Buyer Beware: The Mirage of Private Credit Fund Returns

Private credit has become one of the fastest-growing corners of global finance, with industry estimates placing assets under management at roughly $2 trillion as of 2024 (IMF, Apr. 2024); industry data providers report a comparable trajectory, with the asset class reaching about $1.7 trillion in 2023 and projected to grow further (Preqin, Dec. 2024). The asset class is marketed on the promise of steady income, muted volatility, and attractive risk-adjusted returns. Yet beneath those narratives lies a structural problem: valuation opacity and the wide discretion afforded by fair-value accounting. On closer inspection, a meaningful share of reported performance can be traced not to economic fundamentals but to the latitude managers enjoy in marking illiquid assets—latitude that, in aggregate, can strain investor trust and contribute to risks across the broader financial system.

The Hidden Engine of “Success”

Private credit’s appeal rests on an intricate machinery powered by a practice both commonplace and contentious: the acquisition of distressed loans and bonds at bargain-basement prices, followed by their upward revaluation. These assets, often sold by banks constrained by regulatory capital requirements or by funds facing liquidity shortfalls, may reflect forced-seller dynamics rather than a considered assessment of intrinsic value. For private credit managers, armed with the latitude granted by accounting standards, this creates fertile ground—a chance to recalibrate “fair values” through internal models untethered from observable market transactions.

The implications ripple far beyond swelling Net Asset Values (NAVs). This alchemy crafts seductive narratives of performance, inviting fresh capital like moths to a flame while justifying hefty management fees. Yet for investors, these revaluations introduce risks—risks born not of economic reality but of managerial discretion. The glittering façade serves the architects alone, leaving others exposed to the brunt of eventual market corrections.

Decoding Level 3 Opacity

At the heart of these valuation practices lies a twilight zone of financial reporting—Level 3 assets, as delineated by accounting frameworks like ASC 820 and IFRS 13. Unlike Level 1 assets, which bask in the clarity of observable market prices, or Level 2 assets, which lean on comparable inputs, Level 3 assets are valued using unobservable inputs and management assumptions. Valuation here becomes less a discovery than a projection, shaped by manager-imposed recovery rates, discount factors, and speculative predictions of future cash flows.

Proponents of this system often laud managerial expertise as both bulwark and justification, arguing that these valuations reflect foresight and strategy. Yet the absence of external validation leaves investors navigating an opaque mire—a terrain where annual audits and Limited Partner Advisory Committees (LPACs) provide scant illumination. Within these shadowed margins of discretion, the line between prudent judgment and opportunistic adjustment dissolves, fraying confidence in the private credit ecosystem.

The Game of Winners and Losers

In this delicate construct, fund managers emerge as unambiguous beneficiaries. Their compensation, tethered to inflated NAVs, swells in tandem with perceived portfolio performance. By weaving a narrative of consistent triumph, managers attract fresh capital, expand portfolios, and bolster their fees. Yet this self-reinforcing cycle often exacts a hidden toll—the erosion of transparency and investor protection.

Sophisticated institutional investors, too, find themselves ensnared. LPACs, ostensibly guardians of oversight, often lack the tools or appetite to challenge the nuanced methodologies underpinning Level 3 valuations. Retail investors face an even steeper climb, lured by promises of stability but unarmed to decipher the intricate accounting practices shaping their returns.

Repercussions ripple outward. Sellers of distressed assets encounter artificially inflated benchmarks, forced to accept lower bids or risk losing out entirely. Misaligned capital flows steer investments into ventures predicated on rosy valuations rather than tangible performance. In a market as expansive as private credit, these distortions risk cascading into systemic instability, threatening portfolios and the broader financial landscape alike.

Secondary Markets: The Heart of the Practice

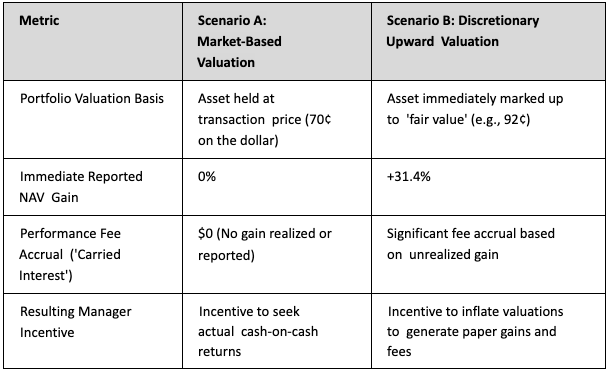

At the nexus of these valuation maneuvers lies the secondary market—a bustling arena where funds trade distressed assets to recalibrate liquidity or reposition portfolios. The anatomy of a typical transaction reveals much about the mechanisms at play. Consider a stylized example: Fund A, facing looming liabilities, sells a portfolio of underperforming loans to Fund B at 70 cents on the dollar. What often follows is a familiar pattern: Fund B revalues these assets upward, citing proprietary models and recovery projections, while setting aside the recent transaction price on the grounds that the sale was not orderly. (The figures used throughout this article are illustrative, intended to show the mechanism rather than to describe a specific transaction.)

