Securing Your Legacy: An Essential Planning Guide for New and Expecting Parents

Estate planning for young families often seems distant until a baby is on the way, and suddenly, every decision you make carries more weight. New and expecting parents face a long list of financial choices, from short-term costs to long-term planning that protects their child’s future. Below, we’ll walk you through the core areas to look at during this transition. You’ll learn how to adjust your budget, update key protections, set up the proper legal documents, and establish long-term savings habits that grow with your family.

Get Started with Financial Planning

Key Takeaways

- Financial planning shifts quickly once you prepare for a baby, so review your cash flow and new expenses early.

- Insurance updates, including life, disability, and health coverage, shape your family’s long-term stability.

- Estate planning documents (i.e., wills, guardianship choices, trusts, and powers of attorney) keep decisions clear.

- Long-term savings tools, like 529 plans, ESAs, and custodial accounts, support the accumulation of generational wealth.

- Tax credits, updated retirement contributions, and new account strategies ensure you stay on track as your family grows.

Immediate Impact: Restructuring Cash Flow and Budgeting for Growth

Financial planning for a baby typically begins with a thorough review of your monthly cash flow. New parents often face rising expenses and changes in income. Below, we’ll explain the most common financial shifts and how to adjust your budget in a clear, steady way.

The Financial Reality Check: Documented Strain and New Expenses

Understanding how to financially prepare for a baby begins with recognizing the common challenges that new parents often face. The costs of raising a child begin immediately and continue through housing, childcare, healthcare, and everyday needs. Recent reports indicate that millennial-age parents face significant financial strain, with 41% rating their financial health as unsatisfactory and 40% noting that money pressures negatively impact their relationships. Debt also climbs quickly, with new parents taking on an average of $181 in new debt each month.

If you’re deciding how to start saving money for a baby, begin by listing new monthly costs and separating them into immediate, near-term, and long-term categories. This makes room for steady adjustments without being pulled in too many directions at once.

Navigating Parental Leave and Income Adjustments

Parental leave can have a significant impact on household income, particularly for mothers. Research shows that mothers face a 38% earnings gap compared to fathers during the year of birth, primarily due to reduced work hours. That gap widens to 43% by eleven years after childbirth, often because mothers move to lower-paying firms.

Planning ensures you understand what your income may look like during this period. Look at short-term disability benefits, any paid leave your employer offers, and your current savings. Then, create a temporary version of your budget based on the income you expect during leave.

Create a High-Earning Family Budget for Sustainability

A robust family budget gives you a clear path when you’re learning how to save money with a new baby. Begin by incorporating baby-related expenses into your existing budget. Include medical bills, diapers, clothing, supplies, and childcare. It’s also beneficial to explore flexible options, such as second-hand gear, shared items from friends or family, and meal planning, to minimize unexpected grocery expenses.

Childcare sits near the top of many parents’ budgets. Reports show that childcare accounts for about one-quarter of a household’s monthly budget, and many families also spend a significant share of their income on housing, sometimes as high as 74%. If daycare costs create pressure, look at part-time schedules, employer programs, or mixed care arrangements that balance time and expense.

Protecting Your Family: Essential Insurance and Risk Management

Insurance plays a crucial role in maintaining the stability of your household during major life changes. Below, we’ll walk you through the core policies new and expecting parents review first, along with the updates that typically follow once a baby arrives.

Core Protections: Life and Disability Insurance

Life insurance often becomes a priority once you begin planning for your child’s future. Many parents compare term and whole life insurance during this stage. Term insurance typically offers higher coverage for a lower cost, while whole life includes a savings component that continues throughout your lifetime. The best choice depends on your income, long-term goals, and the level of security you desire.

Disability insurance is also vital, particularly for high earners. Your income keeps your household running, so protecting it can steady your finances if an illness or injury reduces your ability to work. Review your employer plan and any supplemental options to see how much income they replace.

Health Coverage, Liability, and Policy Updates

Once your baby arrives, update your health insurance as soon as possible. Most plans require you to add a newborn within a short enrollment window, so take care of it early. Also, review your deductibles, out-of-pocket limits, and whether your pediatrician is in-network.

