The Psychology of Market Panic (And Why Smart Investors Still Fall For It)

Most people think market panic is about information when it’s not. It’s all about wiring. When markets become volatile, our brain is doing two things at once:

- Trying to make sense of uncertainty

- Trying to protect us from loss

That’s why fear feels so logical in the moment. Our brains are actively building a case for why we should “do something” to stop the discomfort. That response is completely human. Throughout my 15+ year career as a financial advisor, I’ve had the opportunity to speak with thousands of clients during periods of uncertainty and market volatility. Covid. Russia invading Ukraine. Inflation spikes. Political turmoil. Interest rate hikes. Bank failures. Wars in the Middle East. Every single time, I hear some version of the same underlying question:

Will I be okay?

And while every crisis has different details, the emotional experience tends to feel remarkably similar. While this time may feel different, the reality is… most scary times do. The market has been through almost everything. It’s survived wars, recessions, inflation/stagflation/deflation, terrorist attacks, political chaos, pandemics, housing crashes, bank failures, and generations of people insisting, “No really, this time is different and I’m not going to be okay!”

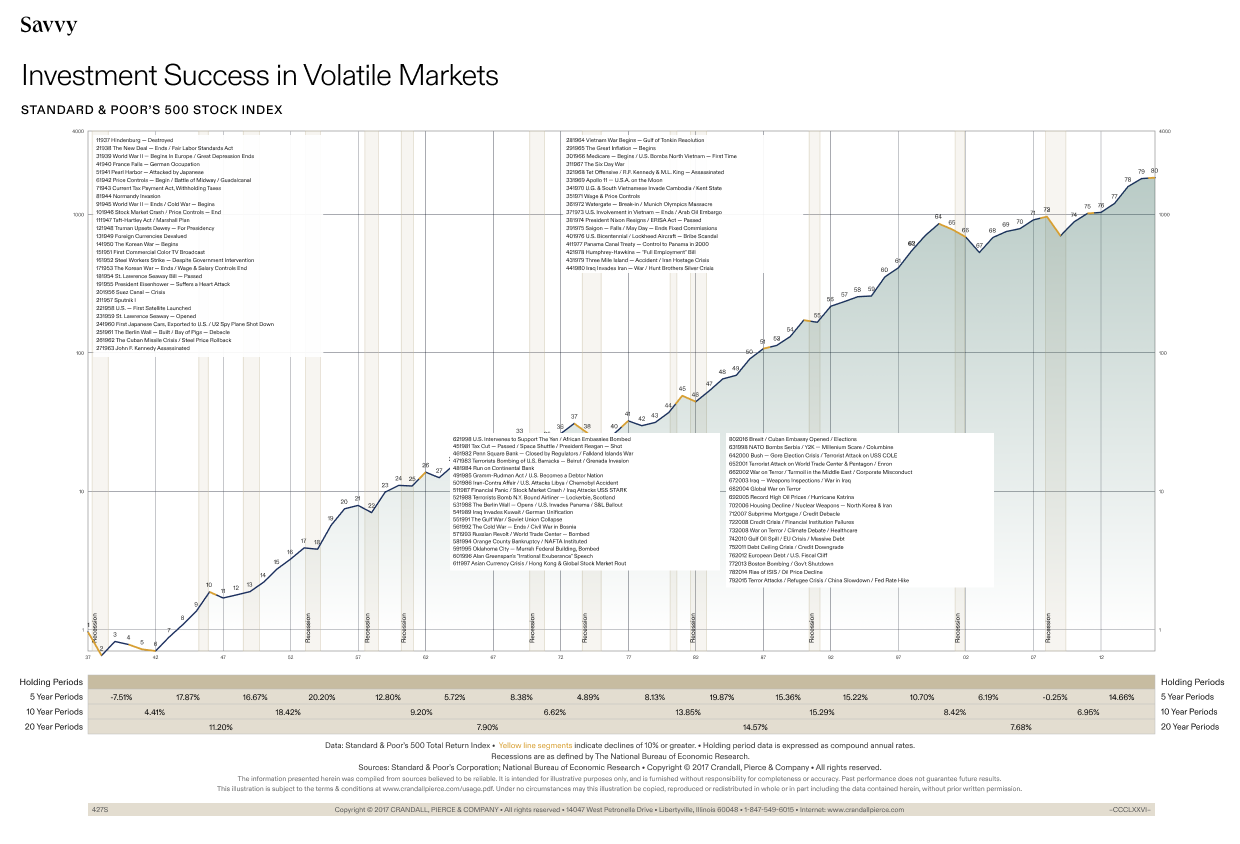

And yet history has rewarded patience. The long-term trend has been positive. Sure, it looks like an EKG along the way. But zooming out changes everything. Historically, about 7 out of every 10 years in the market have been positive, while roughly 3 out of 10 have been negative.¹ Give or take a year or two, that pattern has held for more than a century. And while we always have to say that past performance does not guarantee future results, it’s difficult to ignore the broader trend visible across virtually every major historical chart. Corrections, bear markets, and recessions are not signs that the system is broken. They are features of investing.

Volatility is the price of admission.

Listen, I don’t like it either, but I’ve come to accept it as a feature, not a bug. So yes, the market has been through just about everything imaginable. And despite the chaos, the long-term trend has remained remarkably consistent. It’s also essential to remember that while we may feel powerless when it comes to market volatility, we have more control than we realize. We mitigate as many risks as possible, while simultaneously planning for how to manage the uncontrollable unknowns.

Bull Markets vs. Bear Markets

