What Should Your Next Dollar Do? A Simple Order of Operations for High Earners

When Jordan turned 32, life looked a lot like what he had worked toward for more than a decade.

He was a tech sales director earning around $260,000 a year between salary, bonuses, and RSUs. He and his wife owned a home, had two young kids, and had built a comfortable life that no longer revolved around worrying about bills. Their finances were stable. Retirement accounts were growing. There was money in savings. From the outside, things looked solid.

But higher income introduced a different kind of question. What should the next dollar actually do?

Jordan wasn’t trying to get rich quick, and he wasn’t interested in turning personal finance into a second full-time job. What he wanted was clarity in the form of a simple framework that made sure the money he worked hard to earn was being used intentionally.

Instead of chasing complicated strategies, he followed a straightforward order of operations — and the first step was protecting the foundation.

Speak with a Savvy Advisor Today

Key Takeaways

- Establishing a foundational emergency fund covering six months of expenses ensures that your primary financial needs are protected before moving into more aggressive investment strategies.

- Capturing the full employer 401(k) match is one of the highest-return financial decisions available and should be prioritized to maximize total compensation.

- High earners can maximize tax-advantaged growth by utilizing backdoor Roth IRA strategies and Health Savings Accounts (HSAs) as long-term investment vehicles.

- Consistently increasing your long-term savings rate through incremental adjustments during bonus seasons can help you reach a target savings rate in the mid-20% range.

- Building a diversified taxable brokerage account provides the flexibility to pursue goals like early retirement or business ventures without the restrictions of traditional retirement accounts.

Step 1: Protect the Foundation with an Emergency Fund

After reviewing monthly expenses, Jordan calculated that his family spent about $7,000 a month on core living costs once mortgage, childcare, groceries, insurance, and everyday spending were included. Because his role was specialized and replacing a high-income job could take time if the economy slowed, he aimed for the higher end of a typical emergency fund range.

That meant building toward six months of expenses, or roughly $42,000. He already had cash sitting in checking and savings, so the move was simple. Jordan shifted $25,000 into a high-yield savings account labeled “Emergency Fund,” kept enough in checking for normal cash flow, and set an automatic monthly transfer until the full target was reached.

With that in place, everything else became more structured. Any dollar above the emergency fund now had a job instead of sitting in cash by default.

Step 2: Capture the Full Employer 401(k) Match

Jordan’s employer offered a 6% 401(k) match, and he was already contributing enough to capture it. At his income level, that match alone represented over $15,000 a year in additional compensation, making it one of the highest-return decisions available.

Rather than leaving it there, he used the structure to clean things up. He checked that investments weren’t sitting in cash, reviewed his allocation, and considered whether traditional or Roth 401(k) contributions made more sense for his tax situation. The goal wasn’t perfection; it was making sure the account was actually working as intended.

Step 3: Fill Tax-Advantaged Space with Roth and HSA

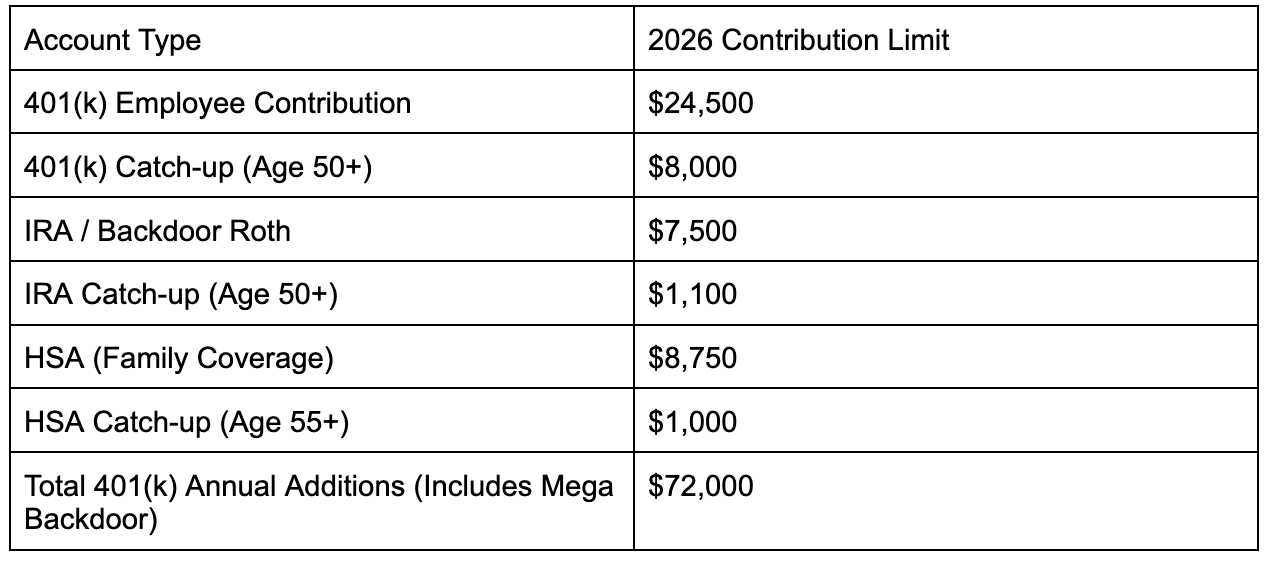

From there, he moved into Roth and health accounts. Because Jordan’s income exceeded direct Roth IRA limits (which for 2026 are $168,000 for single filers and $252,000 for married couples), he used a backdoor Roth strategy instead. That meant making nondeductible IRA contributions and converting them into a Roth.

