I have a love/hate (mostly hate) relationship with my freezer. The ice machine has been broken since Covid. I’ve hired countless people to look at it, diagnose the problem, and present a solution - with zero luck. I’m too stubborn and frugal to buy a whole new appliance just for ice. I’m happy to report that my parents bought me a countertop ice maker for Christmas, because that’s just the kind of parents they are. My kids are obsessed with ice, so I must keep it running 24/7. Recently, they went on a vacation with their aunt, so it was just me, my two rescue dogs that are literally the worst, and the ice maker. Despite having zero desire to pay attention to it while the kids were gone, my silence and peace were disrupted by the hums, clanks, and dropped cubes of the ice machine.

It didn’t dawn on me until recently that the ice maker was working overtime, but for what? I wasn’t emptying out the ice tray. I hadn’t refilled it with water. I wasn’t consuming the frozen water cubes it was spitting out. And yet, the ice maker continued to produce ice. It sounds quite industrious, but it’s just melting yesterday’s output and freezing it again. Over and over again. Rinse and repeat. No new water. No net new value. Just a Christmas gift from my parents that seemed hell bent on recycling whatever ice had melted earlier in the day. What does any of this have to do with money or finance? Glad you asked, even if you technically didn’t.

My over-achieving ice maker is the perfect metaphor for the narrow AI-driven market performance.

When 5 mega-cap companies dominate inflows, ETFs, index funds, options flows, and AI hype, you end up with the same dynamic. Capital rotates between the same names. It feels like productive growth, when it might just be circulation. The machine makes noise, just like the markets. GDP ticks up. However, if productivity gains are speculative, infrastructure spending is front-loaded, and earnings expansion is concentrated in a tiny handful of companies, you end up with something that looks like expansion on the surface – without broad participation. Introducing… your recycled ice cube economy.

Think of real growth like new water entering the system (i.e. new industries, expansion of wages, and broad earnings participation). Durable output is being produced. On the other hand, think of recycled growth. While there very well may be multiple expansion and capital rotation, it’s all happening inside the same ecosystem.

Ice. Melt. Ice again.

Here’s where the danger comes in: As long as demand exists, the machine keeps running as designed. But if inflows start to slow or sentiment (read: vibes) shifts, you just might realize there was never much incremental water to begin with. Just increasingly fragile cubes stacked on top of each other. That’s when volatility hits. When the same handful of names account for a disproportionate share of returns while the rest of the market drifts, it’s worth looking into whether the water is fresh or are we all just cheering on a loud and annoying ice maker. The metaphor illustrates the AI infrastructure loop almost perfectly.