Under fair value accounting principles, such as ASC 820 and IFRS 13, the price in an orderly transaction is often the best initial evidence of fair value. However, the mechanism for ignoring a recent transaction price typically hinges on the classification of the sale as “distressed” or “not orderly.” Fund B may argue that the sale from Fund A was forced due to liquidity constraints, thereby deeming the transaction price unreliable. This allows Fund B to rely on Level 3 “unobservable inputs,” including proprietary recovery assumptions and discount rates, to justify upward revaluations. While technically permissible within accounting standards, this practice raises critical questions about its intent and consequences.

This valuation gap, enabled by Level 3 opacity, becomes fertile ground for discretionary mark-ups cloaked as performance improvement. While the underlying economic fundamentals often remain static, these adjustments varnish NAV growth, creating an alluring facade of success. Over time, this practice pressures sellers to accept lower prices, undermining their bargaining power in a market increasingly skewed by discretionary valuations.

The Systemic Implications

As these practices proliferate, their ramifications extend far beyond individual funds. Inflated valuations corrode investor trust, distort transaction benchmarks, and confound regulatory oversight. They create precarious feedback loops: higher NAVs fuel greater leverage, magnifying exposure to economic downturns. In crises, these fragile constructs risk collapsing, dragging portfolios—and, potentially, economies—into their wake.

Regulatory bodies have begun to stir. The U.S. Securities and Exchange Commission (SEC), through its private fund adviser reforms adopted on Aug. 23, 2023 (SEC, Aug. 23, 2023), introduced measures aimed at amplifying transparency and policing valuation integrity. However, these rules were vacated in full by the U.S. Fifth Circuit Court of Appeals on June 5, 2024 (Fifth Circuit, June 5, 2024), leaving a regulatory vacuum in their wake. The absence of enforceable standards exacerbates the very risks these reforms sought to address, underscoring the urgent need for a renewed commitment to oversight and accountability.

A Close-Up on Industry Practices

For an illustration of scale and stakes, one need look no further than documented industry behaviors that epitomize the challenges of private credit valuation. Regulatory filings and investigative reports provide examples where distressed loan portfolios are acquired at sharp discounts, only to be revalued upward in time for quarter-end reporting. Justifications such as “recovery potential” and “de-risked structures” abound, yet the timing and consistency of these adjustments raise critical questions about their intent.

These practices align with structural incentives endemic to private credit, underscoring the critical need for transparency. Without rigorous disclosures and independent validation, investors remain vulnerable, navigating a landscape where managerial gains often outweigh economic substance.

Spotting the Red Flags

How, then, can investors protect themselves in this murky terrain? Vigilance is key. Indicators of valuation risks include:

- Upward markups that cluster around quarter-end or year-end reporting dates, with little corresponding change in borrower fundamentals.

- Reported fair values that diverge materially from recent transaction prices, with sales routinely reclassified as "distressed" or "not orderly" to justify ignoring observable evidence.

- Heavy reliance on Level 3, model-based valuations with limited disclosure of key inputs such as recovery rates, discount rates, and default assumptions.

- Absence of sensitivity analysis showing how NAV would move under reasonable changes in those key assumptions.

- Reported returns that are smoother than the underlying credit environment—or peer funds with comparable exposures—would suggest.

- Performance fees or carried interest accruing on unrealized, marked-up gains rather than on realized cash-on-cash returns.

- Limited independent verification: narrow audit scope, infrequent third-party valuations, or advisory committees without the resources to challenge valuation methodologies.

Due diligence is non-negotiable. Investors must demand granular disclosures, independent audits, and transparent methodologies. These safeguards, though challenging to implement, offer the clearest defense against the risks lurking beneath the surface.

A Call to Reform

As private credit stretches toward new horizons, its rapid growth demands a parallel commitment to transparency and accountability. The sector’s future hinges on its ability to reconcile ambition with integrity, innovation with responsibility. Investors, fund managers, and regulators alike must confront the uncomfortable truths that shadow this industry.

