How to Build a Financial Plan in Your 40s: A Guide to Financial Security and Prosperity

Your 40s are a turning point, and that’s precisely why financial planning tips for midlife are so vital. As such, your income might be near its peak, but retirement is also finally starting to become a reality. At this stage, you’re balancing long-term goals with immediate needs. You're juggling financial responsibilities like mortgages, college savings, and investment growth.

Recent studies show that individuals who work with financial advisors in their 40s tend to save more. They're also more confident in their financial future. This decade is the ideal time to put strategy behind every dollar as you prepare for the decades ahead, while still enjoying today.

Key Takeaways

- Your 40s are a pivotal time to review your complete financial picture.

- Aim to save at least three times your annual salary by 40, and increase retirement contributions as income grows.

- Maintain an emergency fund to protect against unexpected expenses while continuing long-term investments.

- Diversify your portfolio with a balanced mix of growth and value investments.

- Professional guidance, especially from a CFP, can refine your plan and reduce uncertainty.

Retirement Planning Strategies for Your 40s

Retirement planning in your 40s means fine-tuning, not starting from scratch. By now, you’ve likely built some savings and established healthy habits. However, this decade presents an opportunity for you to make further progress and close any gaps before retirement. It’s also when decisions about contributions, investments, and timing make a lasting impact.

Setting Retirement Savings Goals

Experts often recommend having around three times your annual salary saved by the time you reach age 40. While that’s a good benchmark, many people fall short, as the median retirement savings for individuals aged 35-44 is $45,000. For those aged 45-54, the figure is $115,000, highlighting that a sizable portion of people are still catching up.

A well-rounded retirement plan covers five areas:

- Cash Bucket: Your emergency fund and short-term cash flow.

- Income Bucket: Social Security or other guaranteed income sources.

- Investment Bucket: Stocks, bonds, and other long-term growth assets.

- Risk Management: Insurance coverage that protects your income.

- Legacy Planning: Wills, trusts, and beneficiary designations.

Maximizing Retirement Contributions

Your 40s are the ideal time to take full advantage of retirement accounts. For 2026, you can contribute up to $24,500 to a 401(k), plus an employer match if available. An IRA allows $7,500 in contributions, with an additional $1,000 catch-up contribution available once you turn 50.

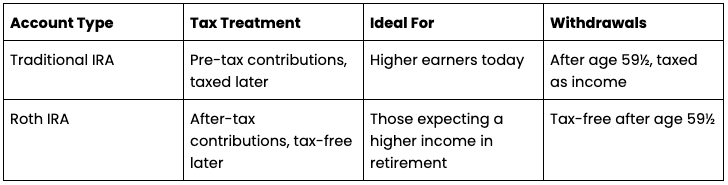

Here’s a comparison of Traditional vs. Roth IRAs:

If you earn too much to contribute to a Roth IRA, a backdoor Roth conversion is an option. Combining employer matching, tax advantages, and consistent contributions makes a significant impact over time.

Withdrawal Strategies

Planning how you’ll draw income later can be as critical as how you save now. Research shows that a proportional withdrawal strategy (i.e., drawing from taxable, tax-deferred, and tax-free accounts in balance) reduces taxes and extends your savings.

The goal is to manage withdrawals so that your tax bracket remains stable year to year, while still providing a reliable income stream throughout retirement.

Social Security Planning

Social Security can replace about 40% of your pre-retirement income, so your claiming strategy matters. Your full retirement age is between 67, but holding off on benefits until age 70 significantly increases monthly payments.

However, many people don’t wait. In fact, only about 10% of Americans claim Social Security at the optimal time, often leaving substantial lifetime income unclaimed. Taking the time to model your claiming options, or discussing them with a planner, lets you avoid leaving money on the table.

Utilizing Retirement Planning Software

Digital tools make retirement modeling more accessible and accurate. Platforms like Boldin and WealthTrace offer features such as scenario testing and tax analysis. For simple calculations, AARP and Bankrate provide free, easy-to-use calculators.

