A Constructive Start, With Differentiation Taking Hold

January opened 2026 with a constructive tone for global markets, though the message beneath the surface was more nuanced than headline returns alone might suggest. After a year defined by disinflation, policy inflection points, and episodic uncertainty, investors entered the new year focused less on whether conditions were improving and more on where growth, earnings, and policy ultimately settle.

In contrast to December’s consolidation, January marked a shift toward differentiation. Equity markets generally moved higher, but leadership broadened unevenly across regions, sectors, and styles. At the same time, policy expectations became more measured, with investors balancing progress on inflation against signs of a slowing, but still resilient, global economy.

Noteworthy Developments

January also included several notable developments that helped shape market sentiment, even as their longer-term implications continue to evolve.

Most prominently, President Trump nominated Kevin Warsh to serve as the next Chair of the Federal Reserve, pending Senate confirmation. While the nomination process remains in its early stages, markets largely viewed the announcement as a reminder that leadership and institutional continuity at the Federal Reserve will remain an important part of the policy backdrop in 2026.

Trade and tariff policy also re-entered the market conversation during the month, particularly in the context of global supply chains and election-year positioning. While no immediate changes were enacted, renewed rhetoric underscored that trade policy remains a potential source of volatility for global markets, especially for export-oriented sectors and regions.

Geopolitical risks remained elevated, including ongoing tensions in the Middle East and Eastern Europe, though markets generally treated these developments as ongoing rather than escalating. As a result, their impact on broader risk sentiment was limited, even as they continued to influence energy markets and regional risk premia.

Fiscal considerations stayed in focus as well. Following the resolution of the late-2025 government shutdown, attention shifted toward government funding dynamics, Treasury issuance, and longer-term deficit considerations, all of which continue to factor into discussions around interest rates and financial conditions.

Finally, early earnings season commentary provided initial insight into corporate expectations for 2026. Management guidance around demand trends, margins, labor conditions, and capital spending drew more attention than headline results, reinforcing the market’s shift toward fundamentals and earnings durability.

January Highlights

The start of the year was supported by a steady flow of economic data and the Federal Reserve’s decision to pause after delivering multiple rate cuts in 2025.

Federal Reserve Update

At its late-January meeting, the Federal Open Market Committee held the federal funds target range steady at 3.50%–3.75%. Policymakers reiterated a patient, data-dependent approach, emphasizing that future adjustments would depend on the evolution of inflation, labor market conditions, and broader financial stability. Markets largely interpreted the decision as confirmation that policy is now operating closer to neutral, with the pace of further easing likely to slow.

Equity Performance

U.S. equity markets posted modest gains in January, building on year-end stability. The S&P 500 advanced for the month, while performance across other indices varied more widely as investors reassessed positioning and relative valuations at the start of the year.

Technology and Growth Leadership

The Nasdaq Composite also finished January higher, supported by continued interest in select technology and AI-related themes. However, performance dispersion within the sector increased, reflecting greater scrutiny of earnings quality, capital spending discipline, and longer-term growth assumptions.

Featured Theme: From Alignment to Differentiation

January represented a shift from the alignment that defined December to a period of more selective market behavior. With inflation continuing to cool and policy uncertainty reduced, investors increasingly focused on fundamentals rather than broad macro narratives.

This transition was evident in earnings commentary, sector-level performance, and regional differences. Markets appeared less reactive to individual data points and more focused on how growth, margins, and balance sheets may evolve in an environment where policy is no longer moving aggressively in either direction.

