Estate Taxes Explained: How to Protect Your Wealth and Legacy in 2026

The estate tax can take a significant share of what you’ve spent decades building, with the federal rate reaching as high as 40% once an estate exceeds the exemption by more than $1 million1. While the One Big Beautiful Bill Act (OBBBA) permanently raised the federal exemption rate to $15 million per person starting in 2026, that headline number doesn’t eliminate the need for planning decisions for high-net-worth families. Asset growth, state-level taxes, and future law changes still influence outcomes. Below, we’ll break down how today’s rules work and how to use them to preserve wealth across generations.

Connect with a Savvy Advisor Today!

Key Takeaways

- The federal estate tax exemption rises to $15 million per person in 2026, but the state estate taxes can apply at much lower levels.

- Estate taxes apply only after deductions and exemptions, so structure is key.

- Lifetime gifting and trust strategies can move future growth outside your taxable estate.

- Business owners often need additional planning to avoid forced sales and reduce estate tax exposure.

- Regular reviews keep your estate plan current as your wealth and life change.

What is the Estate Tax and How Does It Work?

Estate taxes apply when someone passes away and leaves money, property, or other valuable assets to heirs. In simple terms, the federal government might tax the transfer of wealth from an estate to the next generation, but only after deductions and the federal exemption are applied.

Federal Estate Tax Fundamentals

The federal estate tax is a “transfer tax” based on the fair market value of what a person owns at death. It applies to the transfer of assets from the deceased person to their heirs. To calculate it, the estate adds up the gross estate value (i.e., real estate, investments, business interests, and cash). Then it subtracts allowed deductions, including debts, administrative costs, and certain expenses. The result becomes the taxable estate.

This system also uses the “Unified Credit,” which lets you transfer a certain amount of wealth tax-free either during your lifetime or at death. For 2026, the OBBBA increased the federal estate tax exemption to $15 million per individual (or $30 million for married couples)2 and set the annual gift tax exclusion at $19,000 per recipient.

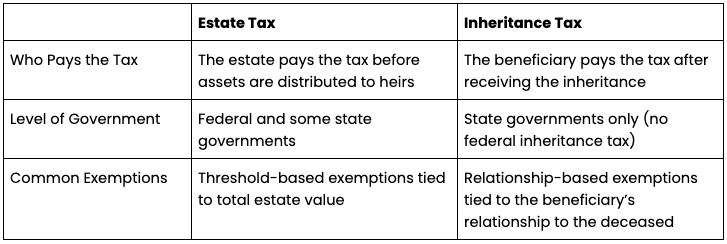

Estate Tax vs. Inheritance Tax: Understanding the Difference

Many people mix up inheritance tax and estate tax, but they actually work differently. With an estate tax, the estate itself pays the tax before heirs receive anything. With an inheritance tax, the beneficiary pays the tax after they receive assets. Inheritance taxes also only exist at the state level, not federally.

Maryland stands out because it is currently the only state that charges both an estate tax and an inheritance tax. Inheritance taxes also vary based on who receives the inheritance. Some states charge higher rates to more distant relatives or non-relatives. Furthermore, five states currently impose inheritance taxes: Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania, with Iowa phasing out its inheritance tax by 2025 completion)3.

Current Estate Tax Rates and Brackets

The estate tax rate works on a progressive bracket system. The federal estate tax starts at 18% and increases as the taxable estate grows, reaching a top rate of 40%. That does not mean the entire estate gets taxed at 40%. Instead, the graduated rates apply only to the taxable portion left after deductions and the exemption amount are applied.

The IRS also clarifies that the 40% rate applies once the taxable estate exceeds the exemption by more than $1 million. For most families, the federal exemption removes estate taxes entirely. For high-net-worth families, the brackets matter because even a small portion of an estate above the exemption can trigger a large tax bill.

2026 Estate Tax Exemption Thresholds

In 2026, the federal government will allow many high-net-worth families to transfer significant wealth without paying federal estate taxes. Still, your exemption amount depends on how you structure your plan, what you give away during life, and where you live.

Federal Exemption Amounts

The estate tax exemption sets the amount you can transfer before federal estate taxes apply. For 2026, the individual exemption sits at $15 million, and married couples can protect up to $30 million with proper planning.

You can also reduce your taxable estate by using the annual gift tax exclusion. In 2026, you can gift $19,000 per recipient each year without using any of your lifetime exemption. This gives families a steady way to move wealth out of an estate over time, especially when parents or guardians want to give money to children, grandchildren, or other heirs.

Portability plays a significant role in planning, too. Portability allows a surviving spouse to use a deceased spouse’s unused exemption. That means couples who plan correctly can preserve the full $30 million exemption, even if one spouse dies first.

The 2026 Sunset Provision: What HNWIs Must Know

For years, estate planning discussions focused on the “sunset” of the Tax Cuts and Jobs Act (TCJA). TCJA was scheduled to expire at the end of 2025, which would have reduced the federal government's revenue in 2026.