I remember the first time I heard someone talk about the market using animal terms. I wasn’t sure if we were talking about the stock market or a viral YouTube animal video where a bull and a bear live in harmony and play with beach balls. I had zero experience when I joined the financial services industry in 2010 and certainly knew nothing about bull and bear markets. I’d vaguely heard about the “S&P 500” but had no clue what any of it meant. Simply put, the S&P 500 is an index that you can invest in. It’s basically like owning a tiny slice of 500 of the biggest companies in America all at once instead of trying to guess which individual company will win.

As you’ll see in the image below, the S&P 500 index has almost 100 years’ worth of data to analyze. That’s a lot of bear and bull markets. There have been roughly the same number of bull and bear markets over the past century (~27 each). The difference is that bull markets have historically lasted much longer and created substantially more wealth. Bear markets tend to be shorter and sharper. They make headlines, whereas bull markets build wealth. Before elaborating, let’s build a foundation of definitions regarding these two animals.

Market cycles are measured from peak to trough, so a stock index (like the S&P 500) officially reaches bear territory when the closing price drops at least 20% from its most recent high (whereas a correction is a drop of 10%-19.9%). A new bull market begins when the closing price gains 20% from its low. Stocks lose 35% on average in a bear market, whereas stocks gain 112% on average during a bull market. Approximately 42% of the S&P 500 index’s strongest days in the last 20 years occurred during a bear market. (source #2 below) What’s more, another 36% of the market’s best days occurred in the first two months of a bull market, before it was clear a bull market had even begun. Said another way, the best way to somewhat gracefully ride the waves of a downturn is to stay invested… with one caveat: There must be an intentional, well-thought-out plan in place to justify staying invested when the market’s tanking. This is where asset location planning comes into play.

So often in our industry, we focus primarily on asset allocation (i.e. mix of stocks and bonds within an investment portfolio). This is one of the many differences between wealth management and investment management. Investment managers tend to only focus on investments, managing money, and asset allocation. Wealth Managers (that’s me) must focus on the entire picture – not just investments. A major responsibility as a Wealth Manager that I never take lightly is the importance of asset location planning – i.e. having various buckets of money that align with the goals for that money and the time horizon for when the funds might be used.

