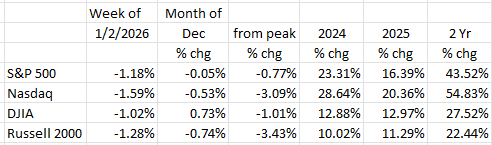

The table shows the growth rates in the major averages for 2024 and 2025. The S&P 500 is up nearly 45% over the two years ended 12/31/25 while the tech heavy Nasdaq grew more than 56% over those two years. Because the DJIA and Russell 2000 are void of major tech companies, their two-year growth rates, while substantial, lagged those tech heavy indexes.6

The consolidated reporting charts are for informational purposes only and should not replace the official reporting made available by each index, custodian, market and/or security.

The consensus says that equity prices will be higher next December than they are today; no doubt heavily influenced by the two year and counting “bull” run. Possible? Of course! Probable? We think that it depends on whether the economy can avoid a Recession.

The “K-shaped” Economy

There is evidence of a “K” shaped economy emerging with high end earners spending and supporting Consumption while those of lower means bargain hunt. Q3’s real GDP growth was a strong 4.3% (annual rate), besting Q2’s 3.8%.1 The strong sectors were health care, apparel, recreational vehicles and services, while hotels, restaurants, auto sales, furniture/appliances, and construction (both residential and commercial) showed mild contraction. Nominal incomes grew at a 2.8% annual rate in Q3 (about flat after inflation).2 To achieve the rise in consumption while real incomes were flat, consumers had to dig into their savings with the savings rate falling to 4.2% in Q3 vs. 5.0% in Q2 and 5.2% in Q1.3 In addition, it looks like nearly 60% of real GDP growth, and all the growth in consumer spending, came from that fall in the savings rate. That says a lot about the real state of the economy.

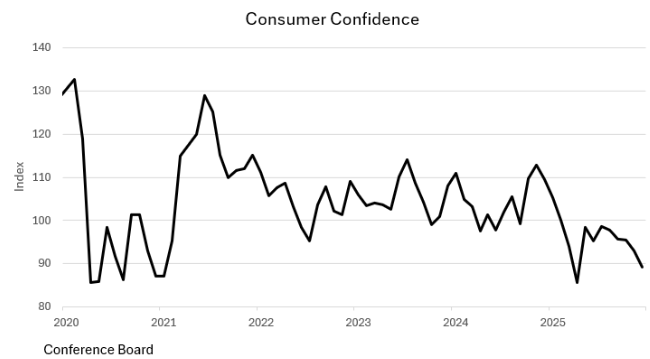

While the reported data show a strong economy, the sentiment survey data, which tend to be leading indicators, tell a different story. The Conference Board’s Consumer Confidence Index showed up in December at 89.1, a big miss from the consensus estimate at 91.0, and well below November’s 92.9. This was the second weakest reading since January ’21.

The K-shape once again revealed itself, with higher earning consumers ($125K+) scoring a 111 index while those in the $35K-$50K bracket showed up at 76.8, near a five-year low.4 To this point, the minutes of the December Fed meeting indicated that “lower-income households had become increasingly price sensitive and were making adjustments to their spending in response to the outsized cumulative increase in the prices of basic goods and services over the past several years.”5 It is also noteworthy that both homebuying intentions (5.7% December vs. 6.2% November) and vacation plans (38.7% December vs. 45.1% November vs. 46.7% October) continued on a downtrend. The vacation index is the lowest it has been since February ’21.

With regard to equity prices, the share of consumers seeing the indexes moving higher next year rose to 52.0% in December (vs. 50.8% in November). This was the fourth highest reading in the index’s history (data back to 1987).4 Those seeing lower stock prices at the end of 2026 were less than 25% (24.4%).

Is the Economy Strong?

