How Does Compound Interest Work? A Beginner’s Guide

How does compound interest work? At its core, it’s the process of earning interest on both your original balance and the interest that builds over time. This simple idea has been called the "eighth wonder of the world" due to its ability to transform modest savings into substantial growth. Below, we’ll break down how compound interest works and how you can use it to build long-term financial security.

Key Takeaways

- Compound interest is interest on both your original balance and past earnings.

- Time, frequency, and rate of return are the main drivers of growth.

- Retirement accounts maximize compounding by sheltering growth from taxes.

- Debit can also compound, working against you if balances are left unpaid.

- Small decisions, like reinvesting earnings and keeping fees low, add up over decades.

What is Compound Interest?

Compound interest is interest that’s calculated on both your original balance (the principal) and the interest that has already been added in past periods. This creates a snowball effect, where your money grows faster the longer it’s been invested. Instead of earning interest only on what you put in, you’re also earning on the interest that has been piling up. That’s why compounding interest is often described as your money working for you.

Simple vs. Compound Interest: The Fundamental Difference

To understand the value of compounding, it is helpful to compare it with simple interest. Simple interest is calculated only on the original balance. The formula is straightforward:

Simple Interest = Principal x Rate x Time

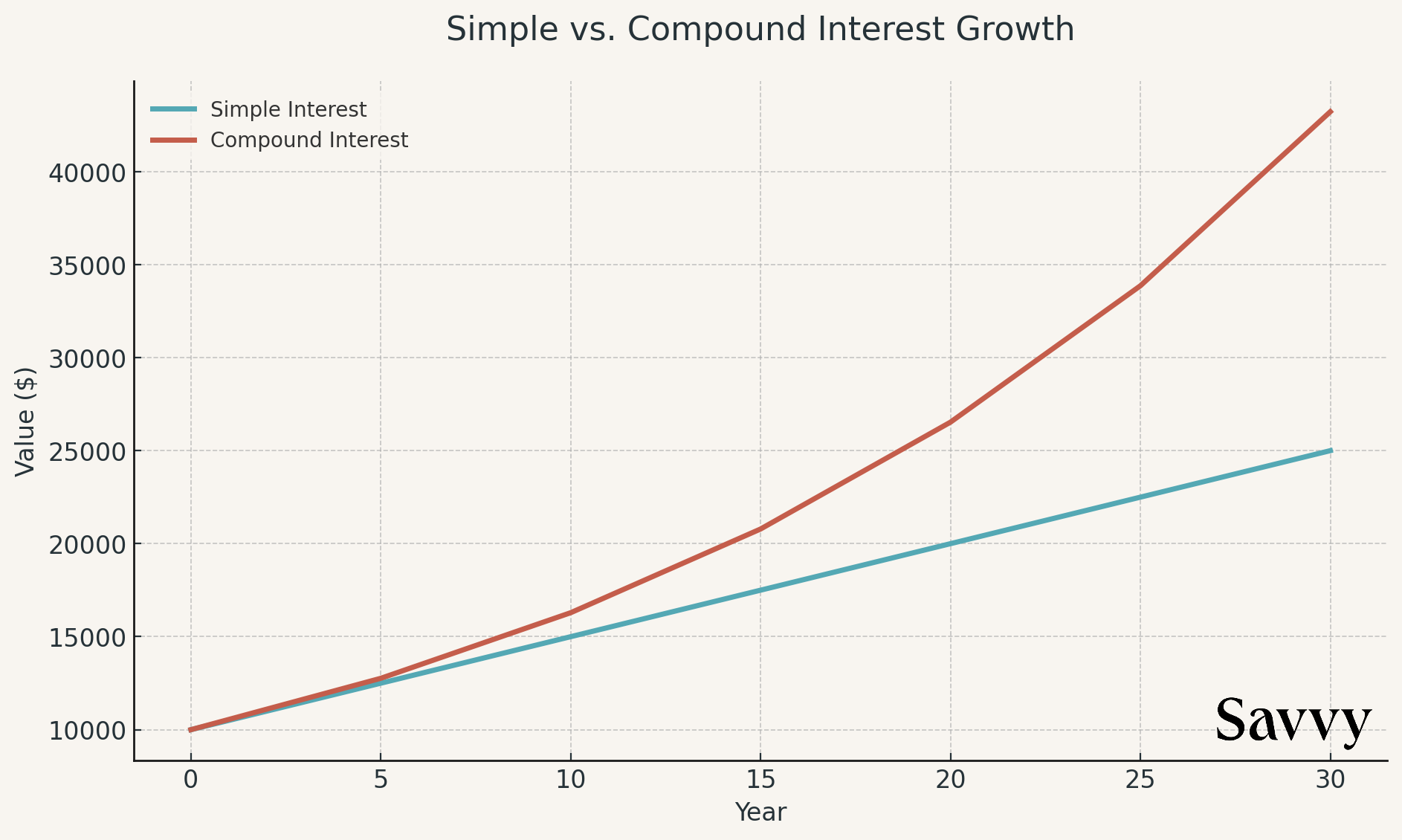

For example, if you invest $10,000 at 5% simple interest for 10 years, you’ll earn exactly $5,000. That leaves you with a total of $15,000

Now look at compound interest. The same $10,000 invested at 5% for 10 years grows to about $16,289. That’s $1,289 more than the simple interest option, without any extra effort from you. Over time, this difference becomes even more pronounced, demonstrating why compound interest examples are so powerful.

The Mechanics: Understanding the Compound Interest Formula

At first glance, the math behind compound interest may seem intimidating. However, it’s actually straightforward once you break it down. The standard formula is:

A = P(1 + r/n)^(nt)

Here’s what each part means:

- A = the final amount

- P = the principal, or your starting balance

- r = the annual interest rate (written as a decimal)

- n = how many times the interest compounds per year

- t = the number of years

For investments that compound once a year, the formula simplifies to:

