Closing a Pivotal Year for Markets

December provided a fitting close to one of the most eventful and consequential years markets have faced since the pandemic. In 2025, investors navigated a rare convergence of forces: still elevated, but slowing inflation, heightened geopolitical uncertainty, renewed trade and tariff tensions, a prolonged U.S. government shutdown that disrupted key economic data, and a decisive turn in monetary policy after one of the most aggressive tightening cycles in decades. At the same time, market leadership became increasingly concentrated, amplifying volatility and raising questions about durability beneath headline index strength.

Against that backdrop, December stood out not because it resolved every uncertainty, but because it brought greater alignment between policy, data, and expectations. Inflation continued to ease, the Federal Reserve took another step toward neutral policy, and markets began to shift their focus from navigating restrictive conditions to recalibrating for a post-tightening environment. After a year defined by adjustment and uncertainty, December felt less like a turning point and more like a moment of consolidation, a pause that allowed investors to take stock of how far the economy and markets had come.

December unfolded in two distinct phases. Markets rallied early in the month, briefly reaching new highs as investors responded to improving inflation data and clearer policy signals. That strength gave way to quieter, range-bound trading later in the month as year-end rebalancing, lighter liquidity, and positioning ahead of 2026 took hold.

December Highlights

The market entered December with growing conviction, supported by the resolution of the U.S. government shutdown and the resumption of official data releases and policy guidance.

Federal Reserve Action

At its mid-December meeting, the Federal Open Market Committee reduced the federal funds target range by 25 basis points to 3.50% – 3.75%. This marked the third rate cut of 2025, bringing cumulative easing to 1.75 percentage points from the cycle peak. While policymakers emphasized a continued data-dependent approach, markets generally interpreted the move as a signal that policy may be approaching a more neutral stance.

Equity Performance

The S&P 500 finished 2025 with a total return of 17.9%. While the index traded higher earlier in December, light holiday volume and year-end positioning led it to finish the month essentially flat, down 0.05%, narrowly snapping a seven-month winning streak1.

Nasdaq Resilience

The Nasdaq Composite lost 0.5% in December and closed the year with a 20.4% return, reflecting continued investor interest in select technology and AI-related themes, albeit with greater differentiation than earlier in the year1.

Featured Theme: Repositioning Toward Neutral

December marked a broader transition in market thinking, from operating under restrictive policy conditions to adjusting toward levels that many policymakers and investors view as closer to neutral. The Federal Reserve’s updated Summary of Economic Projections suggested that the expected path of the policy rate is nearer to estimates of neutral than to the previously restrictive stance, reinforcing the idea that the tightening phase may be coming to a close2.

Consumer activity also remained a notable source of resilience. The National Retail Federation forecasted that U.S. holiday season retail sales would grow roughly 3.7% to 4.2% year-over-year, pushing total seasonal spending above $1 trillion for the first time, and preliminary data from payment processors showed holiday retail spending up about 4.2% compared with the prior year3.

