April 2026

Risk Assets Rebounded as Earnings Regained the Spotlight

April showed that markets can recover quickly when earnings momentum and resilient corporate fundamentals help investors look through near-term macro uncertainty.

After March’s oil-driven reset, investors entered April focused on the durability of the expansion, the inflation impact of higher energy prices, and whether corporate earnings could continue to support risk assets. By month end, the market backdrop had improved. Energy prices remained volatile, Treasury yields moved higher, and the Federal Reserve stayed cautious, while first-quarter earnings helped restore confidence in the equity outlook.

That shift showed up clearly across U.S. markets. The S&P 500 rose 10.4% in April, its strongest monthly gain since November 2020. The Nasdaq Composite gained 15.3%, its best monthly performance since April 2020. The Dow also advanced roughly 7%, and the Russell 2000 participated as risk appetite broadened beyond mega-cap technology.

April built on many of the same themes that pressured markets in March, but with a more constructive investor response. The inflation shock remained relevant, geopolitical uncertainty continued, and rate-cut expectations stayed fluid. At the same time, stronger earnings, continued AI investment, and better market breadth helped shift investor attention back toward corporate fundamentals.

Noteworthy Developments

Earnings Took the Lead From Oil

The most important development in April was the market’s shift in focus from the oil shock to earnings.

Energy remained a key macro variable. Brent crude stayed above $100 per barrel and briefly traded as high as $126, its highest level since March 2022, before settling lower late in the month as investors reacted to renewed U.S.-Iran diplomatic headlines. Still, equities showed a greater ability to absorb energy volatility as earnings season progressed.

First-quarter earnings season helped improve the tone. S&P 500 earnings expectations moved materially higher as large technology companies reported results, with projected first-quarter profit growth reaching its fastest pace since late 2021. That was an important change from earlier in the month, when investors were still evaluating whether higher energy prices, tariff uncertainty, and elevated interest rates would pressure margins.

The AI theme remained the center of gravity. Semiconductors led the move, with the PHLX Semiconductor Index rising sharply in April. Communication Services and Information Technology were the strongest S&P 500 sectors, supported by enthusiasm around cloud infrastructure, data-center spending, AI hardware, and software monetization.

The month’s takeaway is that strong earnings can help investors look through periods of macro uncertainty, particularly when profit growth is broad enough to reinforce confidence in the cycle. Macro risks remain important, but April showed that corporate fundamentals can still carry the market when results are strong.

U.S. Equities

A Sharp Rally Led by AI, Earnings, and Better Risk Appetite

U.S. equities rebounded sharply in April, reversing March’s weakness and pushing major indexes back toward prior highs.