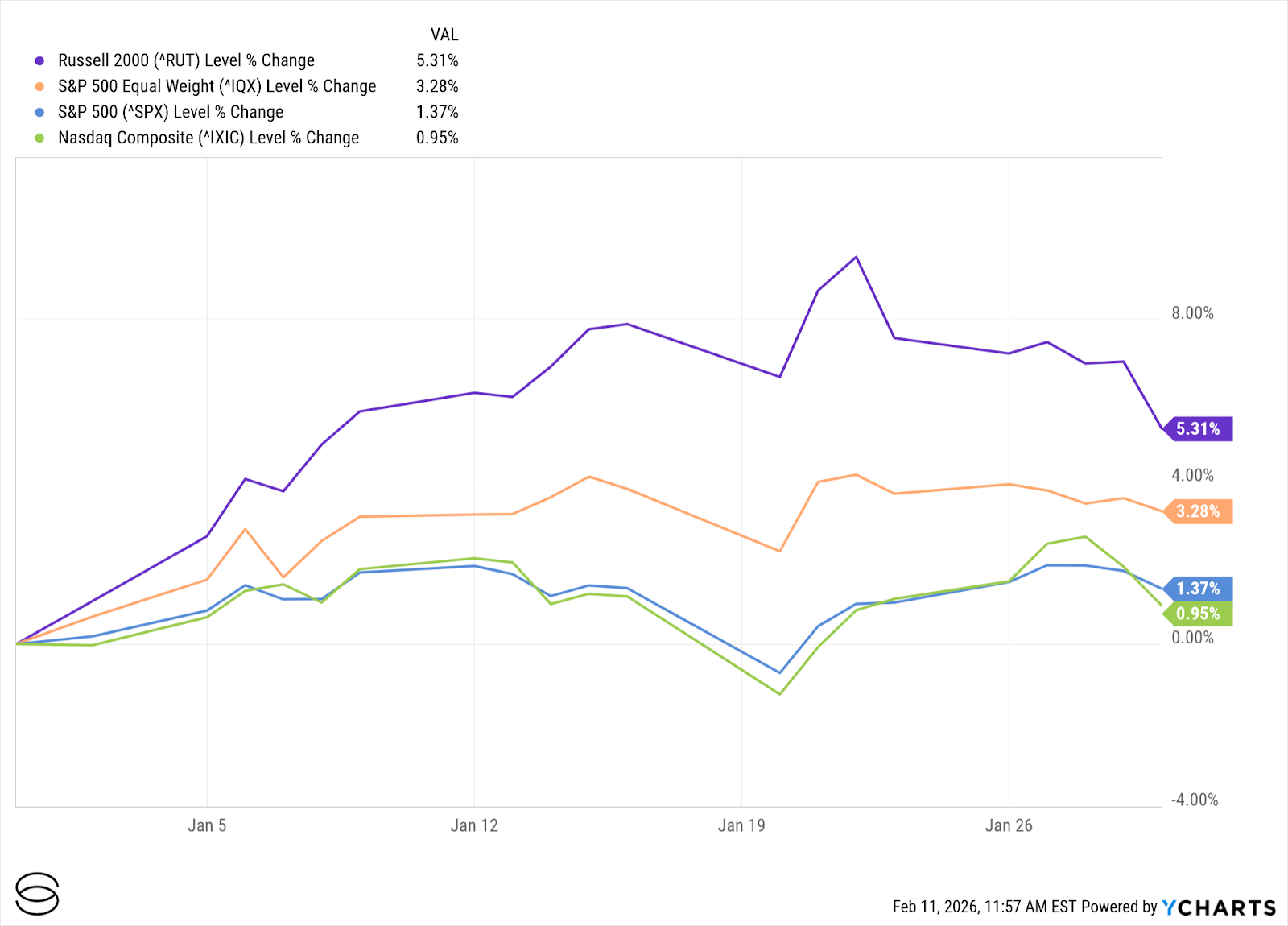

U.S. Markets: Selectivity Beneath Steady Headlines

January equity performance reflected a meaningful shift beneath headline index returns, with broader participation across market capitalizations and styles. Small-cap equities led the market for the month, with the Russell 2000 posting the strongest gains, while the S&P 500 Equal Weight Index also outperformed its cap-weighted counterpart.

By contrast, the cap-weighted S&P 500 and the technology-heavy Nasdaq Composite delivered more modest returns. This divergence suggests that market gains in January were driven less by the largest index constituents and more by a wider set of companies, including smaller and mid-sized firms.