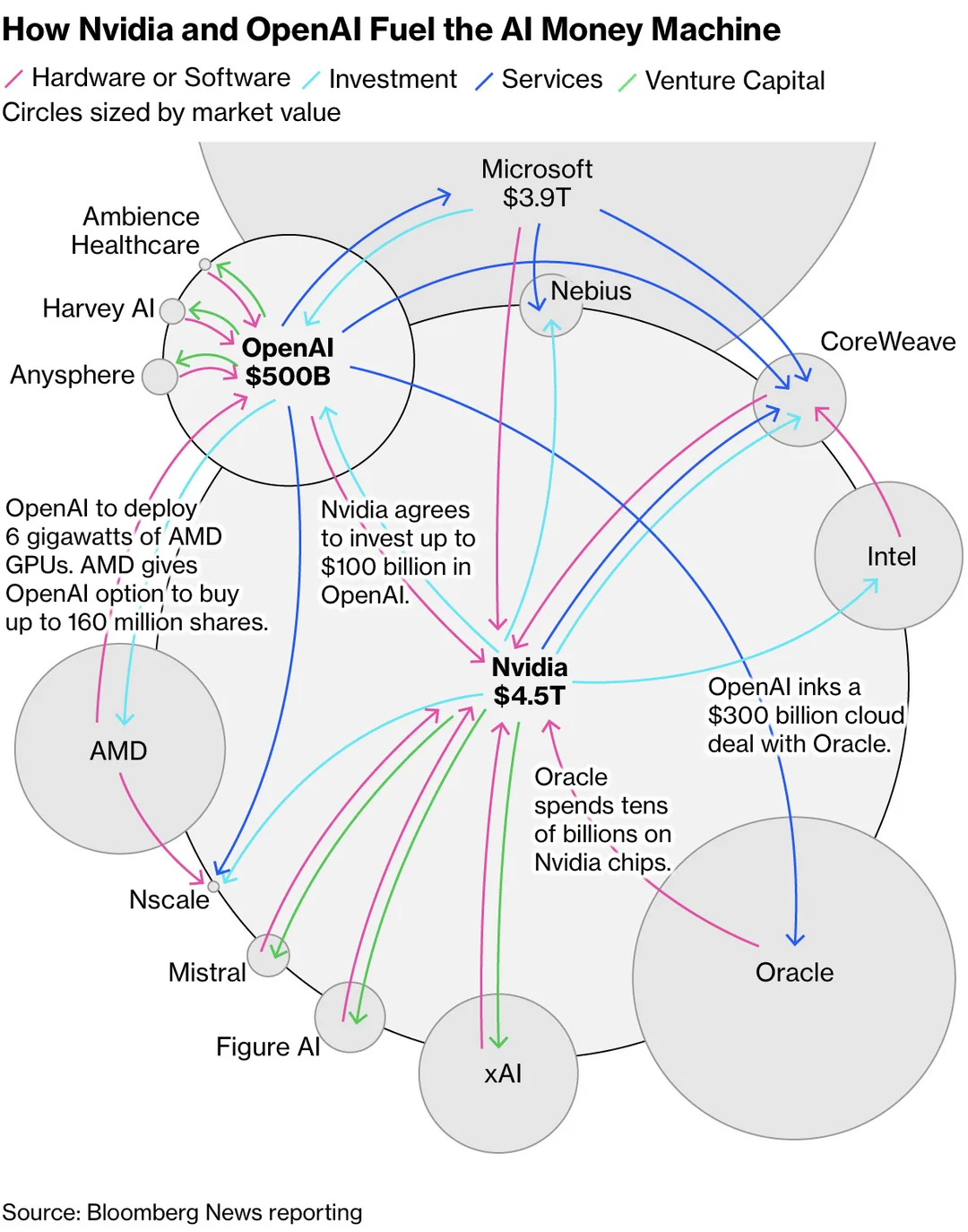

Let’s look at this loop in the real world. Companies building AI models need TONS of computer power, so they buy GPUs from Nvidia worth tens of billions. According to Reuters, Oracle planned to buy ~$40B of Nvidia chips which would go into giant AI data centers supporting AI workloads (Enter: OpenAI). Then, there are the cloud companies who host the infrastructure. The chips end up in data centers that are run by cloud providers (Enter: Amazon Web Services, Microsoft Azure, and Oracle Cloud). These companies rent compute power to the AI companies that are currently training AI models. AI companies spend LOTS of money (Enter: AI labs like OpenAI and Anthropic) on compute capacity.

Here’s the kicker: Many of those same tech giants are investors in the AI labs. For example, Microsoft invests heavily in OpenAI and then books cloud revenue when OpenAI runs models on Microsoft Azure. Amazon invests in Anthropic and then hosts its models on Amazon Web Services. Nvidia invests in AI startups that buy Nvidia chips. This creates a structure where companies are investors, infrastructure providers, and sometimes even customers - all at once. Thus why my brain couldn’t help but make the connection between what economists call circular financing and my ice machine.

It’s giving snake eating its own tail.

The system looks/feels like new output because the ice cubes keep dropping. There is motion. Things are happening. Win for productivity! But sometimes it’s just the same water freezing again. Or is it? There are three major debates happening on Wall Street right now. The first has to do with concentration risk. The lion’s share of AI market cap growth is coming from 5 companies: Nvidia, Microsoft, Amazon, Alphabet (Google), and Meta (Facebook). Most of the returns come from the same key players, which makes GDP and market growth look broader than it is. The second debate involves infrastructure and demand. The system is currently spending hundreds of billions building AI data centers, betting on the expectation that growth will come later. If it does, it’s like a reservoir filling with new water. If it doesn’t, we might just have a bunch of very expensive ice makers running on recycled, melted water. Lastly, there’s a debate comparing financial engineering with actual productivity. If revenue mostly comes from gigantic tech companies buying services from each other, the economy appears to be expanding even if there’s no sign of productivity gains yet. Enter: The Phantom-Growth Concern.