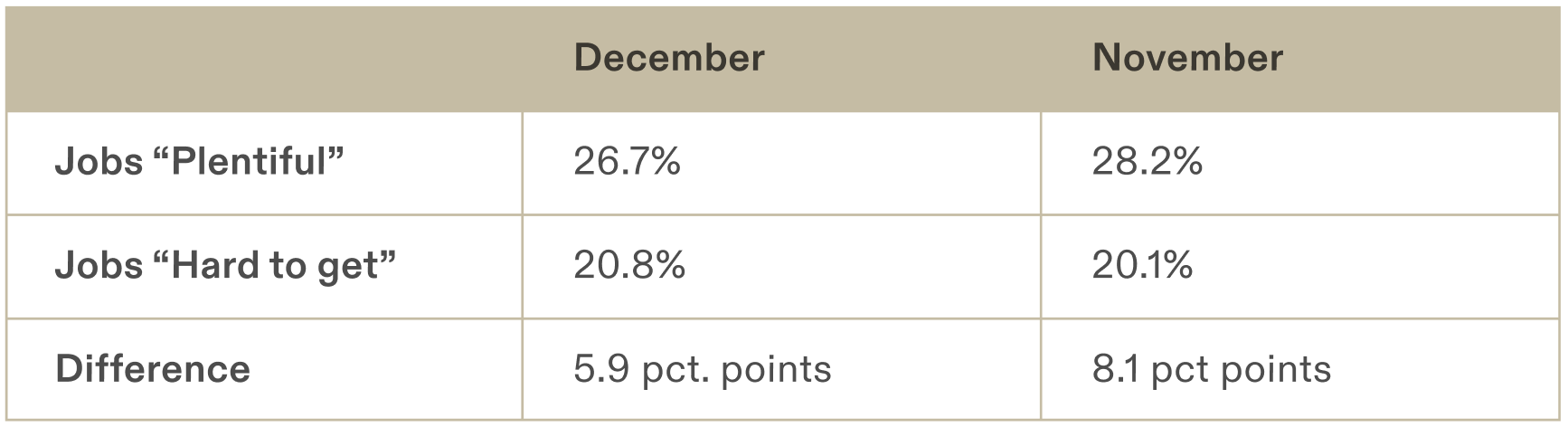

There appears to be a dichotomy between the strong GDP number (+4.3% Q/Q at an annual rate) and the deteriorating attitudes of the American public regarding their economic prospects for the year ahead. The Conference Board’s Consumer Confidence Index was 89.1 for December.4 That’s the lowest since April and second weakest since January 2021. That survey asks respondents if jobs are “plentiful” or “hard to get.” The table shows the November and December responses.

The 5.9 percentage point difference in December was the lowest reading since February ’21 (when the U3 unemployment rate was 6.2% versus 4/6% currently), indicating that there is growing stress in the labor market.

That same survey asks households if they expect stock prices to be “higher” or “lower” at the end of 2026. An astounding 52% said “higher,” the fourth highest reading on record (back to 1987), while those saying “lower” were just 24%, i.e. more than two “bulls” for every “bear.” There appears to be a disconnect here. On the one hand, the job market has tightened, but that doesn’t appear to have hit home yet when it comes to the equity markets.

The ”Wealth Effect”

For sure, there is a “wealth effect” emanating from the equity market to the economy. Unfortunately, that wealth effect impacts mainly the well-to-do, i.e., those that have substantial equity market investments. This results in what economists call a “K-shaped economy,” with the wealthier benefiting from significant double-digit gains in equity investments (see the table at the top of this writing), while those without such investments seem to be hurting. It is this higher income group that has continued to spend while retail businesses have reported that lower income groups are “bargain hunting.” Sooner or later, there is going to be a “correction” in the equity markets, and, when that occurs, the equity “wealth effect” will run in reverse. Whether that is significant or not depends on the magnitude and duration of that “correction.”

