Donor-Advised Funds: Weighing the Pros and Cons for Charitable Giving

What are donor-advised funds (DAFs)? They’re one of the fastest-growing ways to give to charity, combining flexibility with potential tax advantages. A DAF lets you contribute assets and receive an immediate tax deduction. You can even recommend grants to your favorite nonprofits over time. In 2024, Fidelity Charitable donors recommended grants totaling $14.9 billion, a 25% increase from the previous year. We’ll explore the benefits of donor-advised funds and the potential drawbacks to consider before opening one.

Key Takeaways

- DTFs are charitable giving accounts that offer immediate tax deductions and long-term flexibility for making grants.

- DAFs can accept a wide range of assets, from cash and stock to real estate, offering unique advantages for high-net-worth individuals.

- Contributions to a DAF are irrevocable and must go to qualified charities.

- DAFs can play a role in both annual giving and long-term estate planning.

- Comparing providers and understanding fees ensures you choose the fund that best fits your financial goals and philanthropic interests.

Understanding Donor-Advised Funds

Before deciding if a DAF is best for you, it’s worth understanding what they are, how they work, and how they compare to other giving options. We’ll explore key differences between popular providers and alternatives for charitable giving.

What is a Donor-Advised Fund (DAF)?

A donor-advised fund is more than just a charitable giving account. It’s a flexible tool for managing philanthropy over time. When you contribute to a DAF, your donation is deposited into an account managed by a public charity, known as a sponsoring organization. You’ll receive an immediate tax deduction for your contribution. Meanwhile, the funds can be invested for potential growth while you decide which nonprofits to support.

This structure separates the act of giving from the act of granting, giving you time to plan your impact. You can contribute during a high-income year, claim the deduction now, and distribute grants to qualified charities later. It doesn't matter whether that’s weeks or years down the road.

How Do Donor-Advised Funds Work?

Here’s how the process typically goes:

- Contribute Assets: You make an irrevocable contribution of cash, stock, or other assets to your DAF.

- Invest with the Fund: The assets can be invested for potential growth, increasing the amount available for future grants.

- Recommend Grants: You choose when and where to distribute funds to qualified charities.

The sponsoring organization manages compliance and ensures that donations are directed only to IRS-approved nonprofits. While you can suggest how to invest and where to give, the sponsoring organization maintains final control over these decisions.

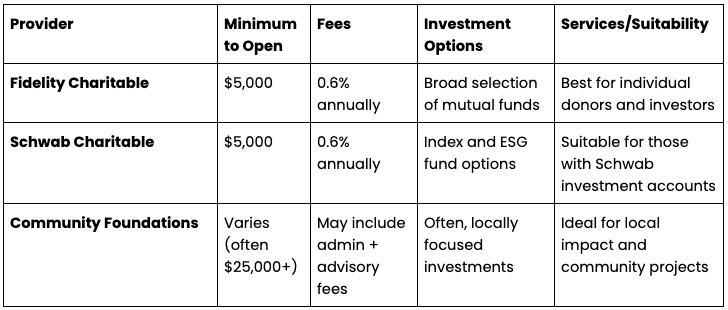

Comparing DAF Providers: Fidelity, Schwab, and Community Foundations

Not all donor-advised funds are the same. Fidelity Charitable, Schwab Charitable, and many community foundations have their own approach, minimums, and fees.

When comparing options, consider fees, investment flexibility, and the level of support you want in managing grants or investments.

DAF Alternatives: Direct Donations, Private Foundations, and Charitable Trusts

Donor-advised funds are just one way to donate a charitable gift. Direct donations are the simplest; you provide directly to a nonprofit and may claim a deduction that year. Private foundations offer more control but come with higher costs, more regulations, and annual distribution requirements. Charitable trusts enable structured giving and potential tax advantages, but setting up and managing them can be complex.

For individuals over 70½, qualified charitable distributions (QCDs) from an IRA can also serve as a tax-efficient way to make a gift. You can read more about how this fits your broader tax trust planning strategy here.

Tax Benefits and Financial Planning

The benefits of donor-advised funds are a primary reason they have gained traction in financial and tax planning. They enable donors to support meaningful causes while taking advantage of tax benefits that can be integrated into a broader tax optimization strategy. Below, we’ll break down how deductions work, what types of contributions qualify, and how DAFs can be a part of long-term estate and charitable planning.

Tax Deductions and Advantages of Donor-Advised Funds

When you contribute to a donor-advised fund, you receive an immediate income tax deduction, even if you distribute grants later. This means you can give now and decide where to send funds over time. This flexibility is one of the biggest benefits of a DAF, and working with your advisor to identify planning opportunities with your entire financial picture in mind can be a powerful combination. For example, clustering donations can help offset income or capital gain heavy years, or allow for itemization of tax deductions that might otherwise not be available. Unlike private foundations which must distribute at least 5% of average asset value each year, your advisor can also optimize your portfolio allocation to target the achievement of specific future charitable goals, maximizing growth, or seeking to preserve the funds value, as needed

Another key benefit is the ability to donate appreciated securities, such as stocks that have increased in value, without incurring capital gains taxes. You can claim a deduction for the fair market value of the asset, potentially reducing your taxable income.

Using a DAF tax deduction calculator lets you estimate your savings and show how charitable giving can complement your tax planning strategies throughout the year.