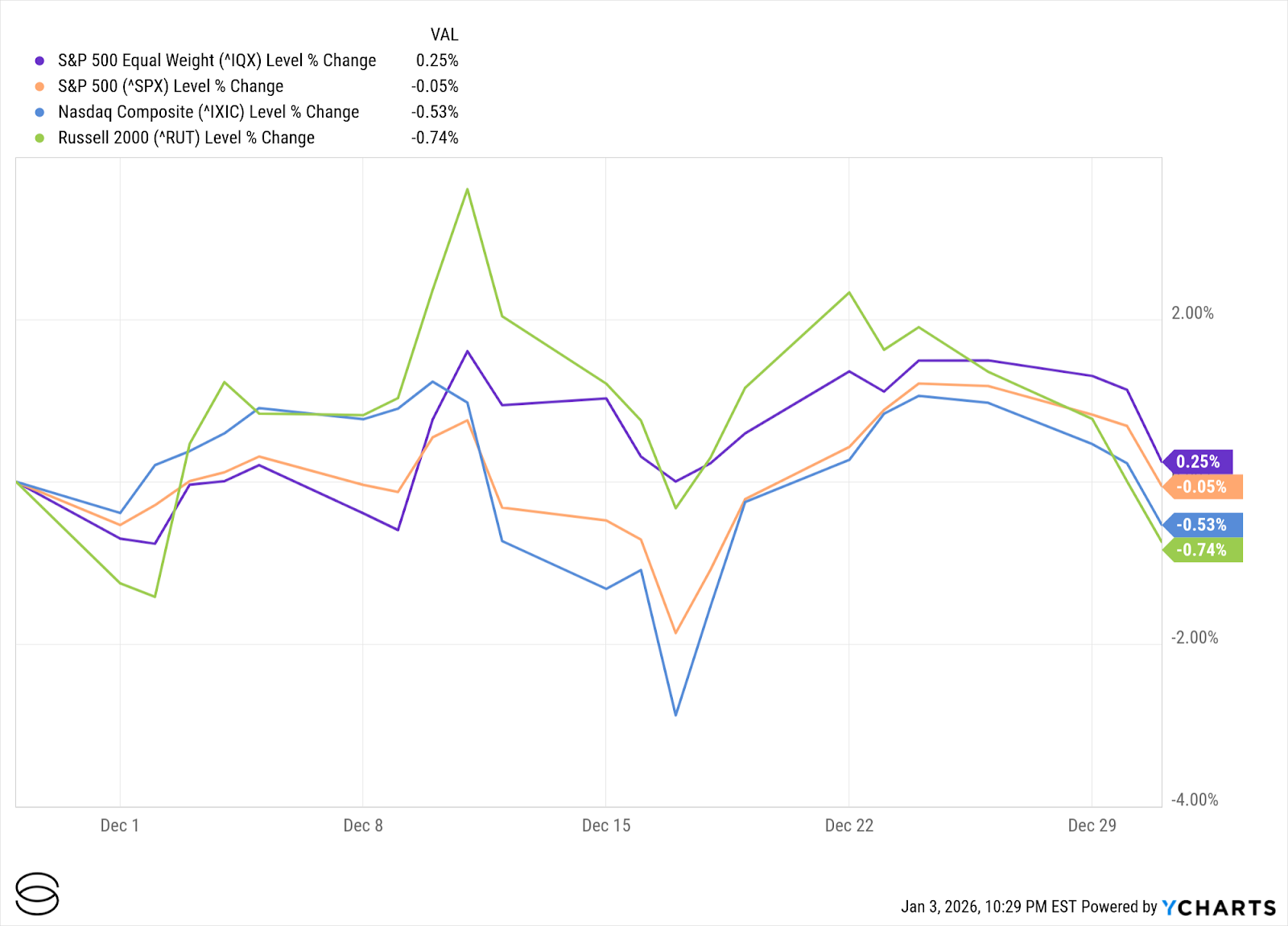

U.S. Markets: A Gradual Shift Toward Broader Participation

December trading in U.S. equities was marked by dispersion beneath relatively calm headline index performance. While major benchmarks moved little on a net basis, leadership within the market continued to rotate as investors reassessed crowded positions and became more selective about sources of return. As the month progressed, there was a noticeable willingness to look beyond mega-cap technology and toward sectors more closely tied to domestic activity and balance-sheet strength.

Overall, the S&P 500 finished December roughly flat, modestly outperforming the tech-heavy Nasdaq and small-cap equities. Under the surface, performance differences across styles and sectors highlighted a market that may be becoming less dependent on a narrow group of leaders and more sensitive to fundamentals such as earnings durability, financing conditions, and exposure to real-economy demand.

Exhibit 1: U.S. Equity Performance (December 2025)