Taken together, the performance pattern points to improving breadth, as returns were distributed more evenly across the market rather than concentrated in a narrow group of large-cap leaders. This shift highlights a market environment that is increasingly sensitive to company-specific fundamentals and sector exposures, rather than dominated solely by index-level momentum.

Exhibit 1: U.S. Equity Performance (January 2026)

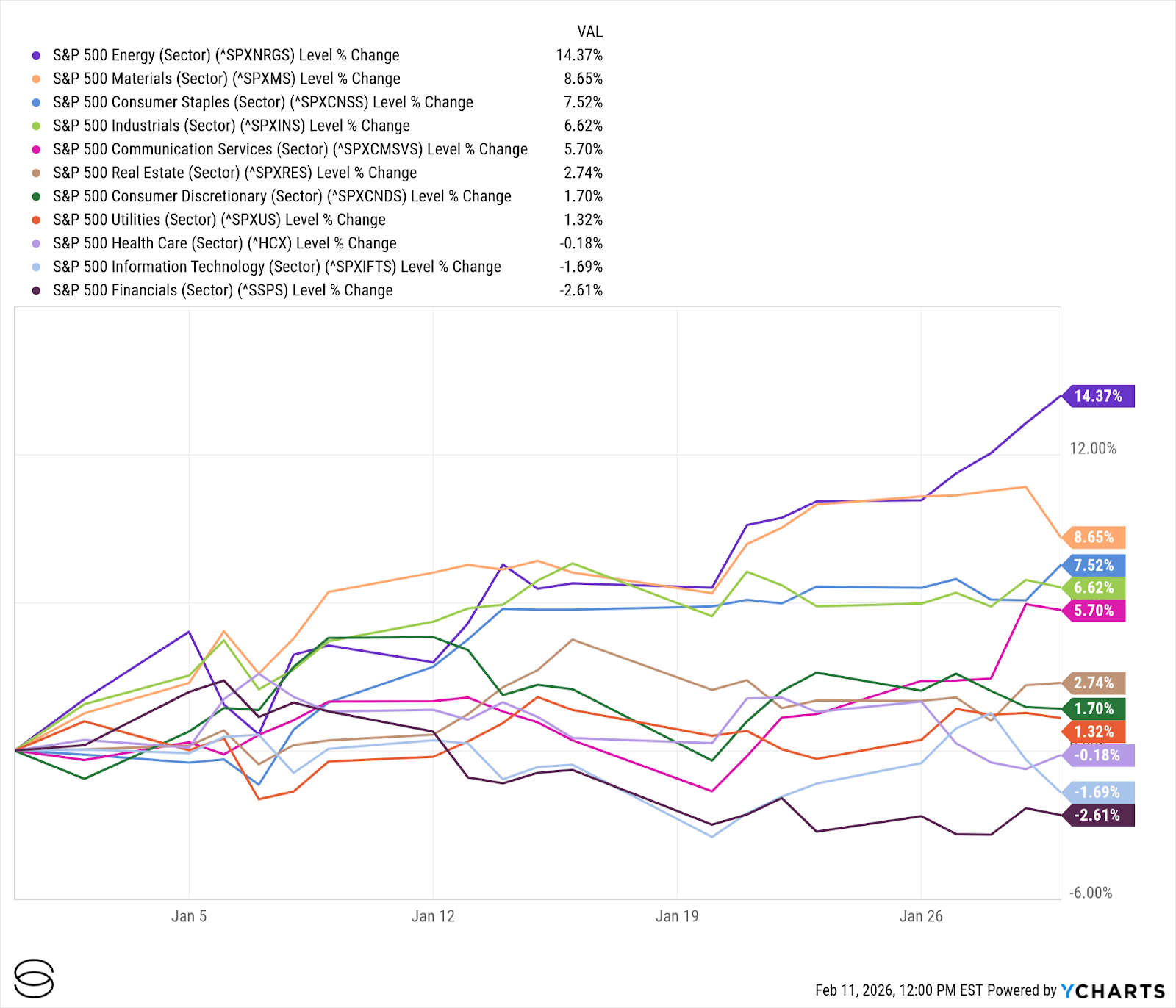

Sector Performance

Sector performance in January was notably uneven and reflected a clear shift toward cyclical and inflation-sensitive areas, rather than the rate-sensitive leadership that characterized parts of late 2025.