This is also a good time to look at your homeowner’s or renter’s policy. Ensure your coverage amount still aligns with your household and belongings. Some parents also add an umbrella policy to increase liability protection. These updates keep your coverage current as your family grows.

Securing the Future: Estate Planning for Young Families

Estate planning becomes more immediate once you have children, even if you’re early in your career. Below, we’ll cover the core legal steps that new parents take to protect their child’s future and maintain clear decision-making during significant life events.

The Legal Cornerstones: Guardianship and Wills

A will becomes one of the most essential documents once a child comes into your life. It outlines how your assets are transferred to your child and provides clear guidance during a difficult time. It also includes a guardianship clause, which explains how to appoint a guardian for your children if you pass away while they are still minors.

When considering how to appoint a guardian for your children, start by selecting someone who can provide both daily care and long-term guidance. Then, discuss your expectations with them to ensure they are willing and prepared to proceed. A simple plan gives your family clarity and removes uncertainty later on.

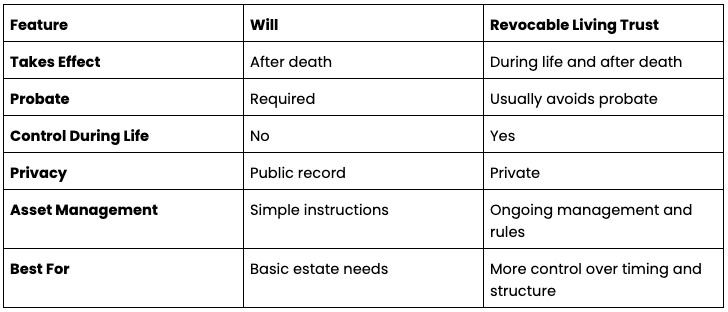

Advanced Wealth Transfer: Utilizing Trusts

Trusts provide parents with greater control over how and when assets are transferred to their children. This makes them a valuable tool in estate planning for young families. A revocable living trust, for example, allows you to manage your assets during your lifetime while creating a clear path for their transfer upon your death.

Trusts also support succession planning for family wealth by letting you set rules for spending, age-based access, or long-term management. When you look at estate planning for children, trusts give you options that a simple will might not provide. They can hold investments, real estate, or life insurance proceeds and guide how those resources support your child over time.

Here’s how they compare:

Finalizing Your Plan: Powers of Attorney and Professional Review

Powers of attorney cover financial decisions and healthcare choices if you become unable to make them. A durable power of attorney names someone to handle money matters, while healthcare directives outline your medical preferences. After preparing these documents, meet with an estate planning attorney to check that everything fits your goals and follows your state’s rules.

Building Generational Wealth: Long-Term Savings and Investments

Long-term planning becomes easier when you understand the savings tools available to your family. Below, we’ll explain education accounts, investment options for minors, and the role early contributions play in building steady growth over time.

Education Funding Strategies

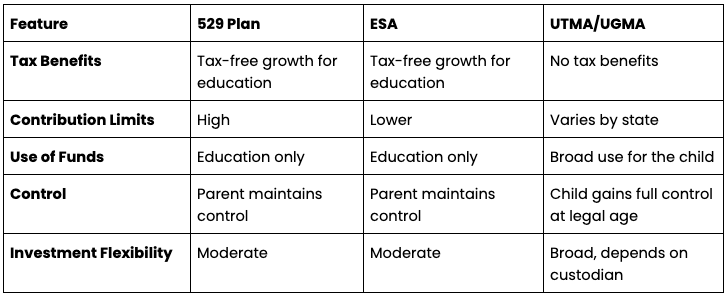

Many parents begin long-term planning by considering how to save for their child’s college education. Tax-advantaged accounts, such as a 529 plan or Education Savings Account (ESA), allow you to save money in a structured manner. When you open a 529 college savings plan, your contributions grow tax-free when used for qualified education expenses. ESAs also offer tax advantages but have lower contribution limits.

The most significant advantage comes from starting early. Even small, steady contributions can grow over time through compounding. This approach gives your child more options later on and keeps higher education within reach.

