March 2026

An Energy Shock Repriced the Global Macro Narrative

March was the month the market narrative changed. What began as an uneasy backdrop shaped by softer growth, tariff uncertainty, and a broad reassessment of AI winners and losers turned into something more consequential: an oil shock. The war involving the U.S., Israel, and Iran drove the biggest one-month increase in global oil prices on record, forcing investors to reprice inflation risk, central bank expectations, and the margin for error across risk assets. By month end, the conversation had shifted from a standard growth scare to a more difficult stagflation debate.

That shift showed up clearly across markets. Global stocks suffered their worst month since September 2022, European equities posted their steepest monthly decline in nearly four years, and bond markets sold off as investors moved away from the view that 2026 would be defined by easier policy. Even the strong rally on March 31 did little to change the broader picture: March was a reset month, not a reassurance month.

Noteworthy Developments

The Market Moved From Disinflation Hope to Stagflation Risk

The most important development was the escalation in Iran and the impact on energy prices. Brent crude ended March above $100 per barrel, after at one point settling above $118 for the expiring front-month contract, and Reuters described the move as the biggest one-month increase in global oil prices in history. U.S. gasoline prices also moved back to roughly $4 per gallon, reinforcing the sense that this was not just a commodity move, but a potential macro headwind for consumers and inflation expectations.

At the same time, central bank expectations changed quickly. The Federal Reserve left rates unchanged on March 18 and said economic activity had been expanding at a solid pace, job gains had remained low, and inflation was still somewhat elevated. But by late March, markets were no longer focused on when the Fed might cut. They were focused on whether higher energy prices would keep policy tighter for longer, or even reintroduce hike risk. Futures markets had moved from pricing rate cuts to factoring in the possibility of rate increases.

And this was not just a U.S. story. The ECB also held rates steady on March 19, while explicitly acknowledging that the war in the Middle East had made the outlook significantly more uncertain by creating upside risks to inflation and downside risks to growth. The Bank of England similarly left its Bank Rate unchanged at 3.75%, citing the conflict and its inflation implications. The month served as a reminder that global central banks are still navigating inflation first, even as growth becomes less comfortable.