Energy emerged as the strongest-performing sector, posting double-digit gains for the month, supported by higher crude prices, improved supply discipline, and renewed geopolitical risk premia. Materials also delivered strong returns, benefiting from firmer commodity prices and improving sentiment around global industrial activity.

Several traditionally defensive sectors performed well. Consumer Staples and Industrials posted solid gains, reflecting continued demand stability and selective strength in areas tied to manufacturing, logistics, and essential consumption.

By contrast, Information Technology and Financials underperformed during the month. Technology declined modestly as investors digested prior gains and reassessed valuations following a strong 2025. Financials lagged amid a flatter yield curve and reduced expectations for near-term earnings acceleration tied to rate dynamics.

Communication Services posted positive but more moderate gains, while Utilities and Consumer Discretionary advanced modestly, reflecting mixed signals around growth and rates. Health Care finished roughly flat, as strength in certain subsectors was offset by broader consolidation following earlier outperformance.

Overall, January’s sector dispersion highlighted a market that is becoming increasingly selective, with performance driven more by near-term fundamentals, commodity exposure, and positioning dynamics than by broad macro trends.

Exhibit 2: U.S. GICS Sector Performance (January 2026)

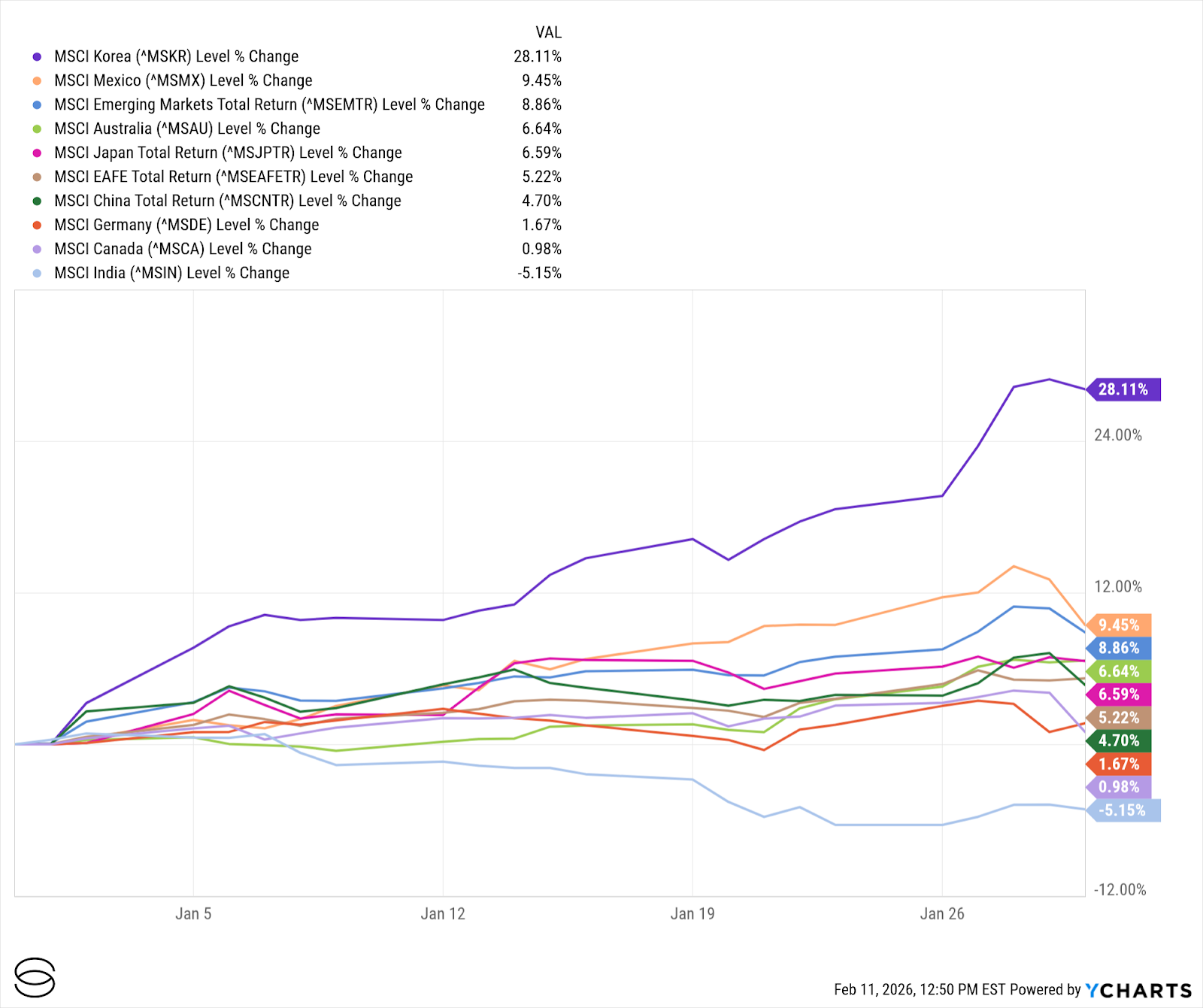

International Developed and Emerging Markets

International equity performance in January was defined by significant country-level dispersion, as local fundamentals and sector composition outweighed broad regional trends. South Korea was a primary leader, with performance catalyzed by a record-breaking export print. Outbound shipments surged 33.9% year-over-year, fueled by a 103% jump in semiconductor exports as global demand for AI-related hardware intensified. Japan also maintained its 2025 momentum; despite a January rate hike by the Bank of Japan, resilient corporate earnings and ongoing governance reforms supported exporters and kept the Nikkei 225 on a solid footing.