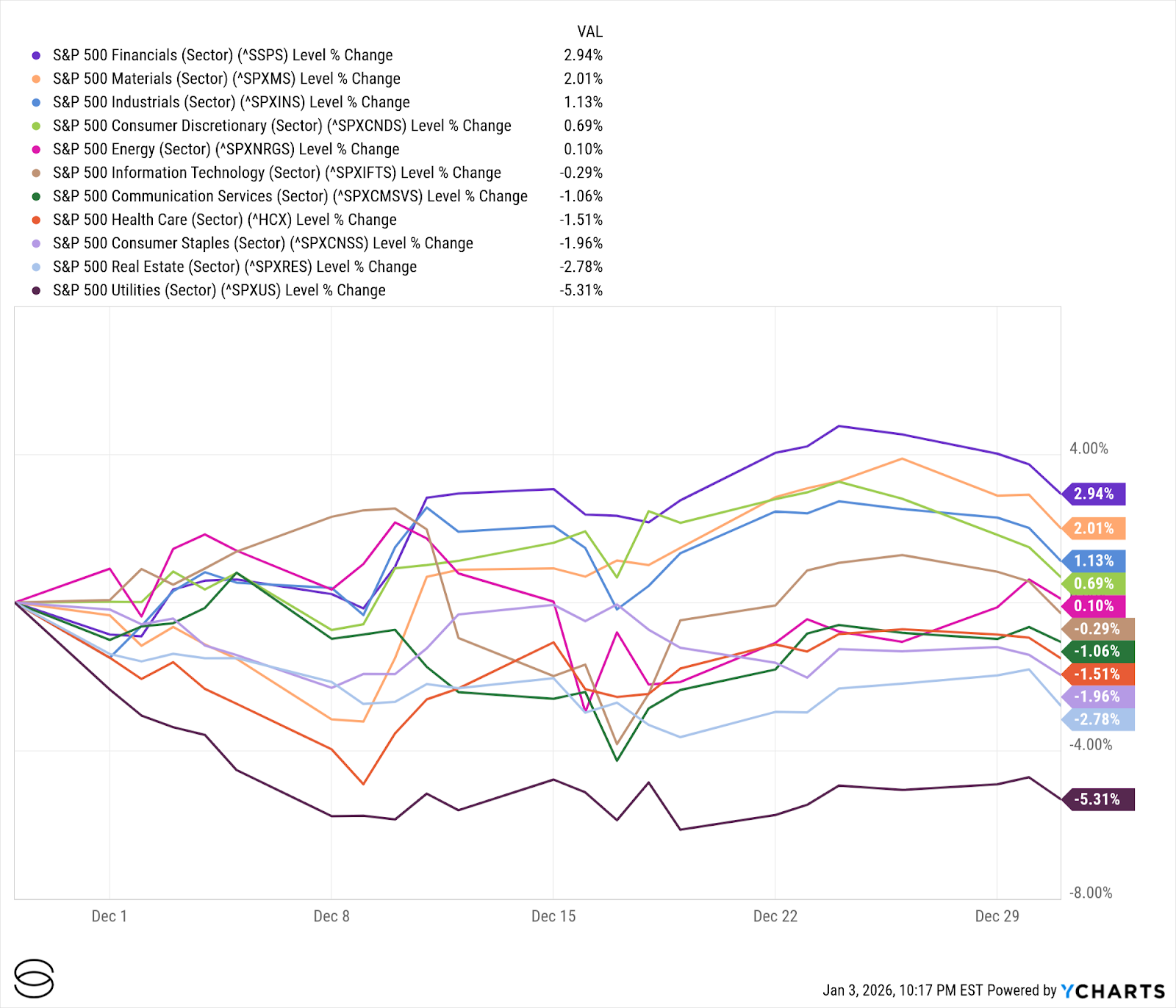

Sector Performance

Financials and Materials emerged as relative outperformers during the month. Financials benefited from improved confidence in nominal growth and a modest steepening in parts of the yield curve. Materials were supported by optimism around domestic industrial activity and infrastructure-related demand.

In contrast, Information Technology and Communication Services posted more muted returns. After a year of outsized gains, these sectors saw increased profit-taking and portfolio rebalancing, particularly in areas most closely tied to high expectations for long-term growth.

Small- and mid-cap equities remained uneven through December, with late-month trading continuing to favor larger-cap names amid lighter year-end trading volumes and positioning dynamics.