A = P(1 + r)^t

This version is one of the most often used in basic compound interest examples.

A Step-by-Step Calculation Example

Let’s see the formula in action. Imagine you invest $5,000 at 6% annually for 8 years.

Step 1: Plug the numbers into the formula.

A = 5000(1 + 0.06)^8

Step 2: Do the math.

A = 5000(1.5938) ≈ $7,969

Step 3: Find the total interest earned.

$7,969 - $5,000 = $2,969

In this case, your $5,000 investment grows to nearly $8,000, with almost $3,000 of that growth coming purely from compounding interest. It demonstrates how even a moderate rate over time can make your money work harder for you.

The 3 Key Factors That Supercharge Your Returns

Compound interest is powerful, but three factors ultimately determine how much your money grows: time, how often interest is added, and the rate of return. Each one makes a sizable impact, and together they create the momentum that drives long-term growth.

The Power of Time: Why Starting Early is Non-Negotiable

Time is the most essential ingredient in compounding. The earlier you start, the more years your money has to multiply.

For example, imagine three people who each invest $5,000 every year until retirement: one starts at 25, another at 35, and the third at 45. The person who begins at 25 contributes only $50,000 more than the one who starts at 35, but by retirement, they have over $600,000 more. That’s the snowball effect in action.

Related Article: Getting Started with Retirement Planning

The Impact of Compounding Frequency

The frequency at which your interest is calculated and added, known as compounding frequency, is also crucial. Annual compounding is common, but some accounts calculate interest on a semi-annual, quarterly, monthly, or even daily basis.

The more often interest is compounded, the quicker your balance grows. For example, a $10,000 investment compounded annually at 5% will grow more slowly than one compounded daily at the same rate. In practice, the difference between monthly and daily compounding is generally slight; however, over many years, it still adds up.

How Different Interest Rates Affect Your Growth

The third factor is the rate of return. Even minor differences in interest rates can have huge effects on the outcome.

Take a $10,000 investment over 20 years:

- At 3% = about $18,061

- At 5% = about $26,533

- At 7% = about $38,697

- At 10% = about $67,275

Notice how a 7% return doesn't simply double the outcome compared to a 3% return. This exponential growth is why high returns, even by a few percentage points, make such a significant impact over decades.