The broader MSCI EAFE Index advanced a more modest 5.2%. Australia outperformed as the ASX 200 reached fresh record highs on a revival in the "commodity supercycle" and peak gold prices. Conversely, Germany and Canada lagged the group. Germany’s industrial sector faced persistent manufacturing headwinds, while Canada’s performance was tempered by trade policy uncertainty and a cautious outlook on domestic consumption.

Emerging markets delivered strong aggregate gains with the MSCI EM Index rising 8.9%, though leadership remained uneven. Mexico stood out as a primary winner, rewarding the structural shift toward "nearshoring" in North American supply chains. While China saw moderate gains from targeted mortgage rate cuts and holiday consumption, it lagged the tech-driven surges seen in neighboring markets. Meanwhile, India underperformed the broader emerging‑markets index, extending a difficult 2025 in which Indian equities lagged most EM peers, as valuations remained elevated in the low‑20s on a forward P/E basis.

Exhibit 3: International Equities Performance (January 2026)

Cross-Asset Performance: Rates, Commodities, and Currencies

Fixed Income

Bond markets were largely range-bound in January as investors adjusted to the Federal Reserve’s decision to pause after multiple rate cuts in 2025 and reassessed the likely trajectory of policy for the year ahead. With inflation continuing to moderate but fiscal dynamics and growth uncertainty still in focus, rates oscillated within a relatively narrow range rather than trending decisively in either direction.

The 10-year Treasury yield moved both higher and lower over the course of the month before ending near recent levels. This reflected a balance between several competing forces: easing inflation pressures that supported duration, ongoing Treasury issuance and deficit considerations that limited upside for bond prices, and economic data that pointed to slowing but still resilient growth.

Credit markets were similarly subdued. Investment-grade and high-yield bonds posted modest returns, as tighter spreads entering the year left less room for further compression absent clearer signs of accelerating growth or policy easing. Issuance remained active, but demand was selective, with investors continuing to differentiate based on balance-sheet strength and refinancing needs.

