Tax Diversification: Why Your Roth, 401(k), and Brokerage Accounts Need a Unified Strategy

Retirement tax strategies often focus on individual accounts. However, most high-earning professionals hold wealth across several different accounts. You might have a sizable 401(k), a taxable brokerage account, and a Roth IRA opened years ago. Each serves a purpose, yet they do not work independently. Together, they shape how much you keep after taxes over decades.

Many advisors still look at these accounts one by one. That narrow view misses how decisions in one account impact the others. Contribution choices, investment placement, and withdrawal timing all interact with each other. When you coordinate them under one plan, you gain control over when and how taxes apply. That flexibility can lower lifetime taxes and create more options both before and after retirement.

Key Takeaways

- Holding assets across tax-deferred, tax-free, and taxable accounts gives you more control over income and taxes in retirement.

- Managing accounts together allows you to choose which “bucket” to draw from each year to manage tax brackets.

- Roth conversions can reduce future RMDs and create tax-free income later in life.

- Asset location reduces annual taxes and keeps more of your returns working for you.

- Withdrawal timing often has a larger tax impact than investment selection alone.

Understanding the Three Tax Treatments (And Why It Matters)

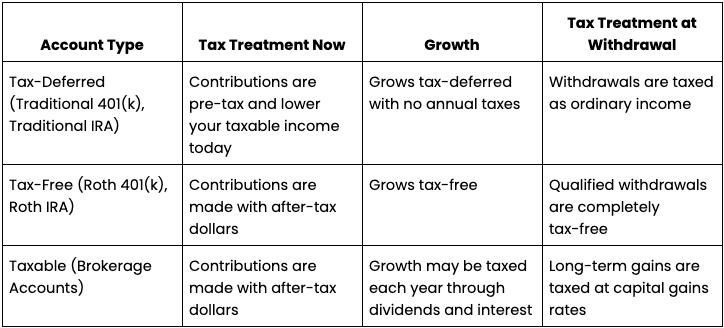

A retirement plan works best when it includes accounts taxed in different ways. Tax-deferred, tax-free, and taxable accounts each follow their own rules for contributions, growth, and withdrawals. Knowing how these tax treatments work gives you more control over income and taxes later in life.

Tax-Deferred Accounts (Traditional 401(k), Traditional IRA)

Tax-deferred accounts let you contribute pre-tax dollars, which lowers your taxable income in the year you contribute. Your investments grow without annual taxes, but withdrawals count as ordinary income. For high earners, that income could face federal rates as high as 37%, with state taxes adding more.

These accounts also come with Required Minimum Distributions (RMDs). Once you reach age 73, or age 75 if you were born in 1960 or later, you need to start taking annual RMDs from traditional retirement accounts. These forced withdrawals reduce control over timing and can raise your tax bill in retirement.

Tax-Free Accounts (Roth 401(k), Roth IRA)

Roth accounts flip the tax equation. You contribute after-tax dollars, so there is no upfront deduction. In exchange, qualified withdrawals in retirement are entirely tax-free. That includes both contributions and investment growth.

Roth IRAs stand out because they have no RMDs during the original owner’s lifetime. This allows assets to remain invested for as long as you choose. Recent legislation also removed RMDs for Roth 401(k)s in many cases. When comparing Roth vs. 401(k) options, Roth accounts add long-term flexibility that tax-deferred accounts can’t match.

Taxable Brokerage Accounts

Taxable brokerage accounts offer complete access to your money at any time. There are no contribution limits and no age rules for withdrawal. Dividends and interest face annual taxes, while long-term capital gains receive lower rates. For 2026, a single filer pays 0% on long-term capital gains if taxable income stays at or below $49,450, 15% up to $545,000, and 20% above that level.

These accounts also allow tax-loss harvesting. Realized losses can offset capital gains and up to $3,000 of ordinary income each year, with unused losses carried forward. In the 401(k) vs. brokerage account discussion, taxable accounts provide flexibility that retirement plans do not.

The Problem with Traditional Retirement Advice

Many retirement plans focus on lowering taxes today without looking ahead. This short-term view often leaves high-income professionals with large tax bills later. By ignoring how accounts interact over time, traditional advice can limit flexibility and raise lifetime taxes.

Why “Max Out Your 401(k)” Can Create a Tax Bomb

Maxing out a traditional 401(k) sounds appealing during high-earning years. The immediate tax deduction seems valuable, but the long-term effect can actually work against you. Over time, large balances build in tax-deferred accounts. When RMDs begin, those balances turn into mandatory income.

These forced withdrawals can push you into higher tax brackets than you had while working. They also raise modified adjusted gross income, which impacts other areas of retirement. Higher income can increase the portion of Social Security benefits subject to tax. It can also raise Medicare premiums. For 2026, IRMAA (Income-Related Monthly Adjustment Amount) thresholds start at $109,000 for single filers and $218,000 for married couples, with Part B and Part D premiums rising sharply above those levels.