Regulation must evolve to meet the moment. Enhanced valuation standards, stricter disclosure requirements, and penalties for misrepresentation are essential pillars of reform. Collaborative frameworks, leveraging industry expertise, can foster self-regulation while aligning with broader oversight objectives.

Ethics must guide this transformation. Fund managers face choices that ripple far beyond immediate returns—choices that determine whether their business models empower or exploit. Investors, too, must weigh their pursuit of profit against the systemic risks their decisions may fuel. The collective will to address these challenges will dictate whether private credit emerges as a beacon of innovation or a cautionary tale of ambition unmoored.

Technology may also play a supporting role. A tamper-evident distributed ledger that records acquisition prices and subsequent valuation adjustments could improve auditability and make discretionary mark-ups easier to detect, though it would not by itself determine fair value or constrain the assumptions that feed valuation models.

Artificial intelligence (AI) and machine learning also hold promise for improving valuation accuracy. These technologies can analyze vast datasets to identify patterns and correlations that may be overlooked by human analysts. For example, AI-driven models could incorporate real-time data on macroeconomic indicators, industry trends, and borrower creditworthiness to generate more objective valuations. While these tools are not a panacea, they represent a significant step forward in mitigating the risks associated with subjective assumptions.

However, the adoption of these technologies is not without challenges. Implementing blockchain solutions requires industry-wide collaboration and significant upfront investment, while AI models must be carefully calibrated to avoid perpetuating existing biases. Moreover, the use of technology does not eliminate the need for robust regulatory oversight; rather, it should complement traditional safeguards to create a more transparent and accountable ecosystem.

Recommendations for Strengthening Investor Protections

Given the systemic risks posed by opaque valuation practices, a multi-pronged approach is needed to strengthen investor protections. First, regulators should mandate more detailed disclosures regarding the methodologies used to value Level 3 assets. These disclosures should include sensitivity analyses that illustrate how changes in key assumptions, such as discount rates or recovery projections, impact NAVs. Such transparency would enable investors to better assess the reliability of reported valuations.

Second, the role of independent auditors must be expanded. While annual audits are a standard requirement, their scope often excludes a granular review of valuation methodologies. Regulators should require auditors to conduct periodic, unannounced reviews of Level 3 asset valuations, focusing on the consistency and rationale behind discretionary adjustments. This would provide an additional layer of oversight, deterring opportunistic behavior.

Third, investor education should be prioritized. Many retail investors lack the financial literacy needed to critically evaluate private credit funds, leaving them reliant on marketing materials that often downplay risks. Educational initiatives, supported by both regulators and industry associations, could empower investors to ask more informed questions and demand greater accountability from fund managers.

Conclusion: A Call for Collective Responsibility

The challenges facing private credit markets are not insurmountable, but addressing them requires a collective commitment to transparency and accountability. Fund managers must recognize that their long-term success depends on cultivating trust rather than exploiting opacity. Regulators must strike a balance between fostering innovation and safeguarding investor interests, while investors themselves must approach private credit with a critical eye, resisting the allure of superficially stable returns.

The practice of discretionary upward valuation demonstrates how structural incentives within private credit fund management can lead to distorted reporting. By exploiting flexibility in fair value accounting principles, fund managers may classify transactions as "not orderly" to justify ignoring observable market prices. This allows them to rely on Level 3 inputs, such as proprietary models and recovery assumptions, to inflate asset valuations. While this practice can enhance reported NAVs and accrue performance fees, it creates risks for investors who rely on these valuations for decision making. The systemic implications of such practices have drawn regulatory scrutiny, including calls for enhanced transparency and oversight from the SEC. As SEC Chair Gary Gensler noted when proposing the private fund adviser rules, "Private fund advisers, through the funds they manage, touch so much of our economy. Thus, it’s worth asking whether we can promote more efficiency, competition, and transparency in this field." (SEC, Feb. 9, 2022). Investors must remain vigilant and critically evaluate reported returns, recognizing the potential influence of structural incentives on valuation practices.