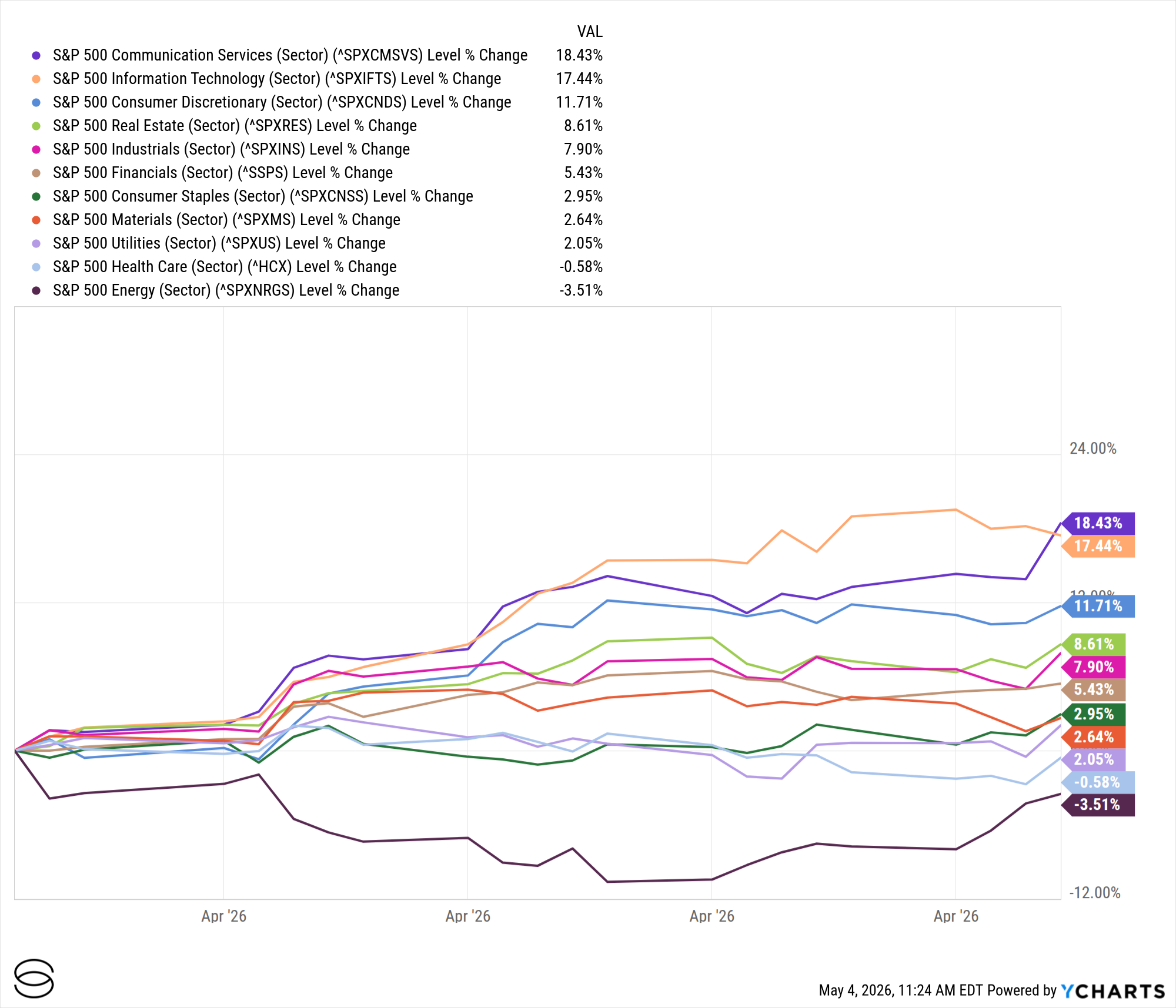

The S&P 500’s 10.4% monthly gain was broad on the surface, with 9 of the 11 sectors finishing higher. Leadership, however, remained strongest in areas tied to AI, cloud infrastructure, semiconductors, and large-cap technology. Communication Services led, helped by Alphabet, while Information Technology followed closely as chipmakers surged.

The rally was growth-led, with investors rewarding companies connected to AI capex, power demand, cloud growth, and data-center buildout. Demand for power-generation equipment, semiconductor capacity, and AI infrastructure continued to support the view that this remains a multi-year investment cycle.

Small caps also participated, which was encouraging from a breadth perspective. The Russell 2000 gained ground in April as risk appetite improved and investors looked beyond the largest index constituents. That said, the backdrop for small caps remains closely tied to rates, financing conditions, and earnings delivery. With Treasury yields still elevated and the Fed reluctant to ease, smaller companies may need more stable macro conditions to sustain stronger relative performance.

From a portfolio perspective, April was a constructive month for equity exposure. Market leadership still favored quality growth and AI-linked companies, but improving participation across sectors and market-cap segments was an encouraging sign.

Exhibit 1: U.S. Equity Performance

Exhibit 2: U.S. Sector Performance

International Markets

Global Equities Recovered, With EM Tech in Focus

International markets also recovered in April, though regional performance remained tied to different drivers.

European equities rebounded after March’s sharp drawdown. The STOXX 600 gained roughly 4.8% in April, its best monthly showing since January 2025. The recovery reflected the broader improvement in global risk appetite, although Europe remains more exposed to the energy-price channel than the U.S., particularly through industrial input costs, transportation, and consumer energy expenses.