Exhibit 2: U.S. GICS Sector Performance (December 2025)

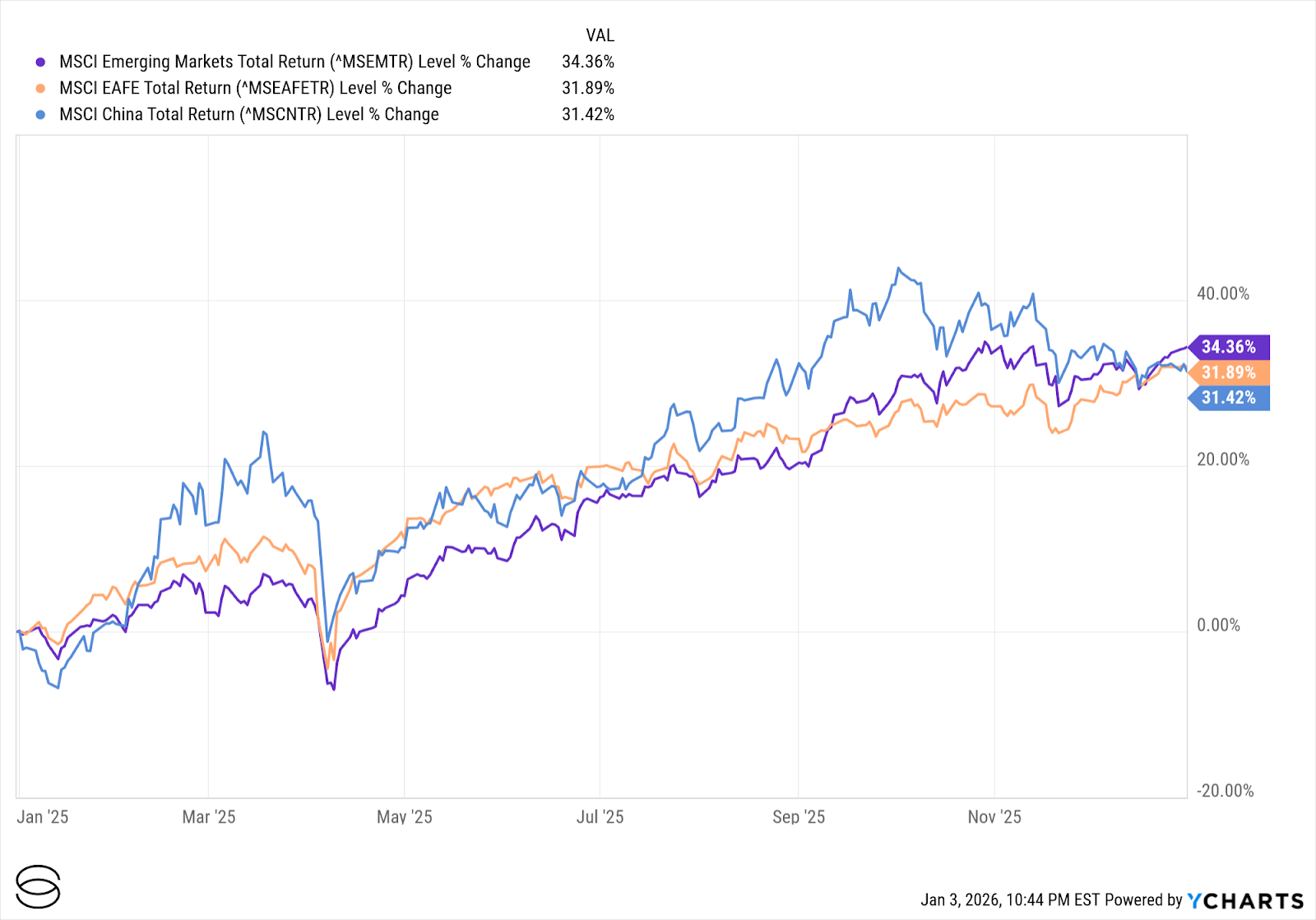

International Developed and Emerging Markets

International markets responded to the easing of U.S. policy expectations, though local fundamentals ultimately drove performance differences across regions. As global financial conditions became modestly less restrictive, investors placed greater emphasis on region-specific factors such as policy support, earnings momentum, currency dynamics, and starting valuations.

As of late December, Hong Kong’s Hang Seng Index stood out as one of the strongest performers among major global benchmarks, posting gains of nearly 35% year-to-date. Performance reflected a rebound from depressed valuation levels, targeted policy measures aimed at stabilizing growth, and renewed investor interest in select sectors. Canada’s TSX Composite and Japan’s Nikkei 225 also finished the year well ahead of many peers, benefiting from a combination of commodity exposure, export-linked demand, and, in Japan’s case, continued progress on corporate governance reforms alongside a competitive currency backdrop.