This two-step process allowed him to bypass income restrictions by making a nondeductible contribution to a traditional IRA and immediately converting it to a Roth. For 2026, he was able to contribute $7,500 ($8,600 if he were age 50 or older). However, he had to be mindful of the pro-rata rule. Since the IRS views all traditional, SEP, and SIMPLE IRAs as one bucket, having existing pre-tax dollars in those accounts could have triggered an unexpected tax bill during the conversion.

Jordan further optimized his tax-advantaged space by maxing out a Health Savings Account (HSA). Rather than using it for immediate medical spending, he treated it as a long-term investment vehicle to capture its triple tax advantage: contributions lowered his taxable income, the investments grew tax-free, and his future withdrawals would be tax-free for qualified medical expenses.

Each step stacked on the previous one: emergency fund first, then retirement matching, then tax-advantaged space. Once those were in motion, Jordan used the same guide to place his next dollar toward his long-term savings rate.Step 4: Increase the Long-Term Savings Rate

His 401(k) contributions had originally sat at 6% for the match, but over time he gradually increased them, especially during bonus seasons. The changes were incremental, but meaningful over a year.

Combined with employer match, Roth contributions, and HSA funding, his total long-term savings rate climbed into the mid-20% range of income.

The Mega Backdoor Roth Option

For Jordan, the regular Backdoor Roth was just the beginning. Since he worked for a large tech firm with a flexible 401(k) plan, he was also able to utilize the Mega Backdoor Roth strategy. This allowed him to contribute far beyond the standard $24,500 employee limit by making after-tax contributions to his 401(k).

In 2026, the IRS allows total 401(k) contributions (employee + employer + after-tax) of up to $72,000. If his employer’s match didn’t fill that gap, Jordan could contribute the difference as after-tax dollars and immediately convert them to a Roth 401(k) or Roth IRA. This move effectively allowed him to shield tens of thousands of additional dollars from future taxes—a strategy particularly powerful for high earners who have already maxed out all other traditional buckets.

Step 5: Build Flexibility with Taxable Investing

At that point, the next dollar shifted into taxable investing. Jordan set up an automated $3,000 monthly investment into a diversified brokerage account. This bucket wasn’t tied to retirement rules or tax restrictions. It was flexible money that could support early retirement, a business idea, a second property, or simply more options later in life.

Addressing Concentration Risk in Company Stock

This is where Jordan noticed a quieter issue: concentration risk. Over time, RSUs had built up into a roughly $40,000 single-stock position tied to his employer. While the stock had done well, Jordan didn’t want his paycheck, bonus, and investments all dependent on the same company.

For many tech professionals, this double exposure is a significant risk. If the company or the tech sector faces a downturn, you risk losing both your primary income and a large portion of your net worth at the same time

So as RSUs vested, he began selling portions and reinvesting into a diversified portfolio.

Step 6: Plan for the Next Generation with 529s

With his own foundation secure, Jordan turned to his two young children. He chose to automate contributions to a 529 College Savings Plan, which offers tax-free growth and withdrawals for education. To maximize the benefit, Jordan took advantage of superfunding, which in 2026 allows a married couple to front-load five years of gifts (up to $190,000 per child) without triggering federal gift taxes. He also gained peace of mind from recent SECURE 2.0 rules: if his children don't use the full balance, they can roll over up to $35,000 (lifetime limit) into their own Roth IRA, provided the account has been open for 15 years.

By making education savings a disciplined part of his order of operations, Jordan ensured his next dollar was securing a debt-free future for his family.

Smaller Cleanup Decisions That Tighten the System

Alongside these bigger moves, smaller cleanup decisions tightened everything further. Old 401(k)s from previous jobs were consolidated. Excess cash stopped accumulating beyond the emergency fund. Investment accounts were checked to ensure everything was actually invested. Stock compensation became a bonus, not a dependency.

None of these actions were flashy, but all of them were meaningful. The result wasn’t simply a growing net worth, but a system where every dollar had a home before it even arrived.

Final Thoughts: A Simple Order for Each Dollar

Jordan didn’t build his financial system through complexity. He followed a simple order for each dollar: protect the downside, capture the match, use tax-advantaged accounts, increase long-term investing, then build flexibility.

For high earners, that kind of intentionality often matters more than any single investment decision. With a clear order of operations, the next dollar always has somewhere to go.

Frequently Asked Questions

What is the financial order of operations?

The financial order of operations is a strategic framework that prioritizes your dollars toward high-impact goals, starting with a base emergency fund and employer matching before moving into tax-advantaged accounts and flexible investing.

How much should high earners keep in an emergency fund?

High earners in specialized roles should aim for at least six months of core living expenses to account for potentially longer job search timelines and higher fixed lifestyle obligations.

What is a backdoor Roth IRA and who needs one?

A backdoor Roth IRA is a strategy for high earners—specifically those earning over $168,000 as single filers or $252,000 married filing jointly in 2026—to bypass income limits and build tax-free growth through a two-step contribution and conversion process.

What is RSU concentration risk?

RSU concentration risk occurs when a significant portion of your net worth—typically more than 10% to 15%—is tied to your employer's stock, making your financial stability overly dependent on a single company's performance.

How much should I be saving if I earn over $200K?

High earners should aim for a total savings rate in the mid-20% range of their gross income to ensure they are building enough wealth to maintain their current lifestyle throughout retirement.

What comes after maxing out tax-advantaged accounts?

Once you have filled tax-advantaged "buckets" like your 401(k), HSA, and Roth, your next dollars should be directed toward a taxable brokerage account to build flexibility for goals like early retirement or business ventures.

Speak with a Savvy Advisor Today

I’m Nathan Mirizzi, an Associate Advisor and CERTIFIED FINANCIAL PLANNER™ professional at Blue Barn Wealth, passionate about helping individuals build clarity and confidence around their financial future. I bring energy, analytical focus, and a strong foundation in personal finance to the clients I serve.

Contact a Savvy advisor

Contact a Savvy advisor