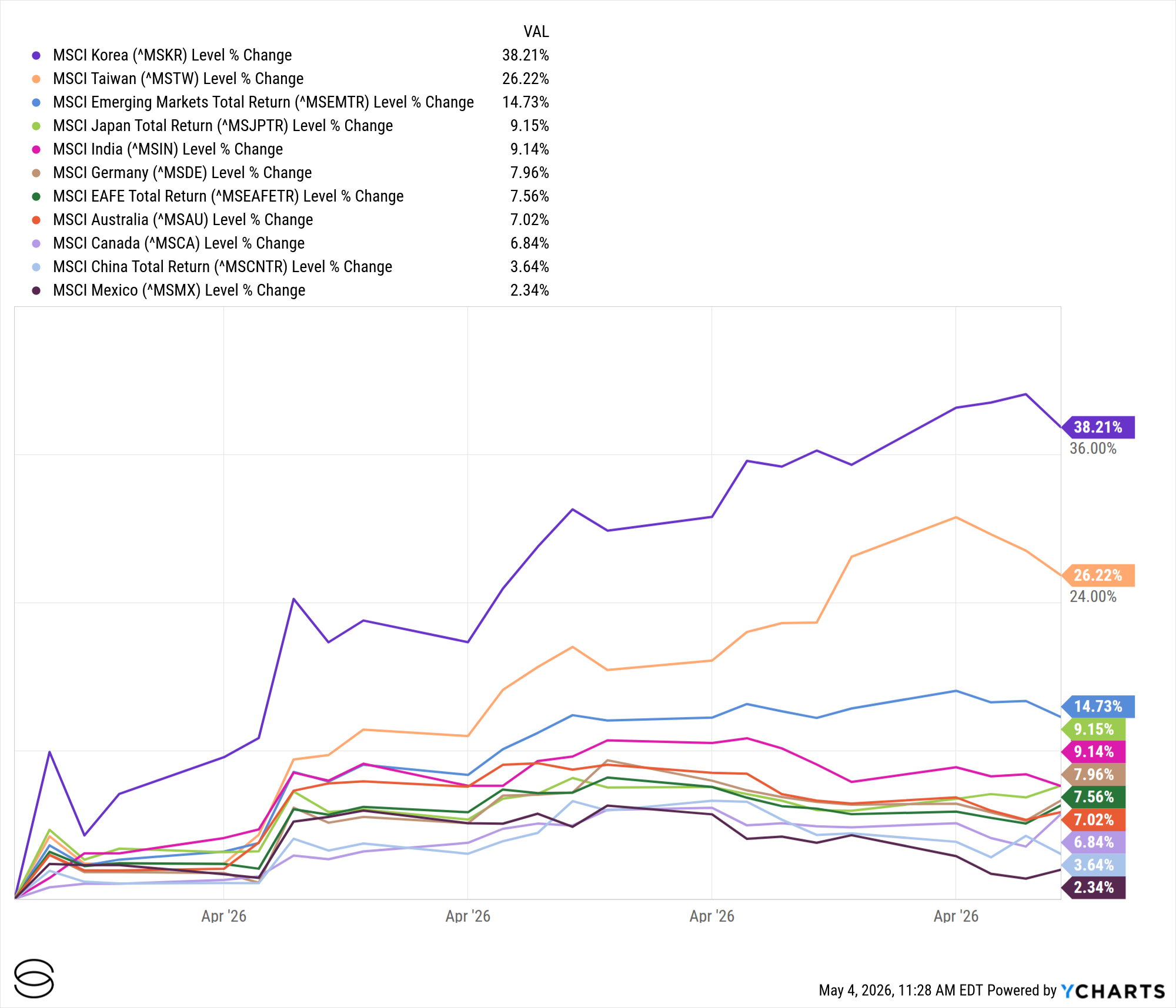

Emerging markets were helped by a renewed focus on the AI hardware cycle. Taiwan and South Korea remained central to the story, given their importance in semiconductors, memory, and the broader global technology supply chain. South Korea’s April exports rose strongly, supported by robust semiconductor demand, reinforcing the connection between EM performance and AI infrastructure spending.

The MSCI Emerging Markets Index reached a record high during April, propelled by strength in Korea and Taiwan. That is constructive for EM investors, while also making the composition of returns important. A meaningful share of recent EM strength has come from AI-linked hardware companies, which means the index is increasingly sensitive to global capex expectations and semiconductor demand.