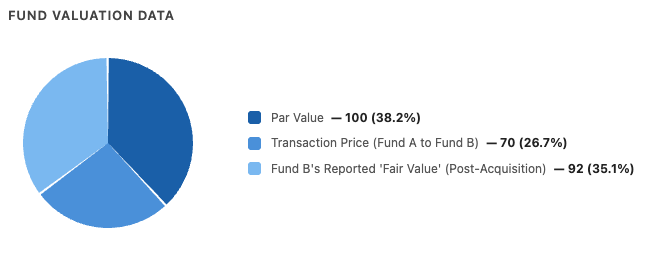

Figure 1. Anatomy of a secondary-market transaction: the valuation gap

This visualization illustrates the core mechanism of discretionary mark-ups. It shows how a distressed asset, acquired at a significant discount (70 cents on the dollar), is subsequently revalued upward by the acquiring fund using Level 3 inputs. This creates a 'valuation gap' between the hard transaction price and the reported Net Asset Value (NAV), artificially inflating perceived performance.

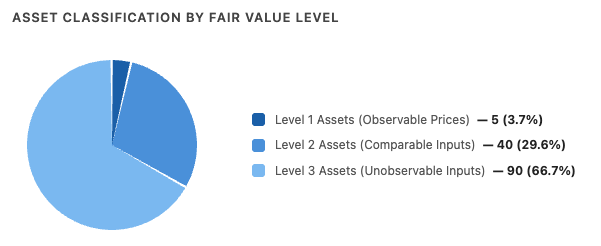

Figure 2. Valuation opacity by asset classification (ASC 820 / IFRS 13)

This chart demonstrates the escalating degree of managerial discretion and valuation opacity as assets move from Level 1 (market-priced) to Level 3 (model-priced). The heavy reliance on Level 3 assets in private credit provides fertile ground for the discretionary mark-ups that obscure true economic performance and mislead investors.

Additionally, a growing body of academic and policy research has examined valuation and return smoothing in private credit markets, generally finding that funds holding more illiquid assets tend to report smoother reported returns than the underlying credit conditions would imply. Financial-press coverage of the sector, including reporting by The Financial Times, has likewise scrutinized how some funds apply subjective valuation adjustments and report smoothed returns. Taken together with the academic literature and the regulatory findings below, this coverage indicates that the concerns described earlier are not merely hypothetical but reflect patterns observers have documented in the industry.

Public filings and regulatory disclosures offer further insight into the valuation methodologies employed by private credit funds. For example, in a Risk Alert issued by the SEC Office of Compliance Inspections and Examinations (SEC OCIE, June 23, 2020), the staff observed that some private fund advisers did not value client assets in accordance with their disclosed valuation processes, in certain cases leading to overcharged management fees and carried interest based on overvalued holdings. These findings underscore the systemic nature of the issue and highlight the need for greater transparency in valuation practices.

Consider, as an illustrative scenario, a fund that disregards observable market prices in favor of internal models that consistently produce higher valuations. Such a pattern—marking a book away from recent transaction evidence without adequate support—would expose a manager to enforcement risk for misleading investors about the fund’s true risk and performance, and it underscores why robust oversight and disclosure matter for market integrity.

The combination of permissive accounting standards and limited regulatory scrutiny creates an environment where opportunistic valuation practices can thrive. While not every fund engages in such behavior, the documented cases and regulatory findings make it clear that the risk is far from theoretical. Investors and regulators alike must remain vigilant to ensure that reported returns accurately reflect underlying economic realities.

Case Studies of Valuation Failures

To further illustrate the challenges of private credit valuation, we turn to the case of the Abraaj Group. Although the Woodford Equity Income Fund is sometimes cited in discussions of fund failures, that episode is best understood as a cautionary example of liquidity mismatch from holding illiquid assets in an open-end, daily-dealing structure rather than a direct private-credit valuation analog (Financial Conduct Authority, 2019); the Abraaj Group is a more relevant example of valuation misrepresentation within a private fund context. Abraaj’s collapse was precipitated by allegations of misappropriated funds and inflated asset valuations; the SEC charged founder Arif Naqvi and Abraaj Investment Management Limited with misappropriating money from a private fund and making misrepresentations to investors (SEC, Litigation Release, Apr. 11, 2019). Investigations revealed that the firm used aggressive accounting techniques to mask liquidity issues and maintain the appearance of steady returns. This case highlights the potential for valuation practices to obscure financial instability, ultimately leading to significant losses for investors.

In a comparable scenario, a fund that overstated its loan portfolio by selectively excluding lower transaction prices from its valuation models would produce materially misleading NAV calculations, harming both investors and broader market confidence. Together, these examples underscore the importance of rigorous valuation standards and greater accountability in private credit markets.