Components of GDP

Let’s dig deeper into Q3’s real GDP growth of 4.3%:

- Imports subtract from GDP (foreign produced). Import volumes contracted in Q3. This was primarily due to the “frontrunning” of the tariffs in Q1 and Q2, i.e. buying ahead prior to tariff implementation so as to pay the lower tariff free price. According to Rosenberg Research, contracting import volumes added 80 basis points (.8 percentage points) to Q3’s real GDP growth.

- In addition, the “wealth effect” from rising equity prices added 240 basis points (2.4 percentage points) to Q3’s GDP gain. We note that the Fed is cognizant that this “wealth effect” is a two-edged sword. Here is a snippet from the minutes of the Fed’s December meeting:

A majority of participants mentioned evidence of stronger spending growth for higher-income households, while lower-income households had become increasingly price sensitive and were making adjustments to their spending in response to the outsized cumulative increase in the prices of basic goods and services over the past several years. (Fed minutes December 9-10, 2025)

- Absent the import issue and the equity wealth effect, it appears that real GDP growth was closer to 1%. And let’s not forget, when we get the inevitable equity market “correction,” we may well see a huge slowdown in household spending. Enough to cause a Recession? That depends on the size and duration of the “correction” and its negative wealth effect impact on consumer spending.

So, while the economy looks strong and healthy from a numbers standpoint, absent the equity wealth effect and the frontrunning of the tariffs by U.S. importers, real repeatable GDP growth was likely closer to 1% than the 4.3% recently released number.

An equity market correction, depending on its size and duration, may be all that is needed (through the resulting negative wealth effect) to cause the Recession we’ve been avoiding for the last few quarters.

Final Thoughts

Equity prices continued their “bull” run in 2025. The major indexes were all up double digits, led by the tech heavy Nasdaq (+20.4%).

There is a huge volume of evidence that lower income households have been pinched by inflation, while households with substantial equity investments benefitted from the equity markets’ run-up allowing them to support Consumption in 2025.

Yet, despite rising equity prices, Consumer Confidence fell in December to the second lowest reading in nearly five years. It appears that lower income households are feeling the pinch of continuing high inflation. Despite that, 52% of consumers surveyed see equity prices moving higher in 2026, while less than 25% see lower prices over that time horizon.

Emerging trends indicate that consumer spending is waning. This is a trend that should be closely watched, as Consumption is a primary economic driver.

Robert Barone, Ph.D.

(Joshua Barone and Eugene Hoover contributed to this blog.)

Robert Barone, Joshua Barone and Eugene Hoover are investment adviser representatives with Savvy Advisors, Inc. (“Savvy Advisors”). Savvy Advisors is an SEC registered investment advisor. Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Ancora West Advisors, LLC dba Universal Value Advisors (“UVA”) is an investment advisor firm registered with the Securities and Exchange Commission. Savvy Advisors, Inc. (“Savvy Advisors”) is also an investment advisor firm registered with the SEC. UVA and Savvy are not affiliated or related.

Dr. Robert Barone, Ph.D. is an economist whose storied career spans numerous decades and positions within the world of finance. Since gaining his Ph.D. in Economics from Georgetown, he has been a Professor of Finance (University of Nevada), a community bank CEO (Comstock Bancorp), and a Director of the Federal Home Loan Bank of San Francisco, where he served as its Chair in 2004. He lives and breathes the world of finance, continuing to provide clients and avid Forbes readers with his latest market insights.

(Joshua Barone and Eugene Hoover contributed to this blog.)

Robert Barone, Joshua Barone and Eugene Hoover are investment adviser representatives with Savvy Advisors, Inc. (“Savvy Advisors”). Savvy Advisors is an SEC registered investment advisor. Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Ancora West Advisors, LLC dba Universal Value Advisors (“UVA”) is an investment advisor firm registered with the Securities and Exchange Commission. Savvy Advisors, Inc. (“Savvy Advisors”) is also an investment advisor firm registered with the SEC. UVA and Savvy are not affiliated or related.

Resources