Divorce and widowhood are two profound financial and emotional transitions that tend to arrive without warning. While these are two very different life events, the financial challenges overlap significantly, such as experiencing sudden changes to your income, new asset landscapes, and the need to rebuild independently. No matter which path you're navigating, a well-structured financial plan can be the difference between reacting to change and moving through it with confidence and clarity.

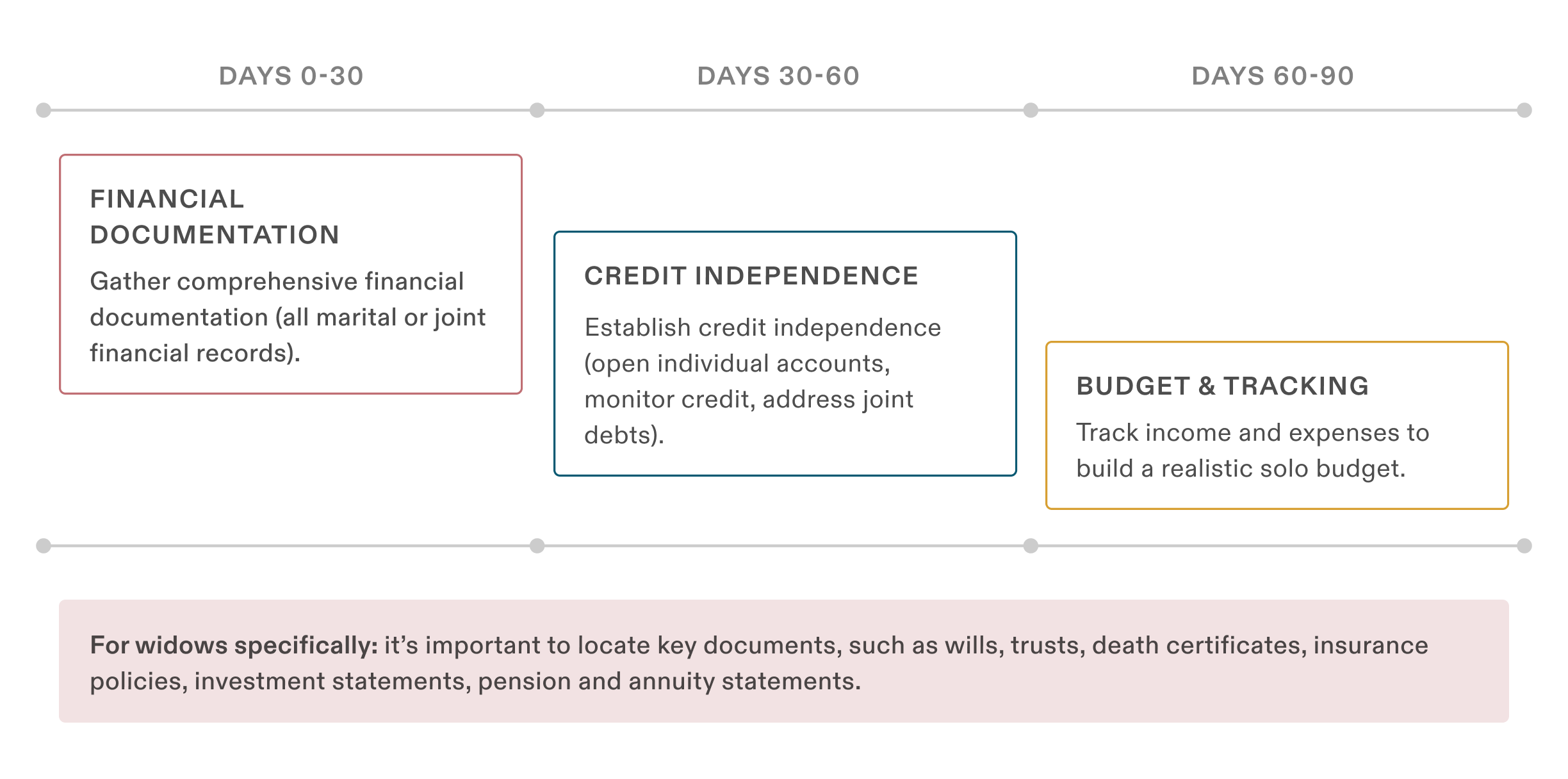

The First 30-90 Days: Immediate Action Checklist

The first step you should take in securing your financial future is establishing financial control. Consider the following actions as you plan for your new circumstance:

Understanding Your New Income Landscape

Income is often the immediate concern after either a divorce or the loss of a spouse. Many wonder where it will come from and whether it will be enough. The answers look different depending on your situation, but the urgency is the same. In fact, one-third of women fear their retirement savings won't cover their monthly expenses1. Income planning isn't optional, it’s the first thing to get right during these times.

If you're navigating divorce, spousal support and child support are often central to your near-term financial picture. Note that alimony tax rules changed in 2018. Today, if you receive alimony, it's not considered taxable income. This may sound like a good thing, but it also means the paying spouse will have no tax deduction, often affecting how willing they are to negotiate. Understanding this dynamic matters when structuring your agreement. To keep the full tax picture in mind while planning, it can be helpful to work with both a financial advisor and a family law attorney.