The Risks of Tax Homogeneity and Non-Holistic Planning

A retirement portfolio built almost entirely in tax-deferred accounts leaves little room to manage income later. You need to take withdrawals on the IRS schedule, regardless of market conditions or personal needs.

Many advisors manage each account on its own. That approach overlooks how withdrawals from one account impact taxes on another. Without a coordinated plan, you lose the ability to choose which account to draw from each year to control your tax bracket. Over a long retirement, that lack of flexibility can add up to significantly higher lifetime taxes.

Building Your Tax-Diversification Framework

A tax-diversification plan looks at all your accounts together rather than in isolation. It sets clear priorities for contributions, conversions, and long-term balance targets based on income, age, and retirement timing. This framework gives you more options as tax rules and income levels change.

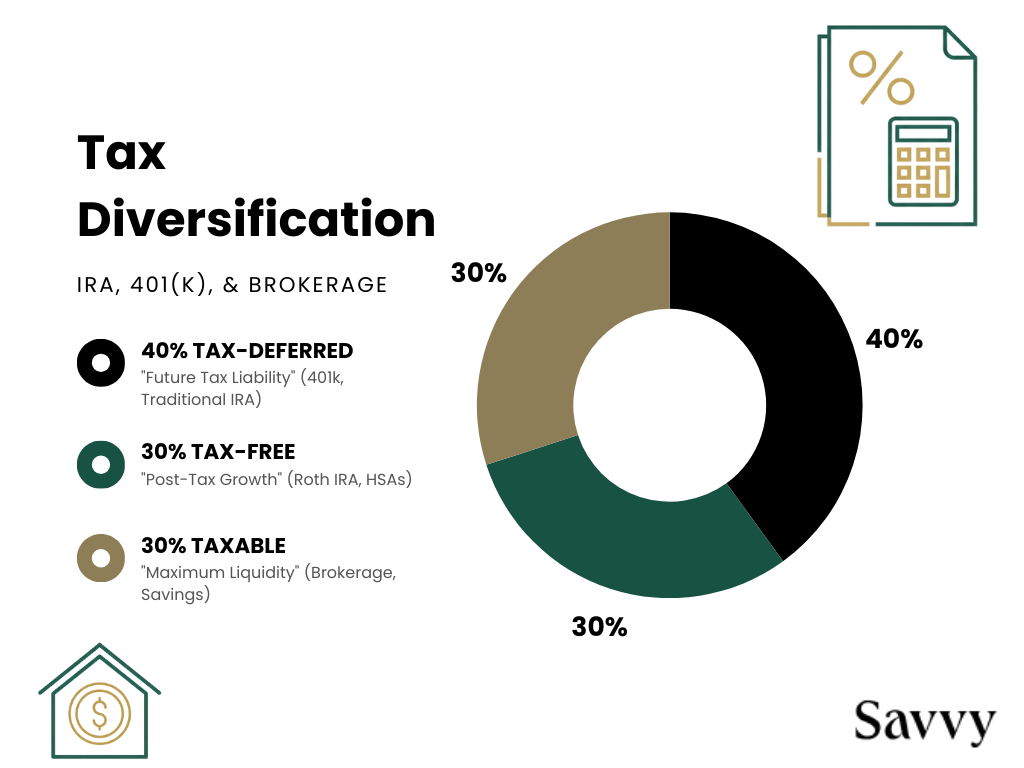

The Optimal Asset Mix and Prioritization

Many high earners aim for a mix that spreads assets across tax treatments. A typical target is roughly 40% in tax-deferred accounts, 30% in Roth accounts, and 30% in taxable brokerage assets. This balance creates flexibility without leaning too heavily on one tax outcome.

During high-income years, it often makes sense to continue funding a traditional 401(k) to reduce current taxes while also using Backdoor Roth IRAs to build tax-free assets. If your plan allows it, after-tax 401(k) contributions paired with in-plan conversions can support a Mega Backdoor Roth strategy. After covering retirement plans, directing additional savings to a taxable brokerage account adds liquidity and future tax planning options.

Strategic Roth Conversions for High Earners

Roth conversions play a vital role in a strong Roth conversion strategy. Converting assets from traditional accounts to Roth accounts triggers taxes today, but it removes future taxes on growth and withdrawals.

Lower-income years create ideal windows for conversions. Early retirement, career breaks, or business transitions often come with reduced taxable income. Conversions during these periods can fill lower tax brackets without pushing income too high. Market downturns also lower the tax cost of conversions by reducing account values. Over time, multi-year conversions shrink tax-deferred balances and reduce future RMDs, which can also limit Medicare premium increases later in life.

Asset Location: What Goes Where?

