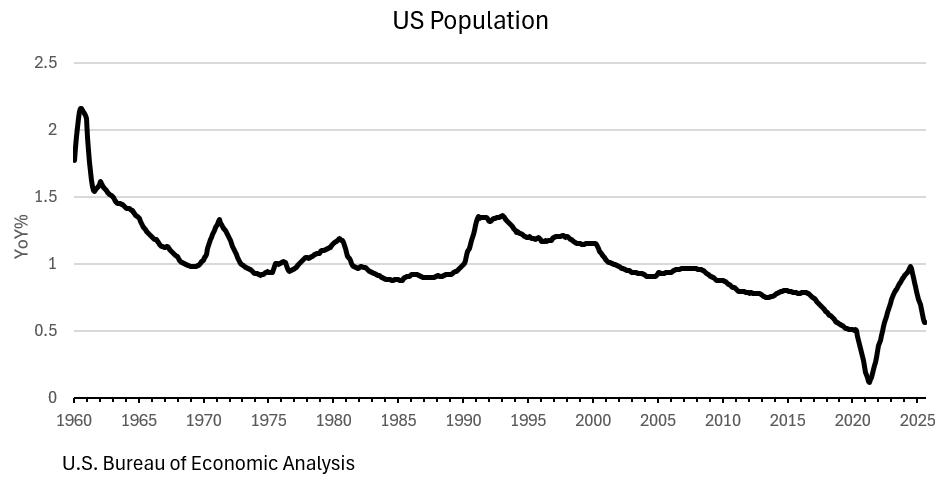

The U.S. labor market is already aging into scarcity.

The median American worker is now 42.3 years old, up from 36 in 2000.

The labor force participation rate among those aged 25–54 — long the backbone of economic growth — has plateaued.

Meanwhile, the dependency ratio (those aged 65+ relative to the working-age population) is projected by the Census Bureau to rise from 27% today to 37% by 2035.

This means fewer new entrants, slower population growth, and more structural wage rigidity — normally inflationary dynamics.

But AI reverses the script.

By automating productivity, AI compensates for labor scarcity and caps wage pressure.

In a sense, the U.S. is entering a “Japanization without stagnation” phase: slow population growth, high technological substitution, and price stability achieved through efficiency, not demand collapse.

In the pre-AI demographic era, slower workforce growth raised inflation risk by constraining supply.

In the AI era, the same demographic slowdown reinforces deflation/disinflation because automation fills the labor gap.

This is the demographic-technological convergence that defines the next decade: an aging workforce that limits demand, and AI substitution that limits costs — a dual anchor on inflation.

From Augmentation to Redundancy

Early AI systems augment human work; agentic systems will replace it.

These self-directed AI “agents” can plan, execute, and settle multi-step workflows autonomously.

When combined with blockchain-based smart contracts, they form tokenized labor markets where work is measurable, tradable, and enforceable without human intermediaries.

McKinsey’s AI and the Future of Work (2025) estimates that:

“Activities accounting for up to 30 percent of hours currently worked across the U.S. economy could be automated by 2030.”

The OECD adds that 27 percent of jobs are “highly exposed” to automation and another 44 percent partially exposed.”

In an aging, slow-growing labor market, this is not just substitution — it’s structural repricing.

When the cost of labor is replaced by the cost of compute, wage growth decouples from output growth, flattening the Phillips Curve.

Tokenization and the Vanishing Transaction Layer

The next phase of disinflation comes from tokenization — where tasks are performed and settled autonomously between AI systems.

Every layer removed from the transaction stack (billing, payroll, HR, compliance) compresses service costs.

If tokenized automation removes even 20 percent of these overheads, it could subtract 0.3–0.4 percentage points from annual core-services inflation.

As AI agents become the marginal producers of digital labor, transactional friction disappears, and with it, much of the inflationary inertia in service economies.

The Paradox of Abundance

The demographic-technology combination yields a strange macroeconomic paradox:

A shrinking labor force normally creates inflation; an expanding digital workforce neutralizes it.

Output keeps rising, but labor income does not.

This is the paradox of abundance: more goods and services produced at lower cost, but with a shrinking wage share of GDP.

The IMF warned in its 2024 technology outlook that:

“Without policy adaptation, AI-driven productivity gains could widen income disparities even as they restrain inflation.”

Disinflation, then, comes not just from efficiency but from labor displacement within an aging population — an economy producing more with fewer workers, and fewer wage earners to drive demand.

Policy, Corporate, and Market Implications

Central banks face an interpretive challenge: distinguishing healthy, technology-driven disinflation from deflationary demand weakness.

If the Fed treats falling inflation as softness rather than supply expansion, it risks over-easing — fueling asset bubbles even as consumer inflation stays subdued.

Fiscal policy will have to adapt through redistribution: tax frameworks for autonomous productivity, wage supplements for displaced workers, and public investment in non-automatable care sectors.

For Corporate America, the new equilibrium is margin expansion with employment contraction.

Companies will enjoy stronger profits per employee, but aggregate wage growth will lag.

That translates into persistent disinflation even as corporate earnings remain robust.

The Structural Endgame

By 2035, AI could account for 60–70 percent of total productivity growth in the U.S. economy, effectively anchoring inflation to the cost of computation.

When the marginal cost of labor gives way to the marginal cost of compute, and compute prices fall with Moore’s Law, the result is permanent technological disinflation.

Inflation will no longer be tethered to wages or employment levels but to energy, bandwidth, and compute cycles — inputs that trend cheaper over time.

In effect, the price level itself becomes a derivative of technological cost, not labor cost.

Conclusion: Disinflation by Design

Artificial intelligence is quietly rewriting the logic of inflation.

By substituting computation for labor, tokenization for bureaucracy, and automation for scarcity, it has created a self-reinforcing disinflationary cycle.

Demographics amplify that cycle — fewer workers, slower demand, more automation, and a lower structural inflation floor.

The U.S. is aging into efficiency, not stagnation.

For policymakers, this is both a gift and a warning:

AI has solved inflation, but it may also hollow out employment.

The challenge of the next decade is not suppressing prices, but sustaining purpose — ensuring that the prosperity of abundance remains broadly shared in a world where productivity no longer depends on people.

AI is delivering deflation/disinflation by design — and redefining what it means to grow.

I'm Joshua, a financial advisor from Reno, Nevada. As someone who co-founded and built a trust company and investment advisory firm from the ground up, I’m passionate about sharing the lessons I've learned on my financial journey of 30+ years to guide and empower clients to secure their financial futures. Using active macroeconomic quantitative and tax avoidance strategies, I mitigate risk and help families achieve lasting financial independence, acting as guardians for future generations. Trust, consistency, and accessibility are at the heart of all my long-lasting client relationships.

Josh Barone is an investment adviser representative with Savvy Advisors, Inc. (“Savvy Advisors”). Savvy Advisors is an SEC registered investment advisor. The views and opinions expressed herein are those of the speakers and authors and do not necessarily reflect the views or positions of Savvy Advisors. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy. All advisory services are offered through Savvy Advisors, Inc. an investment advisor registered with the Securities and Exchange Commission (“SEC”). The views and opinions expressed herein are those of the speakers and authors and do not necessarily reflect the views or positions of Savvy Advisors.

References: