May showed that strong earnings and continued enthusiasm around AI can still support risk assets, even when interest rates remain elevated and inflation risks are still present.

After April’s sharp rebound, investors entered May focused on whether earnings momentum could continue, whether the rally could broaden, and whether easing energy prices would reduce pressure on inflation and the Federal Reserve. By month end, the answer was mixed but constructive. U.S. equities moved higher again, major indexes reached new highs, and technology leadership remained powerful. At the same time, market breadth narrowed, Treasury yields moved higher, and the Fed’s path became less supportive as investors increasingly debated whether the next policy move could eventually be a hike rather than a cut.

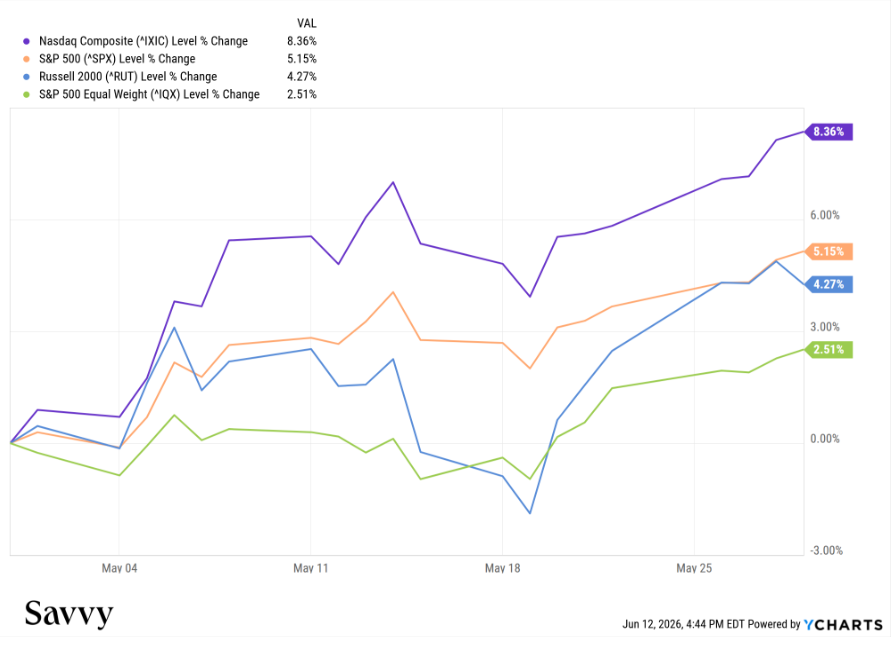

The gains were meaningful. The S&P 500 rose 5.2% in May, extending its rally from the April lows and finishing the month at a record high. The Nasdaq Composite gained 8.4%, again leading major U.S. indexes as AI, semiconductors, software, and cloud infrastructure remained the dominant market themes. The Dow advanced more modestly, while the Russell 2000 gained 4.3% as small caps continued to participate in the broader recovery.

May’s market backdrop was therefore constructive, but not without tension. The equity rally was increasingly concentrated in technology and AI-linked companies, while many traditional sectors lagged or declined. Oil prices moved lower late in the month, helping risk appetite, but inflation data remained firm enough to keep the Fed cautious. Treasury yields rose, the yield curve flattened, and rate-cut expectations continued to fade.

The month’s takeaway is that earnings momentum remains the strongest support for equities, but the market is becoming more dependent on a narrower set of growth drivers.

Noteworthy Developments

AI Leadership Became Even More Important

The most important development in May was the continued dominance of AI-linked market leadership.

Technology was the clear driver of U.S. equity returns. The S&P 500 Information Technology sector rose roughly 16% in May, far outpacing the broader index. Semiconductors and software both participated, supported by continued demand for AI infrastructure, data-center buildouts, cloud spending, and power-related investment. The semiconductor complex remained especially strong, extending the powerful move that began in April.

That leadership helped the major indexes move higher, but it also highlighted a growing concentration issue. While the S&P 500 posted a strong monthly gain, most sectors did not keep pace with the index, and several finished lower. Technology was the only sector to materially outperform, while areas such as Energy, Utilities, and Consumer Staples lagged. In other words, the headline index performance was strong, but the underlying composition was less broad than it appeared.

This does not mean the rally was purely speculative. Earnings results continued to support the move, and many AI-linked companies delivered real revenue growth, margin expansion, and stronger forward guidance. The market was not simply paying higher multiples for the same earnings stream; it was rewarding companies that are benefiting from a major capital spending cycle.

Still, the bar is rising. When leadership becomes concentrated in a handful of themes, the market becomes more sensitive to earnings disappointments, capex guidance, and valuation resets in those areas. May reinforced that AI remains the central investment theme of 2026, but it also showed that broader market participation will be important if the rally is going to remain durable.

U.S. Equities

Another Strong Month, but Narrower Under the Surface

U.S. equities advanced again in May, building on April’s rebound and pushing major indexes to new highs.

The S&P 500 gained 5.2% for the month, while the Nasdaq Composite rose 8.4%. The Nasdaq 100 also outperformed, supported by strength in semiconductors, software, cloud infrastructure, and large-cap technology. The Dow gained more modestly, reflecting its lower exposure to the highest-growth areas of the market. Small caps also participated, with the Russell 2000 rising 4.3% and maintaining strong year-to-date gains.

The quality of the rally was mixed. On one hand, record highs across major indexes, continued small-cap participation, and strong earnings delivery all pointed to a resilient equity backdrop. On the other hand, sector performance showed that leadership was highly concentrated. Technology gained roughly 16%, while many of the more defensive and rate-sensitive areas of the market declined.

Large-cap growth continued to outperform value, and companies tied to AI infrastructure remained the clearest beneficiaries of investor demand. Data-center spending, chip demand, cloud growth, software monetization, and power infrastructure continued to support the view that AI remains a multi-year capital spending cycle.

Small-cap strength was encouraging, but the path remains more complicated. Smaller companies tend to be more sensitive to interest rates, credit conditions, and domestic earnings trends. With the 10-year Treasury yield still elevated and the Fed showing little urgency to ease, small caps may need a more stable rate environment to sustain leadership.

From a portfolio perspective, May was another constructive month for equity exposure, particularly for investors with exposure to quality growth, technology, and AI-linked themes. The main risk is that market leadership has become more concentrated, which raises the importance of earnings execution from the companies carrying the rally.

Exhibit 1: U.S. Equity Performance

Exhibit 2: U.S. Sector Performance

International Markets

International Equities Participated, With EM Technology Leading

International markets also moved higher in May, though performance continued to differ meaningfully by region.

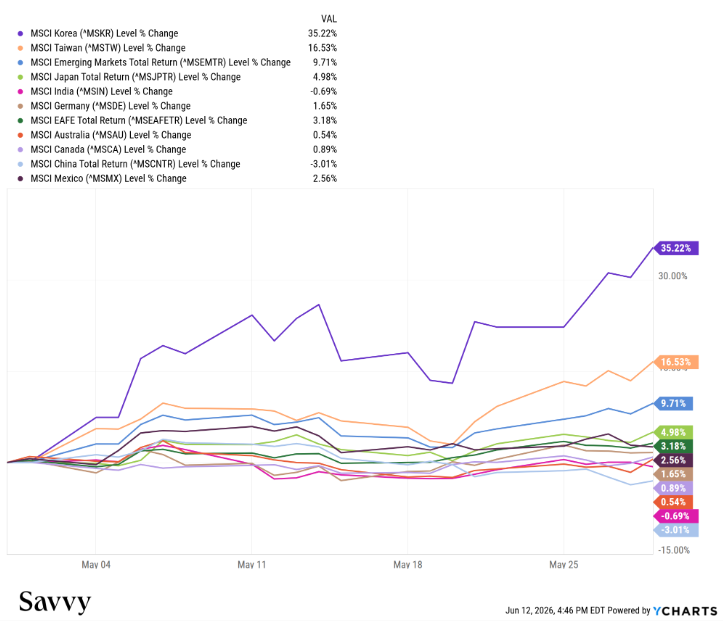

Developed international equities gained ground but generally lagged U.S. equities. The MSCI EAFE Index rose roughly 3.2% in May, helped by improving global risk appetite, a weaker euro, and better performance in Japan and other AI-sensitive markets. European equities also advanced, with the STOXX Europe 600 gaining roughly 3.2% for the month.

Emerging markets were stronger. The MSCI Emerging Markets Index rose roughly 9.7% in May, helped by the same technology and semiconductor themes that supported U.S. markets. Taiwan, South Korea, and other parts of the Asian technology supply chain remained central to the global AI investment story. Semiconductor demand, memory pricing, and hardware infrastructure continued to support the region.

That said, EM performance remains increasingly tied to a narrower set of technology-related drivers. The same AI theme that helped emerging markets rally also makes the asset class more sensitive to changes in global capex expectations, semiconductor demand, and U.S. interest rates. In May, the earnings and technology tailwinds were strong enough to offset those risks. Going forward, the balance between AI-driven growth and higher U.S. rates will be important.

Europe’s setup was somewhat different. European equities benefited from the broader global rally and easing oil prices late in the month, but the region remains more exposed to energy costs and weaker growth trends. The rally was helpful, but Europe still faces a more difficult macro mix than the U.S., particularly if elevated energy prices continue to pressure consumers and industrial companies.

Exhibit 3: International Market Performance

Fixed Income and Commodities

Yields Rose, Credit Held Up, and Oil Finally Eased

Fixed income produced modestly positive returns in May, but the underlying rate backdrop remained challenging.

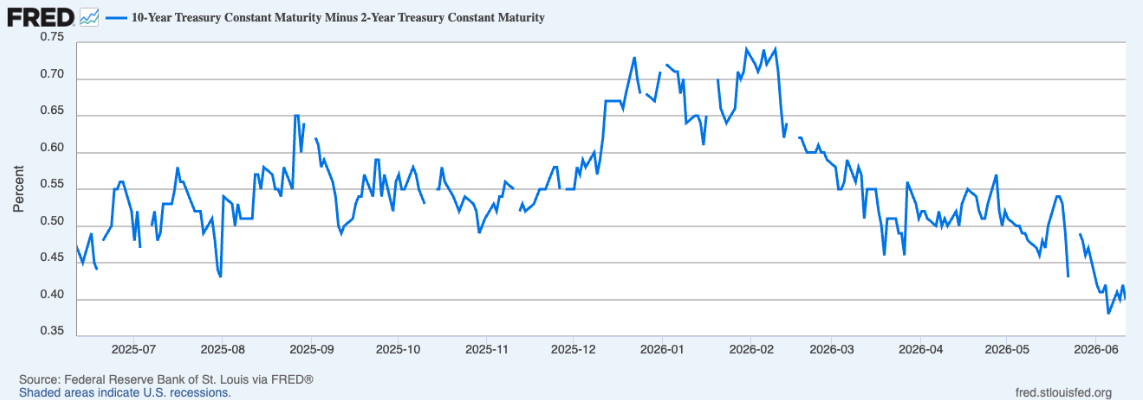

Treasury yields moved higher during the month. The 10-year Treasury yield rose roughly 7 basis points to end May near 4.44%, while the 2-year yield rose more sharply as investors priced in a less accommodative Fed path. The 2-year/10-year Treasury spread flattened to roughly 43 basis points, reflecting the market’s shift away from rate-cut expectations and toward the possibility that policy may need to remain restrictive for longer.

Longer-term yields also drew attention. The 30-year Treasury yield briefly moved above 5% during the month, reaching levels last seen before the global financial crisis, before finishing May just below that level. The move reflected a combination of inflation concerns, elevated oil prices, heavier Treasury supply, and a reassessment of the Fed’s policy path.

Despite the rate volatility, bonds were not broadly weak. The Bloomberg U.S. Aggregate Bond Index returned roughly 0.3% in May, helped by coupon income and tighter credit spreads. Investment-grade and high-yield corporate bonds outperformed Treasuries as credit spreads continued to tighten, reflecting resilient investor demand and confidence in corporate fundamentals.

Oil remained one of the most important macro variables, but the direction improved late in the month. After trading at elevated levels for much of the spring, crude prices fell below $100 per barrel in late May on hopes for progress in U.S.-Iran negotiations and a potential reopening of the Strait of Hormuz. West Texas Intermediate crude ended the month below $90 per barrel, a meaningful decline from prior highs.

That move helped risk sentiment because oil has been the direct link between geopolitics, inflation, consumer confidence, and Fed policy. Lower oil prices do not eliminate the inflation problem, but they reduce the immediate pressure on headline inflation and give markets more confidence that the worst of the energy shock may be easing.

Gold was less central to the cross-asset story in May. Higher real rates and improving risk appetite limited the appeal of safe-haven exposure, even though geopolitical uncertainty remained elevated.

Exhibit 4: Cross-Asset Performance

Exhibit 5: U.S. 10-Year Treasury Yield

Exhibit 6: U.S. 10-Year Minus 2-Year Treasury Yield Spread

Economy and Policy

Growth Remained Resilient, but the Fed’s Flexibility Narrowed

The May data showed an economy that continued to expand, but with inflation still too firm for the Federal Reserve to declare victory.

First-quarter real GDP was revised lower to a 1.6% annualized rate from the initial 2.0% estimate. The revision reflected softer investment and consumer spending than initially reported, although growth still improved from the 0.5% pace recorded in the fourth quarter of 2025. The economy is not accelerating sharply, but it remains resilient enough to keep recession concerns contained.

The labor market also remained steady. The April employment report showed payroll growth of 115,000 and an unchanged unemployment rate of 4.3%. Job growth was slower than in prior cycles, but still consistent with an economy that continues to expand. Importantly, the unemployment rate remained low and stable, giving the Fed little urgency to ease policy.

Consumer spending also held up. April retail sales rose 0.5% month over month and 4.9% year over year. Some of the increase reflected higher gasoline prices, but the data still pointed to a consumer sector that remained resilient despite higher rates, higher energy costs, and lingering uncertainty.

Inflation remained the bigger challenge. April PCE inflation rose 3.8% year over year, while core PCE increased 3.3%. That was above the Fed’s 2% target and reinforced the concern that energy-driven inflation could spill into broader price pressures if elevated oil prices persist.

The Fed minutes from the April 28 to 29 meeting reinforced that message. Policymakers noted that the conflict in the Middle East had continued to influence asset prices and inflation expectations. The minutes also showed increased concern that inflation could take longer to return to target, and that the policy path may need to remain restrictive for longer than investors had expected earlier in the year.

The market’s takeaway was that the bar for rate cuts has moved even higher. Earlier in 2026, investors were focused on when cuts might begin. By the end of May, the discussion had shifted toward whether the Fed might remain on hold for all of 2026, or even consider a hike if inflation fails to moderate.

Key Dates to Watch in June 2026

Markets will be watching whether May’s rally can continue in the face of incoming labor, inflation, and Fed data.

June 5: May Employment Report

June 10: May CPI

June 11: May PPI

June 16 to 17: FOMC Meeting

June 17: May Retail Sales

June 18: May Housing Starts

June 25: May Personal Income and Outlays, including PCE inflation

June 26: Final First-Quarter GDP Estimate

The Bottom Line

May delivered another strong month for risk assets, led by AI, technology, semiconductors, and resilient earnings. The S&P 500 and Nasdaq reached new highs, small caps participated, and international markets also advanced, with emerging markets benefiting from the same AI hardware cycle that supported U.S. technology shares.

The macro backdrop remained more complicated. Treasury yields moved higher, inflation stayed above the Fed’s target, and rate-cut expectations continued to fade. Oil prices eased late in the month, which helped sentiment, but energy remains a key variable for inflation, consumer confidence, and central bank policy.

The next phase for markets will likely depend on three questions: whether AI-related earnings can continue to justify strong performance, whether the equity rally can broaden beyond technology, and whether inflation data improves enough to keep the Fed on hold rather than pushing policy expectations in a more hawkish direction.

For now, earnings momentum remains the market’s strongest support. But May also showed that the rally is becoming more dependent on a narrower group of winners. That makes continued earnings delivery, stable rates, and broader participation increasingly important as investors move into the second half of 2026.

Anshul Sharma is Chief Investment Officer at Savvy Wealth, where he oversees the firm’s investment strategy, portfolio design, and platform innovation. He partners across product, marketing, and operations teams to deliver portfolios that take a methodological approach to balance customization with scalability for advisors and their clients. Before joining Savvy, Anshul spent nearly two decades at Bank of America, where he managed the Chief Investment Office’s Sustainable Model Portfolio Suite, launched new proprietary offerings, and, as Head of Alternative Investment Strategy, provided guidance and thought leadership to advisors around hedge fund, private market, and real asset strategies. He began his career as an Investment Strategist at U.S. Trust, designing multi-asset portfolios for high-net-worth and institutional clients. Anshul holds a Master of Financial Engineering from UC Berkeley and a Bachelor of Computer Engineering from Lehigh University. Outside of work, he is an avid tennis player, enjoys time with his wife, two sons, and their Bernedoodle, and is an auto enthusiast who loves cooking and travel.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation from the Savvy Investment Team. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Investment Management ("SWIM") is a proprietary, in-house investment solution offered by Savvy Advisors, Inc. (“Savvy Advisors”). It is designed to support financial advisors in the management of client portfolios. Savvy Wealth Investment Management is not a separate legal entity and is not independently registered as an investment adviser. All advisory services are provided by Savvy Advisors in its capacity as a registered investment adviser.