Data Shows A Weakening Economy But Markets and Fed Unresponsive

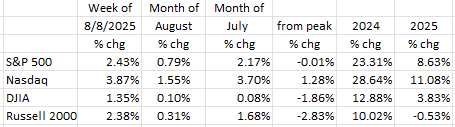

Despite a clearly weakening economy, the equity markets continued on an upward path. For the week ended Friday, August 8th, the Nasdaq advanced nearly 4%, more than compensating for the prior week’s -2.2% loss, and now shows an impressive +11% gain year to date. The S&P 500 advanced +2.4% and the DJIA +1.4%. Even the small-cap Russell 2000 participated (+2.5%).1 All in all, a good week for equities.

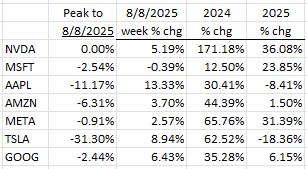

For the magnificent 7, Nvidia set a new all-time high on Friday, and Meta is close. Apple (+13%) and Tesla (+9%) also advanced sharply for the week.

The Consumer

Equity markets seem divorced from economic reality. The economy continues to sputter as consumer spending has slowed in 2025. In June, spending fell versus May on big-ticket items like Furniture (-0.3%), Appliances (-0.6%), Entertainment (Casinos -2.1%), and Travel (Air travel -1.1% and negative in five of the last six months as was spending on Hotels/Motels).2 It is always a telling sign when high-end consumers, i.e., the wealthy, cut back. In June, their spending on Jewelry/Watches fell (-0.6%).2 Doesn’t sound like much, but the norm is a slow and steady increase. So, an actual cutback is significant.

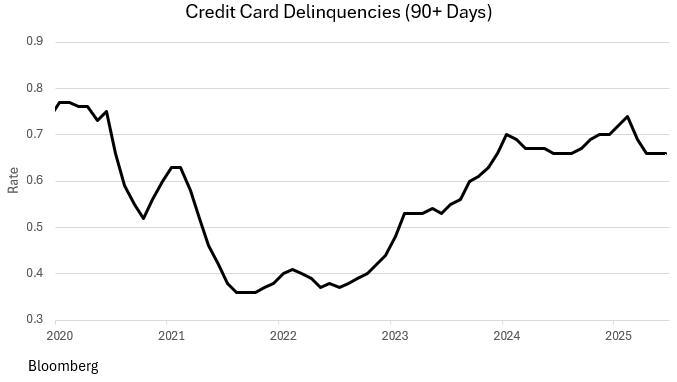

In addition, delinquencies are always a telltale sign of consumer stress. The chart shows the rapid rise in credit card delinquencies since 2022. Auto loan delinquencies are also on the rise. This has begun to show up in the retail sales data. The three-month trend in real consumer discretionary outlays has been negative for the three months ending in June (-1.2% annual rate April through June).

The Labor Market

As discussed in last week’s post, the labor market doesn’t appear to be so “solid” (Fed Chair Powell’s characterization).6 Revisions tend to be highly correlated with the business cycle. That means that negative revisions are associated with a weak economy, and positive revisions with a strong one. So, last week’s -258K large downward revisions to the May and June jobs data, the largest such revision going back to at least 1979, imply a rapidly weakening economy.3

About a quarter of those filing for Unemployment Insurance have been unemployed for at least six months.4 The mean duration of unemployment has risen to 24.1 weeks in July, a rapid rise from May’s 21.8 weeks. That’s a 2.3-week rise over a 2-month period.4 Outside of the Pandemic, the last time we saw a number that high was in 2017. In addition, the 1.974 million unemployment claimants is the highest since November ’21. The U3 Unemployment Rate only rose to 4.2% in July from 4.1%. What that number doesn’t reveal is the rising difficulty in finding a job. And because jobs are “hard to find,” the Labor Force Participation Rate (LFPR) has been falling. A rising number of people without a job have simply stopped looking, and that results in shrinkage in the labor force. So, the unemployment rate doesn’t rise as fast as it would have had those folks not dropped out. Using June’s LFPR, the July U3 would have risen to 4.5%, not the official 4.2%.