In fact, the S&P 500’s historical average yearly return is 10.463% over the last 100 years when dividends are reinvested. Over the past 10 years ending May 2025, the average return has been 12.566% annually, showing the long-term power of compounding in equity investments.

Compound Interest in Action: Real-World Applications

Compound interest is found in everyday financial tools and long-term investing. From savings accounts to retirement plans, this principle is what allows balances to grow steadily over time. Real-world examples make it clear how powerful compounding is for building wealth.

According to recent data, average 401(k) account balances grow significantly with time. Participants under 25 had an average savings of $7,351, while those age 65+ averaged $272,588. This dramatic difference shows how compound growth accelerates wealth over decades.

Savings Accounts and Certificates of Deposit (CDs)

Most bank savings accounts and CDs use compound interest. In many cases, interest is calculated daily and paid out monthly. This makes them predictable and safe, mainly because savings accounts and CDs at FDIC (Federal Deposit Insurance Corporation)-insured banks protect your balance up to legal limits.

The main drawback is that the rates are typically lower than long-term inflation. These accounts are built for short-term goals or emergency funds, but they might not keep up with the rising cost of living.

As of October 2025, high-yield savings accounts offer up to 5.00% APY (Annual Percentage Yield), compared to the national average of just 0.40%.

Investment Accounts

Investment accounts, such as mutual funds, ETFs (Exchange-Traded Funds), or stocks, take compounding to another level. Here, returns grow through share price increases and also through reinvested dividends and capital gains.

When dividends are reinvested, they buy additional shares. Those new shares then generate their own returns, creating a self-reinforcing cycle. Over long periods, this cycle makes a substantial difference in total growth.

Related Article: How to Diversify Your Investment Portfolio

Retirement Accounts: The Ultimate Compounding Vehicle

Retirement accounts such as 401(k)s and IRAs (Individual Retirement Account) are designed to maximize the effect of compound interest. Their tax advantages, whether tax-deferred (traditional accounts) or tax-free growth (Roth accounts), allow your money to compound without being reduced by yearly taxes.

That means more of your money stays invested and keeps working over decades. With regular contributions and long time horizons, retirement accounts turn steady savings into significant wealth by the time you stop working.

Related Article: Individual Retirement Accounts (IRAs): What They Are and How to Open One

Navigating Your Financial Journey: Tools and Traps

Compound interest is a powerful way to grow wealth. However, it also comes with shortcuts and pitfalls. Understanding both sides gives you the tools to take advantage of compounding interest while avoiding situations where it could work against you.

The Rule of 72: A Quick Way to Estimate Growth

The Rule of 72 is a handy mental shortcut to estimate how long it will take for your money to double. The formula is simple:

Years to Double ≈ 72 ÷ Interest Rate

For example, if you earn 9% annual return, your money will double in about 8 years (72 ÷ 9 = 8). While not exact, it’s surprisingly accurate in most scenarios.

Research shows that the Rule of 72 is most accurate for interest rates between 5% and 12% with a margin of error of about 2%. It’s particularly precise in the 8-10% range.

The Other Side of the Coin: When Compound Interest Works Against You

Compounding isn’t always your friend. Debt can quickly become a burden. Credit cards are a prime example because they charge interest on the original balance but also on unpaid interest from previous months.

That means carrying a large balance at a high interest rate leads to thousands of dollars in charges and takes decades to repay if you only make minimum payments. This is where compounding interest shows its “dark side.” Instead of growing your savings, it grows what you owe.

The Silent Killers of Growth: Taxes and Inflation

Even when your investments are compounding, two forces quietly slow your progress: taxes and inflation:

- Taxes: In taxable accounts, interest and gains are reduced each year by taxes. This reduces the balance that keeps compounding, often called “tax drag.”

- Inflation: The gradual rise in prices over time, which erodes purchasing power. If your investment return is below the inflation rate, your money is actually losing value.