These outcomes underscore how regional policy choices, valuation starting points, and sector composition shaped investor returns in 2025. Markets with greater exposure to commodities, global manufacturing, or improving domestic confidence tended to fare better than those more directly tied to slower consumption trends or tighter financial conditions.

Emerging markets also delivered strong year-end results. The MSCI Emerging Markets Index rose modestly in December and closed the year with gains exceeding 30%. Performance was driven in large part by a recovery in Chinese equities, as policy support, easing financial conditions, and attractive relative valuations helped draw global capital back into the region following a prolonged period of underperformance.

Exhibit 3: International Equities Performance (2025 Year-to-Date)

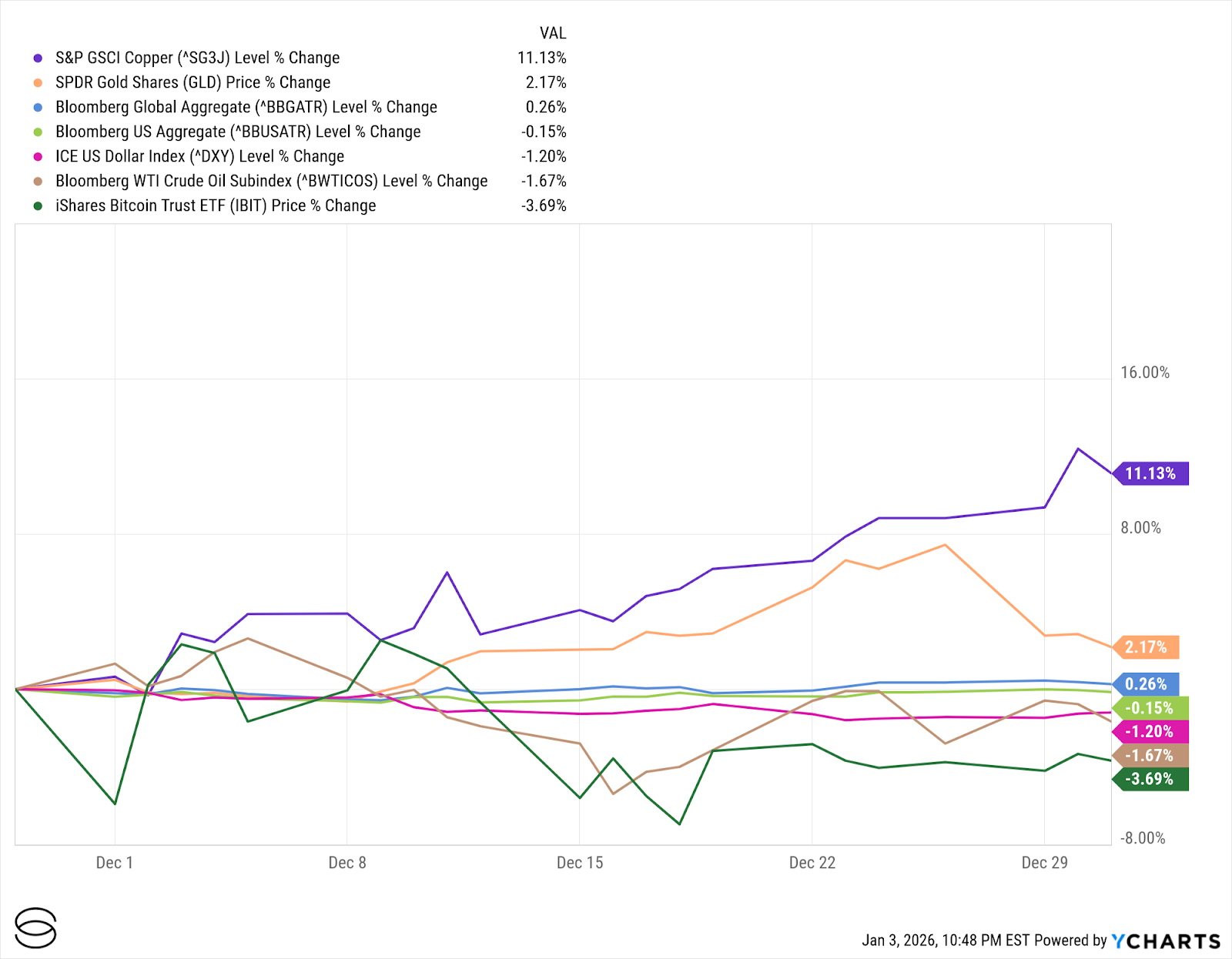

Cross-Asset Performance: Commodities Diverge

Fixed Income

Bond markets were more volatile in December as investors digested the Fed’s latest move. The 10-year Treasury yield ended the year around 4.14%, reflecting a constructive but patient outlook for future policy adjustments.

Commodities and Other Assets

Commodity performance diverged. Copper advanced on improving industrial demand expectations, while crude oil edged lower amid oversupply concerns. Precious metals found mid-month support as real yields eased. Digital assets were volatile, finishing the year off recent highs, but appear to have stabilized some since late November.

Exhibit 4: Cross Asset Performance (December 2025)

Economy and Policy: Clearing the Data Backlog

Following the resolution of the U.S. government shutdown, December served as an important catch-up period for federal statistical agencies. With October inflation data unavailable, markets focused closely on November releases to bridge the gap.

The November CPI report showed headline inflation at 2.7% year-over-year and core inflation at 2.6%, confirming continued progress on disinflation. While the data incorporated methodological adjustments following the collection lapse, it reinforced the broader trend of easing price pressures.

In his final press conference of the year, Chair Powell noted that with the policy rate now within a broad range of estimates for neutral, the Fed is well positioned to assess incoming data as it looks ahead to 2026.

Key Dates to Watch in January 2026

- January 9: December Employment Situation Report

- January 13: December CPI Inflation Data

- Week of January 12: Q4 Earnings Season Begins (Major Banks)

- January 28: Federal Reserve Policy Announcement

Conclusion: Closing the Book on 2025