After the large payroll revisions to May and June data, over the past three months, payroll growth has averaged +35K/month, quite the come down from the usual +150K to +250K markets have become used to.3 The Nonfarm Payroll report has now joined the ranks of other labor market data showing weakness (the sister Household Survey has been screaming weakness in the job market for several months; -260K for July). The JOLTS (Job Openings and Labor Turnover Survey) data for July were the weakest since March ’20, and the Conference Board’s Consumer Confidence Survey had the weakest labor market components since March ’21.

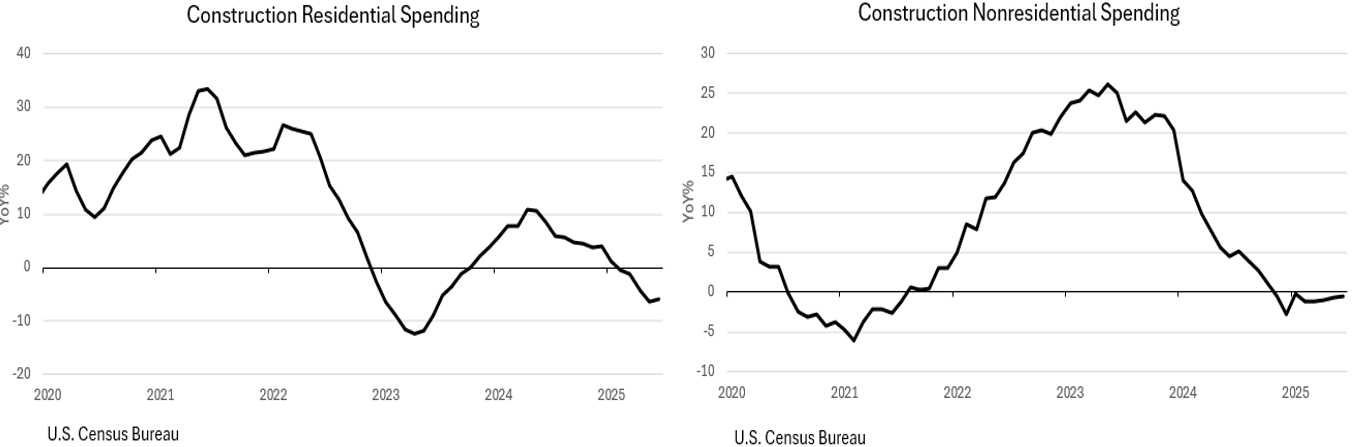

The Housing Market

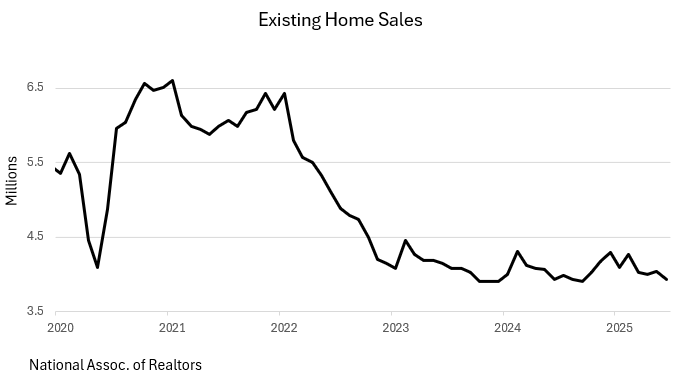

The labor market isn’t the only market showing signs of stress. Housing, both existing and new, has been suffering under the burden of high mortgage rates. As shown on the chart, Existing Home Sales have been in a funk since 2023, coinciding with the rise in interest rates engineered by the Fed.

And the charts for new construction, both residential and non-residential also show a slowdown beginning in 2024.

The Fed

It is clear that the housing market is suffering under the weight of high mortgage rates. And, as we have expressed in past blogs, it is our view that the Fed is behind the curve when it comes to lowering rates. They missed an opportunity at their late July meeting to lower the Fed Funds rate. September is their next opportunity.