Overall, January’s fixed income performance highlighted a market transitioning from reacting to policy inflection points toward evaluating steady-state conditions, with bond returns driven more by carry and income than by price appreciation amid a largely stable rate environment.

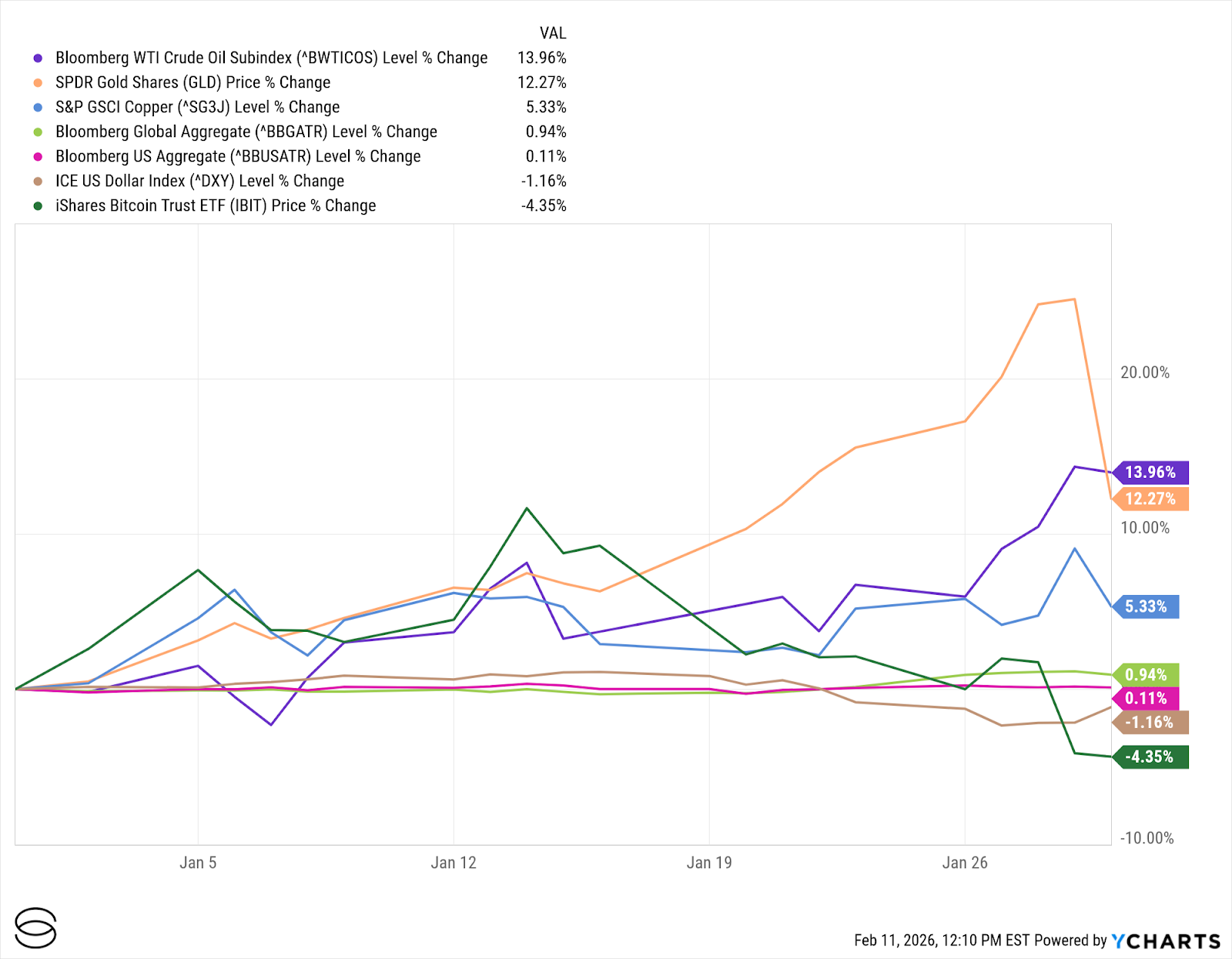

Commodities and Other Assets

Cross-asset performance in January was marked by elevated volatility and sharp dispersion across real assets. Energy and precious metals delivered strong headline gains, while other asset classes experienced more uneven trading as investors navigated shifting expectations around inflation, growth, and policy.