Donating Appreciated Stock to a DAF

Donating appreciated stock is one of the best ways to fund a DAF. Instead of selling the stock and paying capital gains taxes, you can transfer it directly to your sponsoring organization. The charity sells the stock tax-free, and the proceeds are available in your account for future grants.

Estate Planning with Donor-Advised Funds

Donor-advised funds also play a role in trust and estate planning. Many donors use them to continue charitable giving after their lifetime by naming successors or designating philanthropic beneficiaries.

DAFs also reduce the size of a taxable estate while allowing your philanthropic goals to continue. Some people also include DAFs as part of a charitable bequest in their wills, ensuring their values are reflected in future giving.

DAFs for High-Net-Worth Individuals

For high-net-worth individuals, DAFs are a valuable tool for HNWI financial planning. They make it easier to manage large or irregular income years by bunching deductions and donating more complex assets, like real estate or private business interests.

They also simplify ongoing charitable giving, as they offer a single platform to manage contributions, investments, and grants, eliminating the administrative burden of a private foundation. DAFs can be established in 24 hours or less with zero startup costs, while private foundations require legal incorporation, IRS Form 1023 approval (which can take six months or longer), and substantial attorney and administrative fees. Minimum asset thresholds are also much lower — typically $25,000 for a DAF vs. $2M–$10M+ for a private foundation. Ongoing annual costs run 0.85% or less for a DAF, compared to 2.5%–4% for private foundations

Contribution Limits for DAFs

While DAFs give you flexibility, there are limits to how much of your donation you can deduct each year. Donors are able to receive an immediate income tax deduction for cash contributions up to 60% of their adjusted gross income (AGI). In comparison, deductions for securities and other appreciated assets are capped at 30% of AGI. Any donations that exceed these limits can be carried forward for up to five years.

Management and Philanthropic Impact

Beyond tax benefits, donor-advised funds are shaping how people manage and track their charitable giving. They’ve become a bridge between personal financial planning and meaningful impact, letting donors stay engaged with causes while maintaining flexibility and structure. Below, we’ll look at how DAFs are managed, the growing role of impact investing, and how these funds support nonprofits over time.

Impact Investing & Custom Portfolios Through DAFs

Many DAF sponsors now offer impact investing options that combine financial growth with positive social and environmental goals. This means donors can invest their contributions in ESG (environmental, social, and governance) portfolios while waiting to recommend grants.

In fact, donors recommended more than $138 million in grants to impact-investing nonprofits in 2024. Fidelity Charitable also notes that sustainable investment portfolios are now available through most major DAF sponsors, including ESG-focused options for those who want their investments to reflect their values. Apart from ESG, DAFs have also expanded their general investment options with increased flexibility to create custom portfolios, subject to overall balance thresholds.

Private foundations may offer more customization options, but DAFs make it easier for donors to adopt responsible investing without needing extensive management or oversight.

The DAF Giving Process: Recommending and Tracking Grants

How do donor-advised funds work? Once contributions are made, donors can recommend grants to eligible charities through an online platform managed by the sponsoring organization. The process generally includes:

- Logging into your donor portal.

- Selecting the charity (which the sponsor verifies for eligibility).

- Recommending a grant amount.

- Tracking approval and distribution status through the dashboard.

The sponsor ensures the funds go only to qualified 501(c)(3) organizations, making the process simple and transparent. This structure maintains accountability while allowing donors to remain connected to their giving activity.

How DAFs Impact Charities

For nonprofits, DAFs can be a consistent and valuable source of support. Grants from these funds often arrive more reliably than traditional donations, giving organizations greater financial stability.

Research shows that DAF donors have a 59% year-over-year retention rate, compared to 46% for non-DAF donors. That means people who give through DAFs are more likely to continue supporting charities over time, creating a steady stream of funding that allows nonprofits to plan long-term.

DAFs also allow for anonymous giving, which some donors prefer for privacy or modesty reasons.

Can You Withdraw from a Donor-Advised Fund?

It is important to note that DAF contributions are irrevocable. Once you contribute to a DAF, the funds become property of the DAF. The sponsoring organization has legal control over them, and they must be used for charitable purposes.

You can recommend how and where the funds are granted, but you can’t withdraw the money for personal use. This structure ensures that all contributions ultimately support qualified charities, reinforcing the fund’s charitable intent.

Finding Balance in Charitable Giving

Donor-advised funds offer a flexible and accessible way to give. However, they’re not the only option. It’s worth considering the pros and cons of each option before opening an account.

Next Steps:

- Review your current charitable giving approach to determine if a DAF aligns with your goals.

- Compare DAF providers such as Fidelity Charitable, Schwab Charitable, and local community foundations.

- Talk with your financial advisor about how a DAF could complement your tax planning and estate planning strategies.

- If you’re already investing in impact opportunities, explore ESG options within donor-advised funds.

- Revisit your giving plan annually to match your donations with causes that mean the most to you.

Contact a Savvy Advisor Today!

I’m Brandon, Founder of Marathon Wealth Advisors. I help individuals and families turn complex financial decisions into clear, confident plans built for the long run. With nearly two decades of experience in wealth management and investment strategy, and both the CFA® and CFP® designations, I bring a disciplined, thoughtful approach to every client relationship.

Works Cited

- 2025 Fidelity Charitable Giving Report

- Donor-advised fund rules and contribution limits for 2024

- What is impact investing?

- Activating DAF Donors with Wealth Data for Maximum Impact

.webp)