December brought a sense of closure to a year defined by adjustment rather than equilibrium. Throughout 2025, markets navigated disinflation, shifting policy expectations, and periodic disruptions tied to fiscal and geopolitical uncertainty. By year-end, the broad direction of travel had become clearer, even if the destination itself remains uncertain.

What December ultimately provided was alignment. Incoming data, policy signals, and market pricing moved into closer agreement, reducing the tension that characterized much of the year. Inflation continued to ease, the Federal Reserve moved policy closer to neutral, and markets began to look beyond the constraints of a restrictive environment toward a more normalized backdrop.

As we head into 2026, the focus naturally shifts from whether policy will ease to how far and how durable the expansion proves to be. December’s crosscurrents suggest a market that is no longer reacting to extremes, but instead recalibrating within a narrower range of outcomes as investors digest a year that reshaped both expectations and behavior.

Anshul Sharma is Chief Investment Officer at Savvy Wealth, where he oversees the firm’s investment strategy, portfolio design, and platform innovation. He partners across product, marketing, and operations teams to deliver portfolios that take a methodological approach to balance customization with scalability for advisors and their clients. Before joining Savvy, Anshul spent nearly two decades at Bank of America, where he managed the Chief Investment Office’s Sustainable Model Portfolio Suite, launched new proprietary offerings, and, as Head of Alternative Investment Strategy, provided guidance and thought leadership to advisors around hedge fund, private market, and real asset strategies. He began his career as an Investment Strategist at U.S. Trust, designing multi-asset portfolios for high-net-worth and institutional clients. Anshul holds a Master of Financial Engineering from UC Berkeley and a Bachelor of Computer Engineering from Lehigh University. Outside of work, he is an avid tennis player, enjoys time with his wife, two sons, and their Bernedoodle, and is an auto enthusiast who loves cooking and travel.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Savvy Wealth Inc. is a technology company. Savvy Advisors, Inc. is an SEC registered investment advisor. For purposes of this article, Savvy Wealth and Savvy Advisors together are referred to as “Savvy”. All advisory services are offered through Savvy Advisors, while technology is offered through Savvy Wealth. The views and opinions expressed herein are those of the speakers and authors, and do not necessarily reflect the views or positions of Savvy Advisors.

Sources:

1 YCharts, as of Jan 5, 2026.