NOW / NEAR / FAR

Let me tell you about my family friend Bob. He had all his money invested in a 401k through his employer and retired in 2008 when the market dropped 50%. He’s a DIY guy who never saw the value of working with an advisor. When the crash came, he didn’t have a NOW bucket of money or a NEAR bucket. All his wealth was tied up in the FAR bucket, his 401k. When his $2MM became $1MM, his only option was to draw income from his 401k. He had no other option but to tap this one investment account for all his retirement income needs. If he was my client back in the day, he would’ve had three main buckets of money: NOW, NEAR, and FAR. The NOW bucket refers to liquid cash that can be accessed at any time (i.e. an emergency savings account). Bob had a few thousand in his checking account. The NEAR bucket refers to a more conservatively invested portfolio with a shorter time horizon. We may need the funds sooner, so we can’t afford to take on a bunch of risk with these dollars. I typically encourage clients to pull from the NEAR bucket for income needs when the FAR bucket (like a 401k) is getting hammered by a market sell-off. Bob only had one bucket: FAR. His 401k was not too aggressive, since only 60% of his money was invested in stocks. But when stocks fell 50%, his 401k took a major hit. Bob didn’t know what he didn’t know, and that cost him dearly. In the industry we call this sequencing risk. In Bob's case, he didn’t have the luxury of staying invested during the 2008 financial crisis. He had to pull money out of the market and out of his 401k to rebuild his paycheck since he’d already retired from his job. If he’d had a bucket of money to access for living expenses other than his 401k (NOW + NEAR), he could’ve left the investments alone in the 401k and waited to tap those funds until after the market recovered.

I am the Wealth Manager for 44 clients and a handful of my clients are either nearing retirement or in retirement. Every single one of them has NOW money, NEAR money, and FAR money. That gives us tremendous flexibility when it comes to pulling different levers for different needs, given different economic conditions. I never want my clients to be forced to sell at a bad time. Taking a now/near/far approach through asset location planning gives clients a tremendous amount of peace during times of market volatility.

It’s impossible to time the market’s downturns and recoveries. That’s why it’s essential to mitigate as many risks as possible. Crystal balls still don’t exist in our industry, so the onus is on us to create various buckets of money to achieve different objectives despite ever-changing and evolving economic conditions. Remember, a bear market doesn’t automatically mean we’re in an economic recession. There have been approximately 27 bear markets since 1928, but only 15 recessions during that time.3

Not only has the market historically recovered from downturns, but the difference between bull and bear markets is massive. Bear markets can absolutely feel brutal in the moment, but in the words of my Granny “This too shall pass.” Using simple math, you’re in a bear market when the $100K you invested in stocks becomes $80,000 or less. And when you’re living through one, it can feel like the pain will never end. It will. A solid, strategic financial plan focused on asset allocation and asset location is crucial and makes the pain a little more bearable. Pun intended – sorry I had to. Historically, bull markets have lasted significantly longer and produced dramatically larger cumulative returns. That distinction matters more than most people realize. While downturns tend to dominate headlines and emotions, expansions are where long-term wealth is built. Either the market recovers like it always has for more than a century… or we’re dealing with a level of societal collapse where your portfolio is no longer the primary concern. It’s time to reframe our relationship with market volatility to sound something like this:

The market crashes.

Stocks go on sale.

Fight the instinct to run away from the sale.

The Importance of Staying Invested

This next concept is one of the biggest. One chart in particular shows the long-term impact of pulling money out of the market… even for just one year.

The green line represents the investor who stayed invested through the downturn. The gold line represents someone who got scared, pulled money out of the market, then got back in a year later once things “felt safer.” And the red line represents the investor who exited the market entirely and stayed in cash.

Can you pull your money out of the market? Absolutely. It’s your money. That’s exactly what I tell my clients. We’re simply the stewards who’ve been entrusted to care for the dollars. My role as a Wealth Advisor is to help steward it wisely and help clients understand the long-term consequences of certain decisions before emotions make those decisions for you. But this graph right here is why staying invested matters so much.

The investor who stayed invested ended with nearly $300,000 versus less than $200,000 for the investor who waited just one year to get back in. That gap is huge. And most people don’t realize that some of the strongest market gains tend to happen during periods of fear, uncertainty, and recovery. In other words, the moments people feel most tempted to leave the market are often the exact moments that matter most.

Why Long-Term Perspective Matters

You’ll love this next chart too.

There’s very little gold on the image, and one statistic in particular really stands out: historically, 15-year annualized stock market returns have been positive 100% of the time. Now of course, for the eleventy-billionth time we still have to say that past performance does not guarantee future results. But there are very few things in investing with a historical data point that strong – especially not 100%! Comparing market downturns to the subsequent expansions that followed helps explain why long-term investors have historically been rewarded for staying invested during periods of volatility. The downturns feel terrifying in the moment. But historically, the recoveries and expansions that followed have been dramatically larger and longer-lasting.