Modern financial planning software enables you to adjust variables such as savings rate, investment return, or retirement age to see how each factor affects your long-term outlook. Using these tools regularly ensures you stay on track and make informed adjustments as life changes.

Debt Management and Savings Strategies for Your 40s

Managing debt while growing savings is one of the most common financial challenges in your 40s. This stage of life often comes with significant expenses, such as mortgages, family costs, or college savings, so finding a balance between paying down debt and saving for the future is crucial. Building healthy habits now makes the next decade a lot less stressful.

Building an Emergency Fund

An emergency fund acts as your line of defense when unexpected expenses arise. Financial planners usually suggest saving three to six months’ worth of living expenses. However, aiming for the higher end of that range adds more stability in your 40s.

Keep these funds in a high-yield savings account where they stay liquid and earn interest. Many online banks offer competitive rates that grow your savings without tying up your money. Treat this account as off-limits unless an emergency pops up. It’s there to protect your long-term plans, not to fund convenience spending.

Debt Consolidation Options

If you’re juggling multiple loans or credit cards, debt consolidation makes repayment simpler and potentially lowers your interest rate. Not all debts are equal, as using a home equity line of credit with a significantly lower interest can get the debt paid off quicker and accelerate your financial goals.Each option has pros and cons. Personal loans reduce your interest rate but require good credit. Balance transfers may offer 0% interest for a short period, but fees might apply. Debt management plans bundle payments and may negotiate lower rates with lenders, though some agencies charge small monthly fees.

Prioritizing Debt Repayment vs. Saving

Deciding whether to pay off debt or save more is a tug-of-war. The general rule:

- Don’t pass up free money! Capture your 401(k) match first, especially generous programs that match your contribution dollar for dollar.

- Tackle high-interest debt next, such as credit cards.

- Make minimum payments on low-interest debts, like student loans or mortgages, while continuing to save. It may ‘feel’ good to accelerate these larger balances, but stay focused on the high-interest debt.

Balancing both priorities lets you generate wealth without losing momentum. The key is steady progress, like reducing debt while allowing your investments to grow in the background.

Relationship Between Financial Assets and Mental Health

Money affects your bank account, but it also influences your peace of mind. Research shows that individuals with financial security tend to experience lower stress and improved emotional health.

A 2020-2023 longitudinal study found that individuals with less than $5,000 in financial assets had over twice the odds of screening positive for depression and anxiety compared to those with $100,000 or more in assets.

This highlights that saving doesn’t solely concern retirement; it can also influence your stability and well-being. Having cash reserves and long-term investments provides reassurance during uncertain times and gives you greater control over your financial choices.

Investment Strategy and Asset Allocation for Your 40s

Your 40s are the time to fine-tune your investment mix. You’ve likely built a portfolio by now, but your goals, income, and risk tolerance might have changed. A good approach to building an investment portfolio in your 40s focuses on diversification, growth, and tax awareness. During this decade, you’ll want to stay invested while gradually reducing any unnecessary risk.

Determining Stock Allocation

If you’re in your 40s, a generic "middle-of-the-road" portfolio is a missed opportunity. You are in your prime earning years with at least two decades of work ahead of you, continue to focus on the long-term. While "safe" investments feel good during a market dip, playing it too safe now is the biggest risk to your future lifestyle. You need a portfolio that actually has the horsepower to outpace inflation and compound significantly before you even think about hitting the "slow" button.

Think of your Roth account as a high-security vault where the IRS has no key. If you’re aiming for an 80/20 split between stocks and bonds, don't just sprinkle a little of each into every account. Instead, treat your Roth as your "100% Equity Zone." By putting your highest-growth investments there, you ensure that your biggest winners are the ones you eventually withdraw 100% tax-free. You can always balance out the slow and steady 20% of your portfolio (the bonds) in your taxable or traditional accounts. It’s not just about what you own; it’s about making sure your best players are playing on the tax-free field.