Energy was the clear outperformer, with crude oil posting a double-digit gain for the month. Performance reflected a combination of tighter supply dynamics, geopolitical risk premia, and improving sentiment around global demand early in the year.

Precious metals also saw significant movement, with gold delivering strong gains but experiencing notable swings over the course of the month. Price action reflected changing expectations around real yields, currency movements, and investor demand for hedges amid ongoing policy and geopolitical uncertainty. Industrial metals such as copper advanced as well, supported by improving sentiment around manufacturing activity and infrastructure-related demand.

By contrast, digital assets were highly volatile, with Bitcoin experiencing sharp intra-month moves before finishing January lower. Price action highlighted the continued sensitivity of digital assets to liquidity conditions, risk sentiment, and positioning, even as broader financial markets remained relatively stable.

Overall, January’s cross-asset performance reinforced a market environment where inflation-sensitive assets and commodities responded quickly to shifts in sentiment, while assets more closely tied to liquidity conditions experienced sharper reversals.

Exhibit 4: Cross-Asset Performance (January 2026)

Economy and Policy: A Clearer Data Flow

With the government shutdown behind us, January benefited from a more complete and timely set of economic data. December inflation readings confirmed continued progress on disinflation, while labor market data pointed to gradual cooling rather than abrupt deterioration.

Together, the data reinforced the view that the economy is slowing in an orderly fashion. Policymakers emphasized that this environment allows for greater patience, with future decisions guided by trends rather than short-term volatility.

Key Dates to Watch in February 2026

- February 6: January Employment Situation Report

- February 11: January CPI Inflation Data

- February 13: University of Michigan Consumer Sentiment (Preliminary)

- February 17: U.S. Retail Sales (January)

- February 19: Release of January FOMC Meeting Minutes

- February 24: Consumer Confidence Index

- February 25: Second Estimate of Q4 2025 GDP

- February 27: Personal Consumption Expenditures (PCE) Price Index

Conclusion: A Measured Start to a New Phase

January marked a constructive, if more selective, start to 2026. Markets appeared less focused on broad macro inflection points and more attentive to underlying fundamentals, regional differences, and sector-specific dynamics.

While uncertainties remain around growth, policy timing, and earnings sustainability, the early tone of the year suggests a market transitioning from adjustment to evaluation. After a period dominated by macro extremes, January’s price action points to an environment where differentiation, rather than direction, may play a larger role in shaping outcomes in the months ahead.

Anshul Sharma is Chief Investment Officer at Savvy Wealth, where he oversees the firm’s investment strategy, portfolio design, and platform innovation. He partners across product, marketing, and operations teams to deliver portfolios that take a methodological approach to balance customization with scalability for advisors and their clients. Before joining Savvy, Anshul spent nearly two decades at Bank of America, where he managed the Chief Investment Office’s Sustainable Model Portfolio Suite, launched new proprietary offerings, and, as Head of Alternative Investment Strategy, provided guidance and thought leadership to advisors around hedge fund, private market, and real asset strategies. He began his career as an Investment Strategist at U.S. Trust, designing multi-asset portfolios for high-net-worth and institutional clients. Anshul holds a Master of Financial Engineering from UC Berkeley and a Bachelor of Computer Engineering from Lehigh University. Outside of work, he is an avid tennis player, enjoys time with his wife, two sons, and their Bernedoodle, and is an auto enthusiast who loves cooking and travel.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Inc. is a technology company. Savvy Advisors, Inc. is an SEC registered investment advisor. For purposes of this article, Savvy Wealth and Savvy Advisors together are referred to as “Savvy”. All advisory services are offered through Savvy Advisors, while technology is offered through Savvy Wealth. The views and opinions expressed herein are those of the speakers and authors, and do not necessarily reflect the views or positions of Savvy Advisors.