That’s the power of compounding over time. And it’s why temporary declines have historically mattered far less than long-term participation in the market. Over time, clients who remained invested through difficult periods experienced far better outcomes than those who reacted emotionally and exited the market.

The Role of a Trusted Advisor

This is also why having a strong financial plan and an advisor you genuinely trust matters so much. When markets experience high highs and low lows, you need more than information. You need perspective and strategy. Sometimes, you simply need someone reminding you not to make a permanent decision based on a temporary emotional state.

As a fiduciary, my responsibility is not to ignore fear or dismiss emotion. Quite the opposite, which works well for the empathetic bleeding heart that I am. My superpower is to help clients separate temporary emotion from long-term strategy. Money is personal, and it’s extra scary when we see the number on the screen go down. All our concerns are valid. Our emotions are human. I understand. Having said that, history consistently reminds us that reacting out of fear can have both near-term and far-term consequences. That’s why I will almost always encourage clients to stay invested, stay disciplined, and stay focused on the bigger picture. We’ve co-created a solid plan that was built to withstand various economic and market conditions.

Final Thoughts

There will always be headlines, uncertainty, and reasons to panic. Depending on when you’re reading this, the market may be soaring… or struggling. As I write this, the market is hitting unbelievable new highs. And while record highs are exciting, they’re also periods where risk often gets ignored. Looking back to the late 19th century, periods of euphoria and periods of volatility are deeply connected.

We will absolutely have another correction. Another bear market. Another recession. We just don’t know when. After falling more than 50% during the 2008 financial crisis, the stock market not only recovered, but went on to gain nearly 385% over the following decade.

Fear is normal. Volatility is normal. Panic is human.

Building real, sustainable wealth isn’t about never feeling fear. We humans aren’t emotionless robots. Pursuing financial freedom and peace of mind is about not letting that fear make your financial decisions for you. Sometimes F-E-A-R stands for False Evidence Appearing Real. My passion is helping clients filter out the noise, separate fact from fiction, gain perspective, and continue putting one foot in front of the other.

Please note: This commentary is intended for general educational discussion purposes only and should not be interpreted as individualized investment, tax, or legal advice. Past performance does not guarantee future results. All investing involves risk, including the potential loss of principal.

.webp)

Lindsey is a Private Wealth Advisor who believes peace of mind is not found in projections but built through genuine partnership. She helps clients transform financial complexity into clarity by creating personalized roadmaps that deliver real, sustainable freedom. Lindsey is especially passionate about guiding dynamic women as they reclaim their financial power or step into it confidently for the first time. Her approach seamlessly blends sharp analytical thinking with deep intuition: a neurodivergent, creative mind that spots patterns others miss, paired with an obsessive attention to detail that ensures nothing falls through the cracks.

¹ Based on Dow Jones annual return data from 1896–present. See: DQYDJ, "Dow Jones Annual Return Rankings," dqydj.com; and Roger G. Ibbotson & Rex A. Sinquefield, Stocks, Bonds, Bills, and Inflation: Historical Returns (1926–1978), CFA Institute Research Foundation, 1979.

1 Source for bear/bull market stats is Ned Davis Research as of 3/31/25 unless otherwise noted.

2 Source: Ned Davis Research, 4/25. Time period referenced is 1/1/03–3/31/25.

3 Source: National Bureau of Economic Research, 12/24.

All advisory services are offered through Savvy Advisors, Inc. ("Savvy Advisors"), an investment advisor registered with the Securities and Exchange Commission ("SEC"). Savvy Wealth Inc. ("Savvy Wealth") is a technology company and the parent company of Savvy Advisors. Savvy Wealth and Savvy Advisors are often collectively referred to as "Savvy".

Lindsey Leaverton is an investment advisor representative with Savvy Advisors, Inc. ("Savvy Advisors"). Savvy Advisors is an SEC registered investment advisor. The views and opinions expressed herein are those of the speakers and authors and do not necessarily reflect the views or positions of Savvy Advisors. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy.

.webp)