Exhibit 3: International Market Performance

Fixed Income and Commodities

Yields Stayed Elevated While Oil Remained the Key Macro Watchpoint

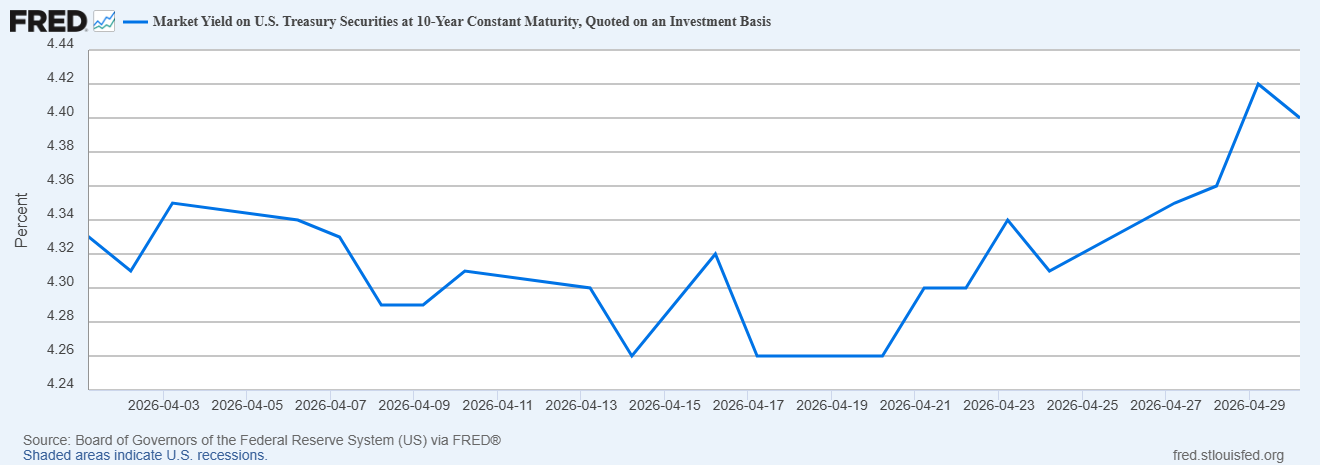

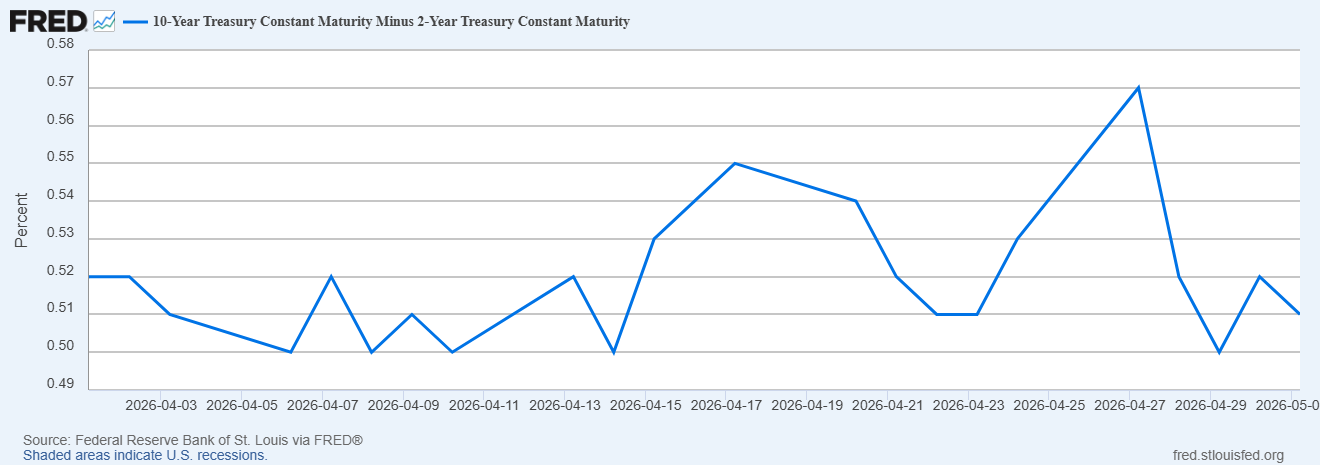

Fixed income had a more challenging month than equities. Treasury yields moved higher as investors weighed the inflation impact of elevated energy prices and a more cautious Fed. The 10-year Treasury yield ended the month near 4.4%, up roughly 8 basis points, while the 2-year yield finished near 3.9%.

The setup for bonds remains mixed. Higher yields provide more income than they did during the prior cycle, improving the long-term return profile for fixed income. Duration, however, remains more vulnerable when inflation risk is the market’s primary concern, which may keep bond performance uneven until energy prices and inflation expectations stabilize.