Last week, Adriana Kugler announced her resignation from the Fed’s Board of Governors effective August 8th.5 President Trump has nominated Stephen Miran, currently the Chairman of his Council of Economic Advisers, to fill out her remaining term which ends on January 31st, 2026. He needs Senate confirmation.

It isn’t apparent if Miran’s appointment is a placeholder, or if Trump will nominate him for his own term (Fed Governor terms are 14 years in length). In addition, Jay Powell’s term as Chairman of the Fed expires in May 2026 although his term as a governor doesn’t expire until January 31, 2028. It is clear that Trump won’t renominate Powell to be Chairman. That leaves Governors Waller and Bowman, the two governors who dissented from the Fed’s recent stay put interest rate stance, and perhaps now Miran as the leading contenders to be the next Chair. Of course, since Miran’s term ends in January, it is possible for the next Chair to be someone not now in the spotlight.

Whatever the case, it is our view that the Fed is behind the curve in lowering rates. Both the labor market and the housing market, as discussed above, are suffering from a slowing economy; rate reduction is long overdue. Perhaps we will be surprised in September with a 50 basis point reduction (but don’t hold your breath).

Final Thoughts

Despite a slowing economy, the equity markets continued to rally with all the major indexes up solidly for the week. The S&P 500 (+8.6%) and the Nasdaq (+11.1%) are solidly in the black for the year, with the Dow (+3.8%) up more modestly. Only small caps (Russell 2000) are in the red (-0.5%) year to date.

Six of the magnificent 7 gained ground last week (ended August 8th). And one, Nvidia, closed on Friday at a new record high. Year to date, only Apple (-8.4%) and Tesla (-18.4%) have lost ground. Nvidia (+36%), Meta (+31%) and Microsoft (+24%) are showing healthy double digit gains year to date.

Consumer spending is slowing. It fell in the April-June period (-1.2% annual rate). And delinquencies have become an issue.

The sign on the revisions to the jobs data are highly correlated with the health of the economy. Positive revisions indicate a strong economy, negative indicate weakness. The large negative revisions to the May-June jobs numbers (-258K) tell us loud and clear that the economy is struggling. That is sure to show up soon in consumer spending data, in housing, and in the jobs picture.

The Fed missed an opportunity at its July meetings, holding the high interest rates steady instead of lowering. With Governor Kugler’s resignation from the Board of Governors, Trump has nominated his Council of Economic Advisers’ Chairman, Stephen Miran. He is a possible nominee to be the next chair (if he votes “correctly”) when Powell’s term as Chair expires next May.

Dr. Robert Barone, Ph.D. is an economist whose storied career spans numerous decades and positions within the world of finance. Since gaining his Ph.D. in Economics from Georgetown, he has been a Professor of Finance (University of Nevada), a community bank CEO (Comstock Bancorp), and a Director of the Federal Home Loan Bank of San Francisco, where he served as its Chair in 2004. He lives and breathes the world of finance, continuing to provide clients and avid Forbes readers with his latest market insights.

(Joshua Barone and Eugene Hoover contributed to this blog.)

Robert Barone, Joshua Barone and Eugene Hoover are investment adviser representatives with Savvy Advisors, Inc. (“Savvy Advisors”). Savvy Advisors is an SEC registered investment advisor. Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Ancora West Advisors, LLC dba Universal Value Advisors (“UVA”) is an investment advisor firm registered with the Securities and Exchange Commission. Savvy Advisors, Inc. (“Savvy Advisors”) is also an investment advisor firm registered with the SEC. UVA and Savvy are not affiliated or related.

Reference:

1 https://finance.yahoo.com/markets/

2 https://finance.yahoo.com/news/retail-sales-fell-june-first-185633408.html

3 https://www.cbsnews.com/news/federal-reserve-lisa-cook-jobs-report-concerning-economy-turning-point/

4 https://www.bls.gov/news.release/empsit.nr0.htm

5 https://www.federalreserve.gov/newsevents/pressreleases/other20250801a.htm