Growth vs. Value Investing

Investors often choose between growth stocks, which focus on companies expanding quickly, and value stocks, which trade below their estimated worth. Both have a place in a long-term plan.

Value stocks have actually outperformed growth stocks over rolling 15-year periods in 93% of cases since 1927. That doesn’t mean value always wins, but blending both styles works out best for returns over time.

Using mutual funds or ETFs (Exchange-Traded Fund) that track both types of companies keeps your portfolio balanced without the need to pick individual stocks.

Tax-Efficient Investing

Your 40s are also the time to start thinking about tax-efficient investing. Placing certain investments in specific account types makes a sizable impact on what you keep after taxes.

Here’s a quick breakdown:

- Tax-Deferred Accounts: Best for tax-inefficient assets such as bonds or REITs (Real Estate Investment Trust).

- Taxable Accounts: Better for index funds or ETFs with low turnover.

- Tax-Free Accounts: Great for long-term growth assets because withdrawals are tax-free.

- Health Savings Accounts (HSAs): Triple tax benefits, and contributions, growth, and qualified withdrawals are all tax-free.

Some investors in their 40s also explore Roth conversions to reduce future tax burdens, especially if they expect to be in a higher tax bracket in retirement. If your household income varies year to year, consider taking advantage of that ‘tax valley’, while switching to tax avoidance in years of a ‘tax peak’. In retirement, Medicare premiums are income based, so conversions today can mitigate those surcharges.

Finding the Best Financial Guidance in Your 40s

Even if you’ve managed your money independently until now, your 40s are an ideal time to seek professional guidance. With higher earnings, family responsibilities, and long-term goals in play, expert insight lets you refine your plan and stay on track. When it comes to financial planning tips for midlife, choosing the proper kind of support heavily influences how you reach your goals.

Financial Advisors vs. Financial Coaches

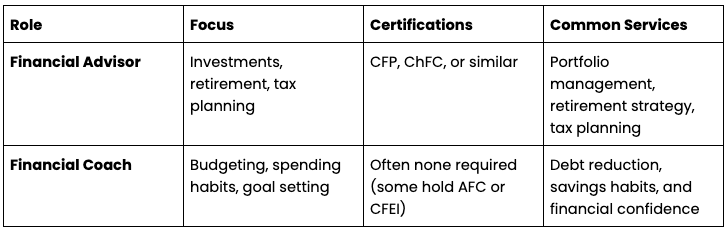

Not all financial professionals serve the same role. Financial advisors and financial coaches both offer valuable guidance, but in very different ways.

Advisors generally manage investments and provide long-term planning under a fiduciary duty, meaning they’re required to act in your best interest. Coaches, on the other hand, focus more on short-term behaviors and building healthy money habits.

A financial advisor may plan your estate or optimize investments, while a coach might create a budget that works for your current lifestyle. Both are valuable depending on where you are in your financial journey.

Utilizing Professional Guidance

Many people in their 40s use a mix of resources to make financial decisions, and advisors, online tools, and family advice all have their place. Gallup data shows that preferences for professional guidance often increase with income, but accessibility remains key for everyone, regardless of net worth.

People at this stage often want reassurance that they’re doing it correctly, whether that means staying on track with retirement or managing investments properly. Working with a trusted expert brings clarity, ensuring you make confident choices for your goals and lifestyles.

Benefits of CFP Professionals

CFPs bring an extra layer of training and accountability to the planning process. They’re fiduciaries at all times, meaning they put your best interests first, and they’re trained in retirement, tax, estate, and insurance planning.

A CFP Board study found that 49% of Americans advised by CFP professionals reported that their advisor helped alleviate their financial anxiety, compared to only 31% of those working with non-certified planners.