Here’s the good news: My ice maker metaphor isn’t a conclusion, but more of a warning. Sometimes early tech revolutions really do look circular at first (i.e. railroads funding railroads and internet companies hosting internet companies). Eventually, the tech bleeds over into the actual economy. As of the writing of this blog, there are so many unknowns. Is AI still filling the reservoir and making new ice or is it just freezing the same old recycled water?

Below is a diagram that went viral recently. While I do appreciate a good visual, it exaggerates things a bit and implies that revenue is fake or purely circular. It makes the loop look tighter than it actually is. Money flows through many layers and it’s not a neat circle in reality. It’s much messier than the diagram illustrates. For example, even if Microsoft invests in OpenAI and OpenAI spends money on Azure, that doesn’t automatically mean the revenue is fake. Why? Because OpenAI also has revenue streams from ChatGPT subscriptions, API customers, and enterprise software deals. Money from outside the loop does enter the system. The diagram makes it look like there’s no new water, which isn’t completely true. What’s more, AI spending isn’t just tech companies paying each other. There are other industries buying AI services (pharma, finance, cybersecurity, logistics, software development to name a few). This translates into new demand entering the system, not just the same stacks of tech dollars being recycled on repeat. Despite its shortcomings, the visual succeeds in showing how tightly connected the AI ecosystem has become. It’s not proof that the whole thing is fake, though.

Right now, a huge portion of market gains comes from the same 5 companies. Regardless of how you feel about the ice maker, the metaphor, the AI bubble, or the diagram, there’s one major risk that everyone is talking about:

Concentration.

Enter: The Case for Diversification. A woman named Sally was recently referred to me for asset management and financial planning. She swore up and down that she was diversified because she owns an S&P 500 index fund, a NASDAQ fund, a tech ETF, and an AI ETF. She essentially owns Nvidia, Microsoft, Amazon, Meta, and Alphabet four different ways. I gently explained to her that she wasn’t actually diversified. Quite the opposite… Her investment portfolio was extremely concentrated, just wearing different hats. I’m thrilled to report that Sally became a client and is thrilled to have a diversified portfolio that owns various parts of the market that aren’t driven by the same story (i.e. mid and small-cap stocks, value-oriented sectors, international markets). Spreading the risk across various asset classes enables us to withstand the different outcomes if the AI cycle slows or the bubble bursts. Sally went from chasing headlines and reacting emotionally to click-bait blog titles and doomsday emails forwarded to her by well-meaning friends to remaining calm and collected during times of intense volatility. Instead of asking “Is AI a bubble that’s going to burst and destroy everything I’ve worked so hard for, thus leaving me destitute and hopeless?!) we are using a different approach: “What happens to my portfolio if AI expectations cool off for a few years?” My answer: Not much, because we believe the portfolio is well built.

If you’re worried the market might be recycling the same water like my ice maker, the answer isn’t to stop investing all together and pull everything out of the market. The solution lies in making sure your portfolio has access to other reservoirs.

.webp)

.webp)

Lindsey is a Private Wealth Advisor who believes peace of mind is not found in projections but built through genuine partnership. She helps clients transform financial complexity into clarity by creating personalized roadmaps that deliver real, sustainable freedom. Lindsey is especially passionate about guiding dynamic women as they reclaim their financial power or step into it confidently for the first time. Her approach seamlessly blends sharp analytical thinking with deep intuition: a neurodivergent, creative mind that spots patterns others miss, paired with an obsessive attention to detail that ensures nothing falls through the cracks.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Inc. is a technology company. Savvy Advisors, Inc. is an SEC registered investment advisor. For purposes of this article, Savvy Wealth and Savvy Advisors together are referred to as “Savvy”. All advisory services are offered through Savvy Advisors, while technology is offered through Savvy Wealth. The views and opinions expressed herein are those of the speakers and authors, and do not necessarily reflect the views or positions of Savvy Advisors.

Any references to publicly traded companies within this article are provided solely for informational and illustrative purposes, based on their relevance to the subject matter discussed. Such references should not be construed as a recommendation, endorsement, or solicitation to buy or sell any securities. The inclusion of any company does not reflect any opinion regarding its investment merits, and readers should not rely on this content as investment advice.