Oil remained the key commodity to watch. Brent stayed above $100 per barrel, briefly moved above $126, and then retreated late in the month as diplomatic headlines reduced some of the immediate risk premium. Gold was less of a factor. After drawing investor attention earlier in the year, gold finished the month modestly lower and offered limited protection during the March risk-off move. Recent cross-asset behavior reinforced that oil was the more important macro variable in April because of its direct link to inflation, consumer expectations, transportation costs, and central bank policy.

Exhibit 4: Cross-Asset Performance

Exhibit 5: U.S. 10-Year Treasury Yield

Exhibit 6: U.S. 10-Year Minus 2-Year Treasury Yield Spread

Economy and Policy

Growth Held Up as the Fed Stayed Patient

The April data showed an economy that continued to expand, with inflation still the key constraint on policy flexibility.

First-quarter real GDP rose at a 2.0% annualized rate, rebounding from 0.5% growth in the fourth quarter of 2025. The increase was supported by investment, exports, consumer spending, and government spending, while consumer spending moderated. Real final sales to private domestic purchasers, a useful measure of underlying private demand, rose 2.5%.

Inflation remained the more difficult part of the backdrop. March CPI rose 0.9% month over month and 3.3% year over year, with energy prices driving a large share of the move. Core CPI was more contained, rising 0.2% on the month and 2.6% year over year, suggesting that the inflation shock was still most visible in the headline data.

The March PCE report told a similar story. The PCE price index rose 0.7% month over month and 3.5% year over year. Core PCE rose 0.3% month over month and 3.2% year over year. That keeps inflation above the Fed’s 2% target and helps explain why policymakers remained cautious.

The Fed held rates steady at its April 28 to 29 meeting. Chair Powell emphasized that the current stance of policy remains appropriate and acknowledged that developments in the Middle East have contributed to a high level of uncertainty. The market’s takeaway was that the bar for rate cuts has moved higher. With energy prices still elevated and inflation above target, investors increasingly expect the Fed to remain on hold through 2026 unless inflation pressures ease more convincingly or labor-market conditions weaken.

Key Dates to Watch in May 2026

Markets will be watching whether April’s equity rally can be validated by incoming labor, inflation, and spending data.

May 1: April Employment Report

May 5: ISM Services and JOLTS Job Openings

May 13: April CPI

May 14: April PPI

May 15: April Retail Sales

May 20: FOMC Minutes from the April 28 to 29 meeting

May 29: April Personal Income and Outlays, including PCE inflation

The Bottom Line

April delivered a meaningful rebound across risk assets, led by stronger earnings, renewed momentum in AI-related sectors, and improved investor risk appetite. U.S. equities recovered much of March’s weakness, international markets participated in the rally, and small caps showed better breadth as the month progressed.

The macro backdrop remained more complicated. Energy prices stayed elevated, Treasury yields moved higher, and inflation data kept the Fed focused on maintaining a patient policy stance. Market expectations also shifted further toward a higher-for-longer rate environment, with the timing of any future rate cuts increasingly dependent on incoming inflation, labor-market, and energy-price data.

The next phase for markets will likely depend on whether earnings momentum continues, whether inflation pressures stabilize, and whether the rally broadens beyond the areas most closely tied to AI and large-cap technology.

Anshul Sharma is Chief Investment Officer at Savvy Wealth, where he oversees the firm’s investment strategy, portfolio design, and platform innovation. He partners across product, marketing, and operations teams to deliver portfolios that take a methodological approach to balance customization with scalability for advisors and their clients. Before joining Savvy, Anshul spent nearly two decades at Bank of America, where he managed the Chief Investment Office’s Sustainable Model Portfolio Suite, launched new proprietary offerings, and, as Head of Alternative Investment Strategy, provided guidance and thought leadership to advisors around hedge fund, private market, and real asset strategies. He began his career as an Investment Strategist at U.S. Trust, designing multi-asset portfolios for high-net-worth and institutional clients. Anshul holds a Master of Financial Engineering from UC Berkeley and a Bachelor of Computer Engineering from Lehigh University. Outside of work, he is an avid tennis player, enjoys time with his wife, two sons, and their Bernedoodle, and is an auto enthusiast who loves cooking and travel.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation from the Savvy Investment Team. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Investment Management ("SWIM") is a proprietary, in-house investment solution offered by Savvy Advisors, Inc. (“Savvy Advisors”). It is designed to support financial advisors in the management of client portfolios. Savvy Wealth Investment Management is not a separate legal entity and is not independently registered as an investment adviser. All advisory services are provided by Savvy Advisors in its capacity as a registered investment adviser.