Here’s how they all compare:

Investment Vehicles for Minors

Custodial accounts, such as UTMA (Uniform Transfers to Minors Act) or UGMA (Uniform Gifts to Minors Act), provide parents with a straightforward way to invest for a child’s future. These accounts hold assets in the child’s name. However, you can manage the money until your child reaches the legal age in your state. They work well for long-term goals that extend beyond education, such as purchasing a first car, securing housing, or gaining early investing experience.

Compared to trusts, custodial accounts are easier to open and manage but offer less control over how the child uses the funds once they become an adult. For long investing timelines, stick to diversified, growth-focused investments that take advantage of compounding over many years.

Protecting Your Own Future: Tax and Retirement Adjustments

Your financial picture shifts once you have a child, and tax and retirement planning often changes along with it. Below, we’ll cover the credits, deductions, and account updates to review as you settle into your new family structure.

New Tax Opportunities: Credits and Deductions

Raising a child opens the door to several tax benefits, even for higher-earning parents. The Child Tax Credit and the Child and Dependent Care Credit can reduce your overall tax bill, depending on your income and childcare expenses. If you recently married, your filing status may also change how much tax you owe when filing jointly or separately.

You can also use tax-advantaged accounts, such as a Flexible Spending Account (FSA) or Health Savings Account (HSA), to cover dependent care and medical expenses. These accounts let you use pre-tax dollars for everyday family expenses throughout the year.

Re-evaluating Retirement Contributions

Your retirement strategy might shift once your household grows. Start by reviewing your current 401(k) contributions and the match your employer offers. You might adjust your contribution amount for a period while still keeping enough to earn the match.

If one parent steps away from work or reduces hours, a Spousal IRA gives you a way to contribute to building retirement savings for the non-working spouse. This keeps long-term planning on track. Also, review the beneficiaries on your 401(k), IRA, and other accounts to ensure that they reflect your new family structure.

The Next Steps in Securing Your Family’s Legacy

Preparing for a new child brings many financial changes. However, taking small steps now strengthens your family’s future. With the proper documents, steady planning, and clear protection in place, you create a foundation that grows with your household. Use the takeaways and next steps below to continue building a long-term plan that supports your goals.

Next Steps:

- Review your current budget and adjust it to include new and upcoming baby-related expenses.

- Update or purchase life, disability, and health insurance before your baby’s arrival.

- Open long-term savings accounts, such as a 529 plan or custodial account, to start building early growth.

- Review your retirement accounts and update beneficiaries to reflect your new family structure.

Personalized Financial Planning

Connect with a Savvy advisor to build a plan that supports your goals today and protects your legacy for years to come.

FAQs

What is the downside of having a trust?

Trusts offer control, but they can be more expensive and time-consuming than a basic will. You must set them up with an attorney, keep the paperwork up to date, and transfer assets into the trust. If you don’t fund it correctly, the trust won’t work as intended.

How much can my kids inherit without paying taxes?

Most families never owe federal estate tax. In 2025, the exemption is $13.99 million per person, allowing children to inherit up to that amount before the federal estate tax applies. State estate or inheritance taxes may apply at much lower limits, and kids may owe income tax on inherited retirement accounts.

What are the six worst assets to inherit?

Assets that often create tax or complexity problems include traditional IRAs, 401(k)s, HSAs (for non-spouse heirs), non-qualified annuities, illiquid business interests, and real estate with major debt or co-owners.

What is the 5 by 5 rule in estate planning?

It’s a trust rule that allows a beneficiary to withdraw the greater of $5,000 or 5% of the trust's value each year. It offers limited access to funds without giving full control of the trust.

Can I sell my house to my son for one dollar?

You can, but the IRS will treat the difference between the sale price and the home’s true value as a gift. That can require a gift-tax filing and may create a higher capital-gains tax bill for your child later.

Hello there! I’m Evan Melching, a Wealth Manager and AWMA™️ from Indianapolis, Indiana, specializing in financial planning, tax-saving strategies, and retirement planning. With nearly a decade of experience as a financial advisor, I’m passionate about crafting financial plans that are as unique as the person behind them. With a deep understanding of market trends, risk management, and long-term investment strategies, I empower my clients to make confidently informed decisions.

Works Cited

- Millennial-Age Parents Suffering Severe Financial Strain

- Soaring living costs push majority of parents into debt

- New moms “opt down” to lower-paying firms