Asset location focuses on placing investments in the account type where they face the least ongoing tax impact. The goal is to reduce annual taxes on investment income while allowing more of your returns to compound over time.

The Asset Location Hierarchy

Taxable brokerage accounts work best for tax-efficient investments. Broad market index ETFs (Exchange-Traded Fund), low-turnover funds, and municipal bonds tend to generate lower taxable income each year.

Tax-deferred accounts, like traditional 401(k) and IRAs, fit better with tax-inefficient assets. REITs (Real Estate Investment Trusts), taxable bonds, and actively managed funds often generate income taxed at ordinary rates, which stays sheltered inside these accounts.

Roth accounts should hold assets with the highest expected growth. Any gains in these accounts avoid future taxes entirely. In fact, following an asset location approach can raise annual after-tax returns by about 0.14 to 0.41 percentage points for investors in mid to high tax brackets. For a retired couple with a $2 million portfolio, that difference can equal roughly $2,800 to $8,200 per year in reduced tax drag.

Withdrawal Strategy: The Retirement Payoff

Tax diversification shows its actual value once withdrawals begin. A coordinated plan gives you control over where income comes from each year, which can lower total taxes across your retirement.

Strategic vs. Traditional Sequencing

Many retirees follow a simple rule: withdraw from taxable accounts first, then tax-deferred accounts, and save Roth assets for last. While common, this approach can lead to higher taxes later. Large tax-deferred balances remain untouched for years and continue to grow, which increases future RMDs.

A strategic approach begins drawing from tax-deferred accounts earlier, often before Social Security starts. These withdrawals can fill lower tax brackets while income remains modest. Taxable accounts and Roth assets then play a role based on market conditions and tax brackets. Roth accounts often stay intact for late-retirement needs or for heirs who can receive the funds tax-free.

The Math of Lifetime Tax Savings

Small changes in withdrawal timing can create significant differences over decades. On a $5 million portfolio, coordinating withdrawals across account types can reduce taxes by hundreds of thousands over a 30-year retirement.

Those tax savings do not disappear. When reinvested, they add meaningful growth to the portfolio. Ongoing adjustments during market swings, health changes, or shifts in income keep the plan matched with your actual life rather than a fixed formula.

Turning Tax Diversification into Action

Tax diversification works best when it guides actual decisions rather than just account balances. A unified approach connects how you save, invest, convert, and withdraw across every stage of your financial life. When all accounts follow one plan, taxes become a variable you can manage rather than react to.

Next Steps

- Review your current account balances by tax type to see where concentration exists.

- Estimate future RMDs to understand potential income and tax exposure.

- Identify years with lower income where Roth conversions might fit.

- Check whether your investments sit in the most tax-appropriate accounts.

- Revisit your withdrawal plan before retirement begins, not after.

Ready to build a tax-efficient roadmap for your wealth?

Contact a Savvy Advisor Today!

FAQs

Should I stop contributing to my 401(k) to build up my Roth?

Not usually. Many high earners benefit from doing both. A traditional 401(k) can lower taxes today, while Roth contributions or conversions build tax-free income later. The right mix depends on income, cash flow, and future tax exposure.

What if tax rates go down in the future—won't Roth conversions backfire?

Roth conversions are less about predicting tax law and more about managing risk. Even if rates fall, tax-free income can reduce RMDs, Medicare premiums, and taxable Social Security, which still creates long-term value.

Can I convert my 401(k) to a Roth while still working?

Sometimes. Many plans allow in-plan Roth conversions or after-tax contributions converted to Roth. Others require you to wait until separation. Plan rules matter, so checking your employer’s options is an essential first step.

How do I determine the right conversion amount each year?

The goal is to convert enough to fill lower tax brackets without triggering higher rates or surcharges. This usually means modeling current income, deductions, and future RMDs to find a repeatable annual conversion range.

Will Roth conversions affect my Medicare premiums?

Yes, they can. Roth conversions increase taxable income, which may trigger Medicare IRMAA surcharges. Strategic planning spreads conversions over multiple years to manage premiums while still reducing long-term tax exposure.

Works Cited

- Required Minimum Distributions: What's New in 2026

- Roth IRA Conversions: What High Earners Need to Know

- Taking your required minimum distribution (RMD)

- Find the best Medicare plan for you by working with a licensed agency.

- 2025 2026 2027 Medicare IRMAA Premium MAGI Brackets

Hi there! I’m Jacob LaRue, CFP®, a Wealth Manager from Minneapolis, MN, passionate about providing tailored retirement planning services to MedTech employees and their families. As part of the Perspective 6 Wealth Advisors, I assist in comprehensive financial plan development, investment management, and running client review meetings. With focus areas across retirement income planning, Social Security analysis, and retirement distribution analysis, I’m dedicated to helping clients achieve financial freedom in retirement.

Contact a Savvy advisor

Contact a Savvy advisor