U.S. Equities

A Tough Month for Risk Assets

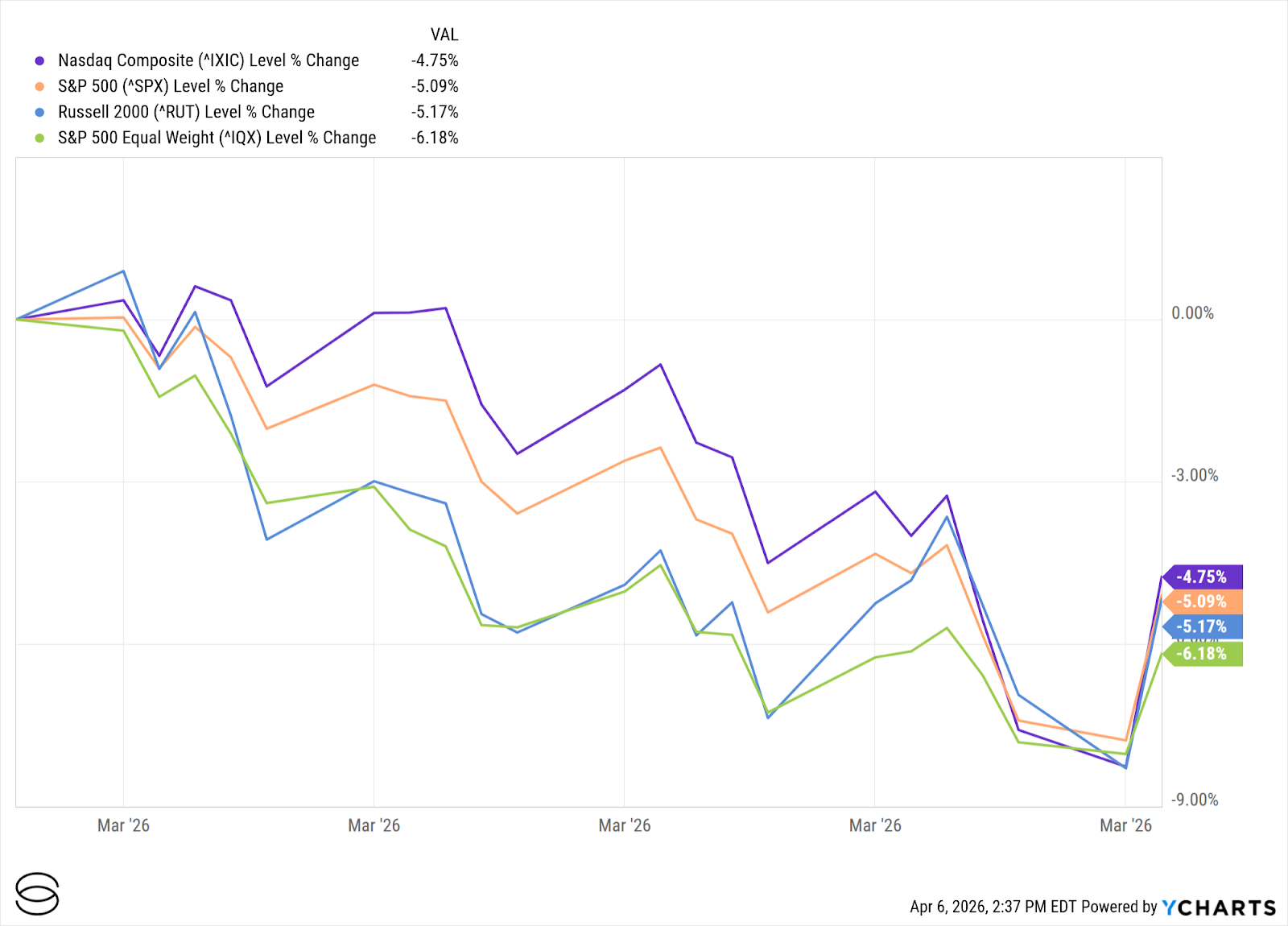

U.S. equities ended March with meaningful monthly declines, even after a sharp relief rally on the final trading day. The S&P 500 fell 5.1% on the month, while other U.S. equity indices (the Dow, Nasdaq, and Russell 2000) were also down 5.4%, 4.8%, 5.2% respectively. That is notable because it was not just a narrow tech correction. By month end, the drawdown had broadened into a more generalized de-risking episode.

The drivers were fairly clear. Rising oil prices pressured the inflation outlook. Treasury yields backed up sharply. And the market was already dealing with unresolved concerns around AI-related disruption, private credit stress, and tariff uncertainty. In the end, Q1 marked the S&P 500’s worst quarter in four years.

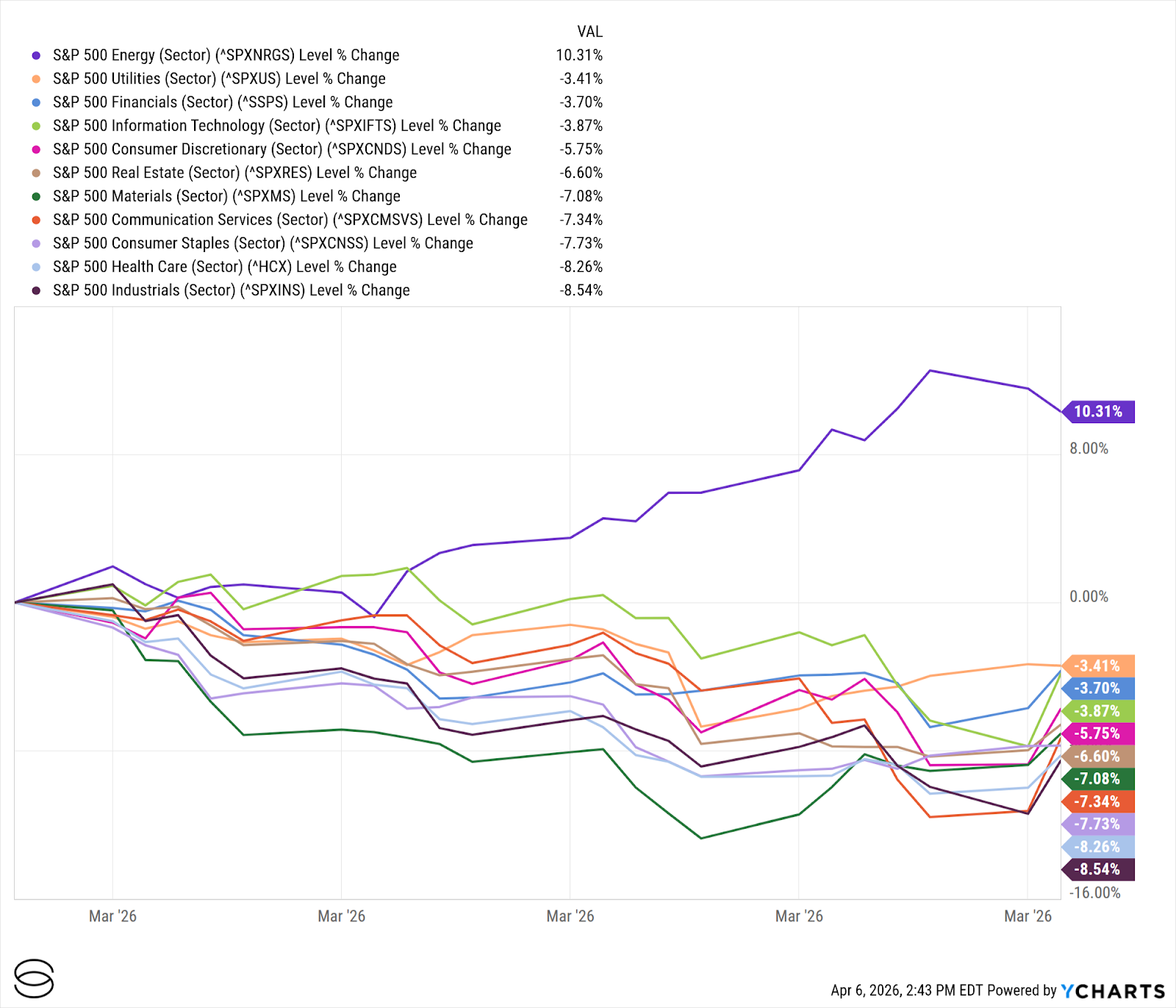

Leadership also rotated in a way that fit the macro tape. While all Magnificent Seven stocks and other higher-duration growth exposures finished down in the quarter, energy stocks remained the relative standout through much of the month, logging a 13-week winning streak by late March.

Exhibit 1: U.S. Equity Performance (March 2026)

Exhibit 2: U.S. Sector Performance (March 2026)