Disclosures

This document contains discussions related to private credit markets, valuation practices, and investment risks, which are financial topics requiring disclosures. The content may be interpreted as commentary on investment strategies, asset valuation methods, and risks associated with private credit funds. Readers should note that this document does not constitute financial or investment advice. Private credit investments involve significant risks, including valuation opacity and reliance on discretionary accounting practices, which may not align with observable market data. Investors are strongly encouraged to consult with a qualified financial advisor or conduct independent research before making any investment decisions. Past performance is not indicative of future results. Additionally, the document references accounting frameworks such as ASC 820 and IFRS 13, which are subject to updates and changes; readers should verify the current applicability of these standards as of the publication date, June 1, 2026.

I'm Joshua, a financial advisor from Reno, Nevada. As someone who co-founded and built a trust company and investment advisory firm from the ground up, I’m passionate about sharing the lessons I've learned on my financial journey of 30+ years to guide and empower clients to secure their financial futures. Using active macroeconomic quantitative and tax avoidance strategies, I mitigate risk and help families achieve lasting financial independence, acting as guardians for future generations. Trust, consistency, and accessibility are at the heart of all my long-lasting client relationships.

Disclosures

This document contains discussions related to private credit markets, valuation practices, and investment risks, which are financial topics requiring disclosures. The content may be interpreted as commentary on investment strategies, asset valuation methods, and risks associated with private credit funds. Readers should note that this document does not constitute financial or investment advice. Private credit investments involve significant risks, including valuation opacity and reliance on discretionary accounting practices, which may not align with observable market data. Investors are strongly encouraged to consult with a qualified financial advisor or conduct independent research before making any investment decisions. Past performance is not indicative of future results. Additionally, the document references accounting frameworks such as ASC 820 and IFRS 13, which are subject to updates and changes; readers should verify the current applicability of these standards as of the publication date, June 1, 2026.

References

Sources are listed alphabetically by author/issuer. Inline citations in the text reference these entries by source and date.

Financial Conduct Authority (FCA). “FCA statement on LF Woodford Equity Income Fund.” 2019. https://www.fca.org.uk/news/statements/fca-statement-woodford-equity-income-fund

International Monetary Fund (IMF). “Fast-Growing $2 Trillion Private Credit Market Warrants Closer Watch.” IMF Blog, Apr. 8, 2024. https://www.imf.org/en/blogs/articles/2024/04/08/fast-growing usd2-trillion-private-credit-market-warrants-closer-watch

Preqin. “2025 Global Report: Private Debt.” Dec. 2024. https://www.preqin.com/insights/global reports/2025-private-debt

U.S. Court of Appeals for the Fifth Circuit. National Association of Private Fund Managers, et al. v. SEC — opinion vacating the SEC private fund adviser rules. June 5, 2024. (Summary: https://www.sidley.com/en/insights/newsupdates/2024/06/us-fifth-circuit-court-of-appeals vacates-private-funds-rules-whats-next)

U.S. Securities and Exchange Commission (SEC). “SEC Enhances the Regulation of Private Fund Advisers.” Press Release 2023-155, Aug. 23, 2023. https://www.sec.gov/newsroom/press releases/2023-155

U.S. Securities and Exchange Commission (SEC), Office of Compliance Inspections and Examinations (OCIE). “Observations from Examinations of Investment Advisers Managing Private Funds” (Risk Alert). June 23, 2020. https://www.sec.gov/files/Private%20Fund%20Risk%20Alert_0.pdf

U.S. Securities and Exchange Commission (SEC). “Arif M. Naqvi and Abraaj Investment Management Limited” (Litigation Release No. 24449). Apr. 11, 2019. https://www.sec.gov/enforcement litigation/litigation-releases/lr-24449

Gensler, Gary (SEC Chair). “Statement on Private Fund Advisers Proposal.” Feb. 9, 2022. https://www.sec.gov/newsroom/speeches-statements/gensler-statement-private-fund-advisers proposal-020922

Financial Times. Ongoing reporting and analysis on private credit valuation, fund performance, and disclosure practices. https://www.ft.com/private-credit

International Monetary Fund (IMF). “Global Financial Stability Report” (chapter on private credit). Apr. 2024. https://www.imf.org/en/publications/gfsr

ASC 820, Fair Value Measurement (Financial Accounting Standards Board) and IFRS 13, Fair Value Measurement (IFRS Foundation) — accounting frameworks governing the fair-value hierarchy referenced throughout this article.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy. All advisory services are offered through Savvy Advisors, Inc. (Savvy Advisors), an investment advisor registered with the Securities and Exchange Commission (SEC).