If you've lost a spouse, your income priorities will likely center on a few key areas. Social Security survivor benefits: when and how you claim matters significantly, and optimizing timing can increase your lifetime benefit. Life insurance proceeds are another focal point, which require a strategic decision between a lump sum or structured income. Additionally, you’ll want to ensure a thorough review of any pension or annuity payout options your spouse held.

No matter how you arrived here, two income considerations apply: your investment portfolio and your monthly cash flow. Re-evaluating your portfolio for income generation, risk tolerance, and time horizon is a critical step and is best made intentionally, not reactively. With that, rebuilding cash flow on a single-income basis means taking a close look at expenses, adjusting spending, and rebuilding emergency savings. You should come out with a budget that is sustainable and prioritizes your immediate stability and long-term financial health.

Asset Division & Retirement Accounts – What You Need to Know

Dividing assets during a major transition oftentimes shape outcomes beyond the financial decision itself. This transition is often complex and can be easily misunderstood. For example, during a divorce, fair doesn't always mean equal, and that the after-tax value of assets matters as much as the face value. It’s important to consider the following:

- Equitable vs. equal distribution: Equitable distribution ensures a fair division, which is not always a 50/50 split. Deciding what's truly fair can sometimes require forensic accounting.

- QDROs: Qualified Domestic Relations Order (QDROs) are legal documents typically found in a divorce agreement, required when dividing retirement plans governed by ERISA. They recognize that a spouse, former spouse, child, or other dependent is entitled to receive a predefined portion of the account owner’s retirement plan assets. Without a QDRO, funds may not be accessible, taxed, or penalized.

- The tax implications: Asset division carries real tax consequences depending on what you receive. For example, a Traditional IRA is subject to ordinary income tax on every distribution. That means a $1M IRA is worth much less after tax than a $1M brokerage account.

- Beneficiary and titling updates: In both divorce and widowhood, beneficiary designations and account titling require immediate updates. Many tend to overlook this, but it's an important step, as outdated designations can override even a will if left unchanged.

A fiduciary advisor serves as a valuable partner during this process, providing objective analysis to help achieve a settlement that preserves your long-term interests.

Reassessing Your Investment Portfolio

The weight of becoming a widow or divorcee can feel overwhelming in many ways, emotionally, logistically, and financially. In moments like these, giving yourself grace during the first 6 to 12 months before making any major financial decisions can help prevent irreversible actions.

- Your old portfolio may no longer fit your life: A transition often means your risk tolerance, time horizon, and income needs have all shifted at the same time. The portfolio that made sense in a dual-income household may no longer match with your lifestyle.

- Re-evaluate asset allocation: Walk through what a portfolio reassessment entails: income needs, liquidity, growth vs. preservation balance, and the longer planning horizon women face given longevity.

- Avoid reactive decisions: Major moves made in the first year such as selling investments, cashing out retirement accounts, or dramatically shifting allocations, are often driven by emotion rather than strategy, and can have lasting consequences.

A fiduciary advisor can assist you in re-evaluating and rebalancing for your new reality, helping you see the long-term impact of decisions rather than making rash ones in the moment.

Once the dust settles, a thoughtfully reassessed portfolio becomes one of the most powerful tools for long-term financial independence.

Avoiding Common Pitfalls

After losing a spouse or going through a divorce, many women encounter complex financial decisions, while simultaneously processing complex and emotional stress. A trusted financial advisor acts as a buffer, and can help guide you to long-term security. Some of the most common mistakes in the first year you’ll want to lookout for are:

- Avoiding scams: Be cautious of unsolicited financial offers. You should verify any opportunity with a trusted advisor before taking any action.

- Avoiding rushed decisions: Major financial moves made in the first year are challenging or impossible to undo. It’s best to allow yourself time to emotionally process before making significant changes to your investments, real estate, or retirement accounts.

- Don't overlook the details: Update beneficiary designations, account titling, estate documents, and healthcare coverage, are crucial and can have serious long-term consequences.

- Don't navigate your circumstance alone: A fiduciary advisor can provide guidance and an objective analysis to help you reach decisions that protect your long-term goals.

Long-Term Rebuilding – Retirement Catch-Up and New Goals

A strong financial plan should grow and adjust with each stage of your life. Post-transition, focus on rebuilding toward a secure and independent future:

- Catch-up contributions: For those over the age of 50, the IRS allows additional contributions to 401(k)s, IRAs, and similar accounts. This can be a powerful tool for closing any savings gap created by the transition.

- Spousal IRAs: If you're re-entering the workforce or are on reduced income, a higher-earning partner in a future relationship (or a current one navigating divorce) can fund an IRA in your name, helping to build independent retirement wealth.

- Update your estate plan: You’ll want to establish or revise your will, powers of attorney, and beneficiary designations to reflect your new circumstances. These documents are the foundation of ensuring your wishes are honored.

- Reset your goals: What does a secure, independent future look like for you now? Proactively addressing retirement, income, and legacy planning is how women build financially secure and empowering legacies.

Ready to build your financial roadmap? A Savvy advisor can help ensure your plan is personalized, resilient, and adaptable – no matter what life brings. Reach out to us to get started.

.webp)

[1] 25 Facts About Women's Retirement Outlook - Transamerica Institute (2025)

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy. All advisory services are offered through Savvy Advisors, Inc. (“Savvy Advisors”), an investment advisor registered with the Securities and Exchange Commission (“SEC”).