International Markets

The Oil Shock Went Global

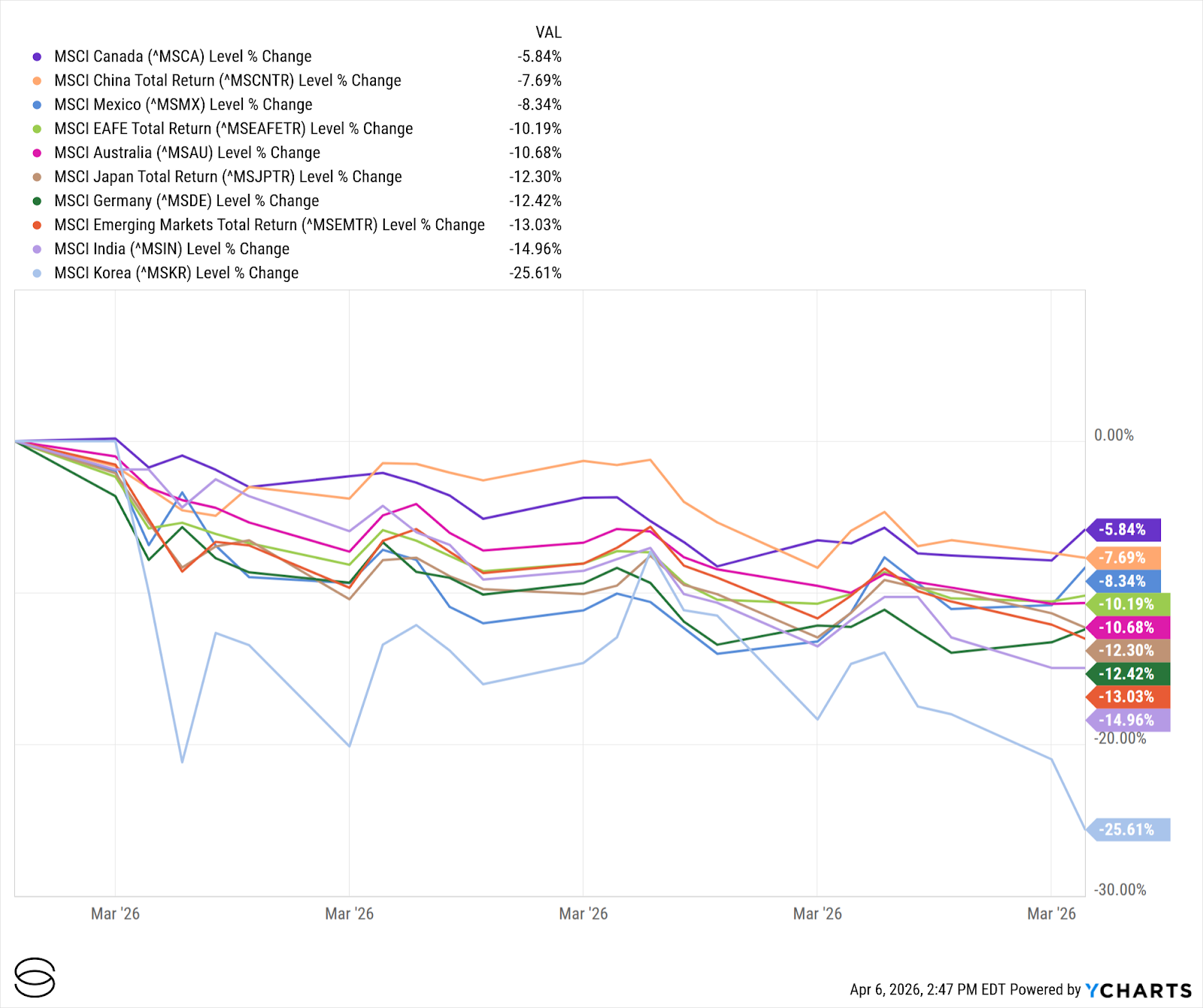

International markets fared worse than the U.S. during March’s drawdown. Europe’s STOXX 600 index fell 8.0%, its worst month since 2022 and its steepest monthly decline in nearly four years. Globally, March was the worst month for world stocks since September 2022, with roughly $8 trillion in total market capitalization erased.

Asia was hit particularly hard as much of the region remains sensitive to imported energy costs. Jittery investors pulled over $50 billion from Asian equities in March, the largest monthly outflow since at least 2008, as higher oil, rising global yields, and stagflation fears hit markets such as Taiwan, South Korea, and India. In a way, this reinforced how quickly a geopolitical shock can move from the energy complex into equities, currencies, and capital flows.

China was a partial offset, though not a full one. Beijing set its 2026 growth target at 4.5% to 5.0%, signaling a willingness to tolerate somewhat slower growth while still supporting the economy. That helped to support the view that China may be relatively better insulated than some other markets, but it was not enough to fully offset the drag from the broader oil shock and global risk-off move.

Exhibit 3: International Market Performance (March 2026)

Fixed Income and Commodities

Bonds Lost Their Cushion While Oil Took Center Stage

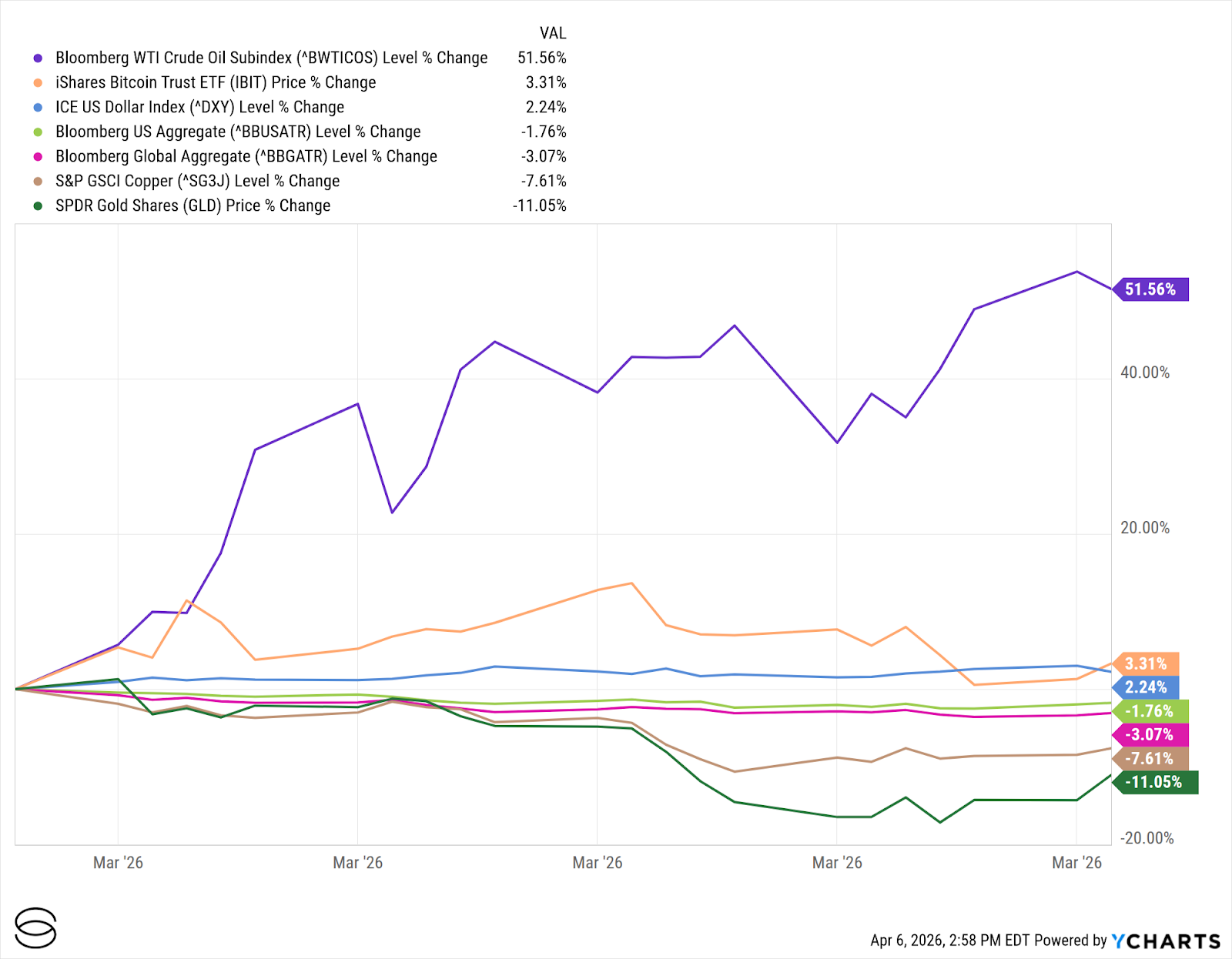

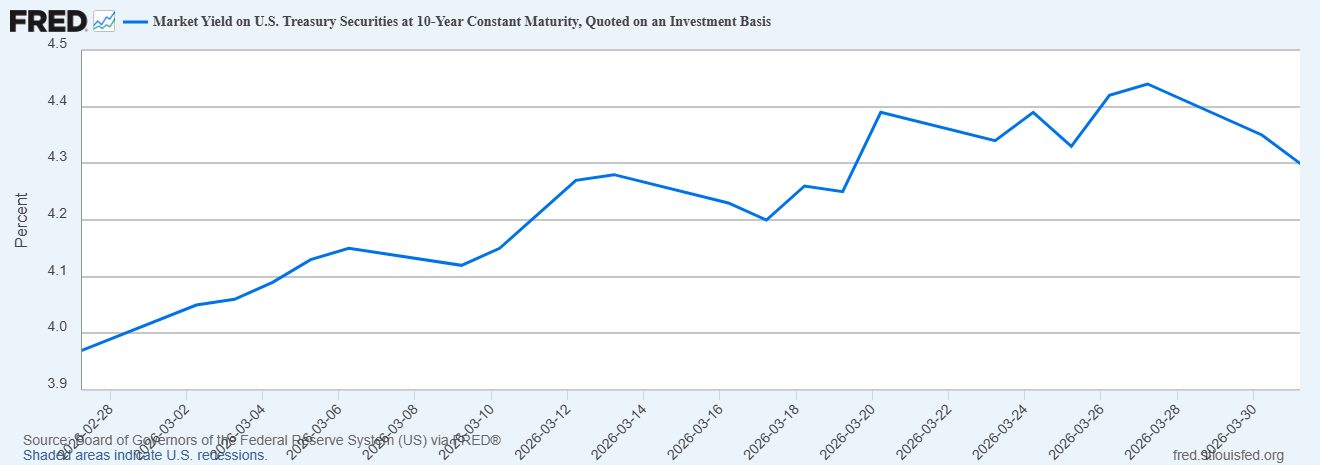

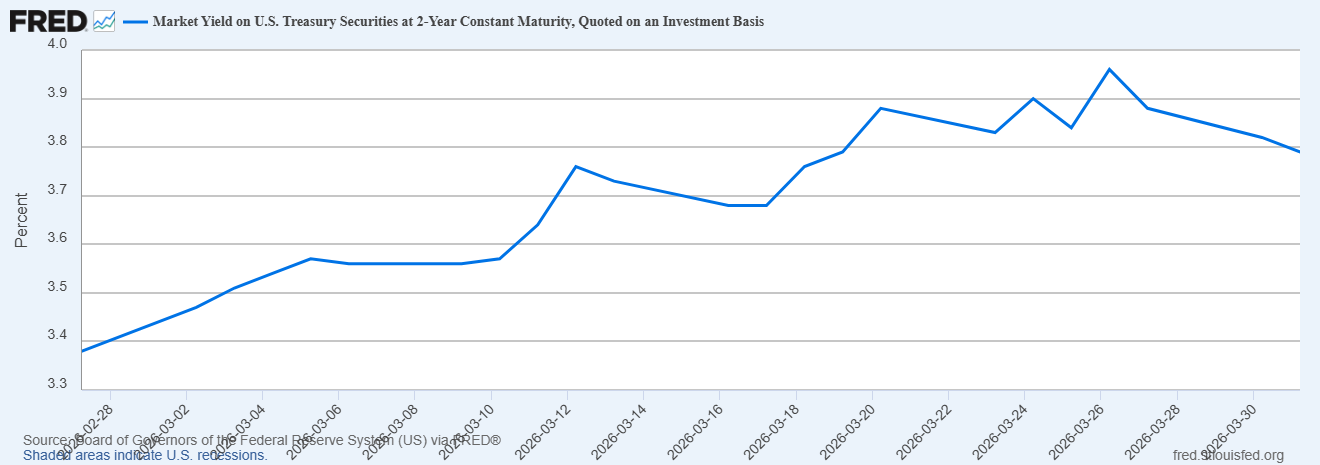

Cross-asset performance in March told a clear story: the nature of the shock mattered. The benchmark 10-year Treasury yield rose nearly 40 basis points to around 4.4%, while the 2-year yield climbed roughly 45 basis points, its largest monthly increase since October 2024. As a result, bonds did not provide their typical diversification benefit. Because the shock was inflationary, both equities and fixed income came under pressure at the same time.

Commodities, led by oil, were the epicenter. Brent crude surged and remained firmly above $100 per barrel, marking its largest monthly gain in decades. That move became the defining cross-asset signal of the month, tightening financial conditions, pushing yields higher, and challenging the assumption that central banks would be in a position to ease policy in the near term. It also raised the likelihood that inflation data in the coming months could reaccelerate after a period of relative stability.

Gold sent a more nuanced signal. While prices rebounded late in the month, the metal was still on track to finish March lower, even as the U.S. dollar strengthened. That combination highlights an important dynamic: in an energy-driven inflation shock, traditional hedges do not always respond in a linear way. In March, oil, not gold, was the asset that carried the clearest macro signal.

Exhibit 4: Cross-Asset Performance (March 2026)

Exhibit 5: U.S. 10-Year and 2-Year Treasury Yield (March 2026)

Economy and Policy

The Backward-Looking Data Stayed Calm, but Forward Risk Increased

The economic data released during March largely reflected a pre-shock environment, one that was cooling, but still relatively stable.

Inflation remained contained heading into the month. February CPI showed prices rising at a moderate pace, with core inflation still running slightly above headline levels but not reaccelerating in a meaningful way. Similarly, January PCE (released with a delay) pointed to a steady but not worsening inflation backdrop. Taken together, the data suggested that disinflation progress had slowed, but had not reversed prior to the oil-driven move higher in March.

Growth, however, was already losing momentum. The second estimate of fourth-quarter GDP was revised down to a 0.7% annualized pace, reinforcing the idea that the economy entered 2026 on softer footing than expected. Measures of underlying demand also moderated, pointing to less resilience beneath the surface.

Labor market data told a similar story. Job openings held roughly steady, but hiring slowed, suggesting a gradual cooling in labor demand. The March employment report, released on April 3rd, showed payrolls rebounding modestly and the unemployment rate holding near recent levels. While that was a constructive signal, it likely does not yet reflect the full impact of March’s energy shock on hiring and business sentiment.

The key takeaway is that the data entering March did not point to an economy under immediate stress. But it also did not leave much of a buffer. As the inflationary impulse from higher energy prices is arriving at a time when growth is slowing, it may raise the risk of a more challenging macro mix in the months ahead.

Key Dates to Watch in April 2026

Markets will be watching to see whether March’s energy spike starts to show up more clearly in inflation, spending, and business sentiment data. The key U.S. dates are:

April 9: Personal Income and Outlays (including PCE inflation) + Q4 GDP (third estimate)

April 10: March CPI

April 14: March PPI

The Bottom Line

March forced the market to confront a more complicated macro backdrop. The dominant question is no longer just whether growth is slowing or whether a handful of crowded trades have become overextended. It is whether the global economy is moving into a period where softer growth and firmer inflation coexist for longer than investors expected coming into the year.

That does not automatically mean a lasting regime shift is here. A meaningful de-escalation in the Middle East and a reversal in oil could still ease pressure on rates and inflation expectations. But March clearly raised the bar for risk assets and made the macro path less forgiving. In the end, this was a month that reminded investors how quickly geopolitical stress can become a market-wide repricing event.

Anshul Sharma is Chief Investment Officer at Savvy Wealth, where he oversees the firm’s investment strategy, portfolio design, and platform innovation. He partners across product, marketing, and operations teams to deliver portfolios that take a methodological approach to balance customization with scalability for advisors and their clients. Before joining Savvy, Anshul spent nearly two decades at Bank of America, where he managed the Chief Investment Office’s Sustainable Model Portfolio Suite, launched new proprietary offerings, and, as Head of Alternative Investment Strategy, provided guidance and thought leadership to advisors around hedge fund, private market, and real asset strategies. He began his career as an Investment Strategist at U.S. Trust, designing multi-asset portfolios for high-net-worth and institutional clients. Anshul holds a Master of Financial Engineering from UC Berkeley and a Bachelor of Computer Engineering from Lehigh University. Outside of work, he is an avid tennis player, enjoys time with his wife, two sons, and their Bernedoodle, and is an auto enthusiast who loves cooking and travel.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Inc. is a technology company. Savvy Advisors, Inc. is an SEC registered investment advisor. For purposes of this article, Savvy Wealth and Savvy Advisors together are referred to as “Savvy”. All advisory services are offered through Savvy Advisors, while technology is offered through Savvy Wealth. The views and opinions expressed herein are those of the speakers and authors, and do not necessarily reflect the views or positions of Savvy Advisors.