That’s why long-term investors often use tax-advantaged accounts and aim for returns above inflation to keep their compounding working effectively.

Related Article: IRA vs. 401(k): A Comparison of Retirement Savings Vehicles

5 Strategies to Maximize the Power of Compound Interest

If you want to make the most of compound interest, there are a few key moves that give your money the best opportunity to grow. These strategies are easy to understand and have a significant impact over time.

- Start as Early as Possible: Time is your most significant advantage. Even small contributions made early can grow into large sums over decades.

- Contribute Regularly and Consistently: Making steady contributions, either monthly or yearly, keeps the compounding effect going and builds momentum.

- Continually Reinvest Your Earnings: Dividends, interest, or capital gains should stay invested whenever possible. Reinvesting keeps your money compounding instead of sitting idle.

- Seek Higher Returns (Within Your Risk Tolerance): Even small increases in your rate of return can mean thousands more over the long run. The key is to balance growth potential with the level of risk you’re comfortable with.

- Use Tax-Advantaged Accounts to Your Benefit: Accounts like IRAs and 401(k)s let your investments grow without being reduced by annual taxes. Over time, this makes a significant impact on your final balance.

Pitfalls That Can Weaken Your Growth

Even with the power of compound interest on your side, some choices slow down or even undo your progress. Knowing what to avoid keeps your savings on track.

- Waiting Too Long To Start: The most significant missed opportunity is time. Delaying contributions means fewer years for your money to compound.

- Cashing Out Too Early: Withdrawing money before it has time to grow interrupts the compounding process, often reducing your long-term results by thousands of dollars.

- Overlooking Fees: Even a small annual fee, like 1%, might seem harmless. However, over decades, it eats away a large portion of your returns.

- Ignoring Inflation: If your earnings don’t outpace inflation, you lose purchasing power. That’s why aiming for growth above the inflation rate is essential.

Take Control of Your Financial Future Today

Compound interest has the potential to transform steady savings into meaningful long-term wealth. By starting early, contributing regularly, and avoiding any pitfalls, you can apply this principle to your goals.

Next Steps:

- Review your current savings and investment accounts.

- Begin to increase regular contributions, regardless of the amount.

- Reinvest dividends and interest instead of cashing them out.

- Explore tax-advantaged options like IRAs and 401(k)s.

- Set long-term goals and revisit your progress each year.

FAQ

How often is interest compounded in a 401(k)?

401(k)s don’t use fixed compounding schedules. Growth comes from reinvested earnings like dividends and capital gains, which compound as long as your money stays invested.

Can I live off the interest on a million dollars?

If invested conservatively (1–2%), it might generate $10,000–$20,000 a year. With a 4–5% return, it could provide $40,000–$50,000 annually. Your lifestyle, taxes, and investment strategy all factor in.

How much money do I need to invest to make $3,000 a month?

To generate $36,000 per year:

- At 3% return: ~$1.2M

- At 5%: ~$720K

- At 7%: ~$515K

Higher returns mean less capital is needed but more risk.

What will $1,000 be worth in 20 years?

It depends on the return:

- 3%: ~$1,806

- 5%: ~$2,653

- 7%: ~$3,870

- 10%: ~$6,727

Time + return = exponential growth.

How much is $1,000 worth at the end of 2 years if the interest rate of 6% is compounded daily?

About $1,127.49. Daily compounding slightly boosts returns over short periods, especially at higher rates.

Hi there! 👋🏼 I’m Nick, with 20+ years in wealth management, I like to blend sophisticated strategies with personalized client experiences. I specialize in financial planning for all life stages, from early savings to retirement distribution. I also bring expertise in high-net-worth services, equity management, and municipal bonds.

Works Cited

- Historical Average Stock Market Returns for S&P 500 (5-Year to 150-Year Averages)

- Savings For Retirement

- You Can Get Up to 5.00% APY on the Best High-Yield Savings Accounts Today, Oct. 1, 2025

- How Long Does It Take For Your Money or Debt to Double? Explaining the Rule of 72 to Students

.webp)

.webp)