Beyond investment advice, CFPs manage significant life transitions, like updating your estate plan or navigating healthcare costs. If you haven’t already set up legal documents such as a will or healthcare directive, see our related guide on living will planning.

Fee Structures and Choosing a Professional

Financial professionals can charge in a few different ways:

- Percentage of Assets Under Management (AUM): Commonly 0.5%-1% annually.

- Flat-Fee or Hourly: Best for those who want one-time planning or advice on specific goals.

- Commission-Based: Less common among fiduciaries; may create potential conflicts of interest.

Before hiring someone, ask these three key questions:

- Are you an employee or independent advisor?

- How are you paid?

- Are you a fiduciary some of the time, or at all times?

Knowing both answers upfront ensures you understand their incentives and your working relationship.

Hybrid Approaches

Many midlife investors are turning to hybrid models that blend digital tools with personal advice. You can use planning software for everyday management while paying a fee-only planner for major milestones, like selling a home, changing jobs, or preparing for retirement.

This “best of both worlds” approach offers professional insight when you need it most, without committing to a full-service fee year-round. For many in their 40s, that balance provides structure without overcomplication.

Integrating Components Into a Comprehensive 40s Financial Plan

A good financial plan in your 40s ties everything together, such as your savings, investments, debt, and long-term goals. This decade offers a valuable mix of income potential and time, providing you with the space to strengthen your financial foundation and prepare for the years ahead.

Next Steps:

- Review your retirement accounts and confirm you’re meeting or exceeding annual contribution limits.

- Reassess your debt repayment strategy to ensure it aligns with your savings goals.

- Evaluate your investment portfolio for diversification and tax efficiency.

- Schedule a consultation with a CFP to build or update your long-term plan.

- Revisit your will, insurance coverage, and beneficiary information every few years.

FAQs

What is the 50/30/20 rule for savings?

The 50/30/20 rule divides your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings or debt repayment. It’s a flexible budgeting framework that helps you maintain balance while still prioritizing long-term financial goals.

What is a good net worth by age 40?

A common benchmark is to have a net worth roughly twice your annual salary by the time you reach age 40. However, this varies based on lifestyle, career stage, and cost of living. The key is maintaining consistent savings and minimizing high-interest debt as your income grows.

What is the FIRE movement?

FIRE (Financial Independence, Retire Early) is a lifestyle strategy that focuses on saving aggressively—often 50% or more of one's income—and investing those savings to achieve financial independence decades ahead of traditional retirement. The goal isn’t always to stop working, but to gain freedom over how and when you work.

How do I protect my 401(k) from a stock market crash?

Diversification is your best defense. Spread investments across asset classes like stocks, bonds, and cash equivalents, and consider adjusting risk exposure as you near retirement. Rebalancing periodically and maintaining a long-term view help cushion short-term market swings.

What is the rule of 72?

The Rule of 72 is a straightforward formula for estimating how long it will take an investment to double in value. Divide 72 by your expected annual return rate. For example, at a 8% return, your money doubles in about 9 years (72 ÷ 8 = 9).

I’m Ed, a financial advisor based in Westfield, Indiana. I began my career in financial services in 2012 after spending ten years in corporate accounting and finance. Today, I focus on helping the working affluent navigate all areas of financial planning, from investment management and benefits consulting to risk management and long-term strategies. I hold degrees in Accounting and Business Administration from Monmouth College, and I’m proud to be a CPA as well as a CERTIFIED FINANCIAL PLANNER® and Chartered Financial Consultant® (ChFC®). I also stay active in the profession by serving as Co-Director of NexGen for the Financial Planning Association’s Great Indiana Chapter, mentoring newer advisors.

Works Cited

- What Is the Average Retirement Savings by Age?

- How Much Lifetime Social Security Benefits Are Americans Leaving On The Table?

- Financial assets and mental health over time

- Value investing vs. growth investing: Which is better in today’s market?

- Financial Planning Longitudinal Study