Instead, the OBBBA permanently raised the exemption to $15 million per person beginning January 1st, 2026. That change removed the immediate concern that the exemption would fall to around $7 million. It also gave more stability to long-term planning for high-net-worth individuals.

Still, estate planning works best when you plan ahead. “Permanent” does not mean untouchable, as Congress can always change the tax laws again. When you use today’s exemption through gifting and trust planning, you can move future growth out of your estate. Starting in 2027, the $15 million base is also set to increase each year through inflation indexing.

State Estate Tax Considerations

Even if you stay under the federal exemption, you could still face estate taxes at the state level. Currently, 12 states and the District of Columbia impose their own estate tax rules, and many of them set exemption limits far lower than the federal $15 million threshold.

For example, Oregon’s estate tax exemption sits at $1 million, and Massachusetts uses a $2 million exemption. That means a family with a net value of $5 million or $10 million might owe state estate tax even though they owe no federal estate tax.

Some states also create extra risk through “cliff tax” rules. New York is the best-known example. If your estate exceeds the exemption by more than a small amount, the state can tax the entire estate rather than only the excess. That creates a sharp jump in taxes and can surprise families who only planned around the federal exemption.

Visual: Bar Chart. A bar chart comparing the Federal exemption ($15M) against various state-level exemptions (e.g., OR at $1M, MA at $2M, NY at $7.35M).

Strategic Estate Tax Planning Approaches

Even with a high federal exemption in 2026, estate tax planning is still essential. The proper approach can reduce what your heirs pay, keep more wealth in the family, and give you more control over how assets transfer. Most strategies fall into a few categories: gifting, trusts, charitable planning, and business planning.

Gifting Strategies During Your Lifetime

Lifetime gifting gives you a direct way to reduce future estate taxes. When you gift assets during your lifetime, you move them out of your estate. That matters most when those assets are likely to grow. If you gift them now, the future appreciation happens outside your taxable estate.

You can start with the annual gift exclusion. In 2026, you can gift up to $19,000 per recipient each year without using your lifetime exemption. This works well when you want to make consistent gifts to children, grandchildren, or other family members.

Some families also make larger gifts that use part of the lifetime exemption. This approach can “lock in” today’s asset values and remove future growth from the estate. It also works well when asset values dip, and you want to transfer wealth at a lower valuation.

Trust Structures for Estate Tax Efficiency

Trusts can be an essential factor in estate planning because they give you control over how and when assets pass to others. Many trust strategies also reduce estate taxes when appropriately used.

A Spousal Lifetime Access Trust (SLAT) allows one spouse to transfer assets into an irrevocable trust for the benefit of the other spouse (and often children). This can reduce the taxable estate while still keeping indirect access to the assets through the spouse.

A Grantor Retained Annuity Trust (GRAT) works well for high-growth assets. You place assets into the trust and receive annuity payments for a set term. If the assets grow faster than expected, the extra growth passes to heirs with little to no gift tax cost.

An Irrevocable Life Insurance Trust (ILIT) removes life insurance proceeds from the taxable estate. Without an ILIT, a sizable death benefit can push an estate above the exemption and increase estate taxes.

For families planning for multiple generations, a Dynasty Trust can preserve wealth over time. This structure can reduce or avoid transfer taxes across generations when structured around the Generation-Skipping Transfer (GST) exemption.

Charitable Planning Techniques

Charitable giving can reduce estate taxes while allowing you to direct part of your wealth to causes you care about. The structure you choose determines whether you receive income, when the charity receives funds, and how the transfer impacts your estate.

A Charitable Remainder Trust (CRT) provides income to you (or another beneficiary) for a set number of years or for life. After that, the remaining assets go to charity. This can reduce the value of your taxable estate while creating predictable cash flow.

A Charitable Lead Trust (CLT) works in the opposite direction. The charity receives income first for a period of time. Then the remaining assets pass to heirs, often at a reduced gift tax value.

A Donor-Advised Fund (DAF) offers a simpler option. You contribute assets, take an immediate income tax deduction, and remove those assets from your estate. Then you recommend grants to charities over time.

Business Succession and Valuation Discounts

If you own a business, estate planning becomes a bit more involved because business value often makes up a large share of your net worth. Without planning, heirs might need to sell part of the business just to cover taxes or expenses.

A Family Limited Partnership (FLP) can help you transfer business interests while keeping control. In many cases, parents keep management authority while gradually gifting limited partnership interests to heirs.

Business owners can also use valuation discounts. When you gift a minority interest in a private business, that interest could qualify for discounts related to lack of marketability or lack of control. This lets you transfer more ownership while using less of your exemption.

Buy-sell agreements are vital as well. These agreements set rules for what happens if an owner dies, becomes disabled, or wants to exit. They can also create a plan for liquidity, so heirs don’t need to sell assets quickly or accept unfavorable terms.

Estate Tax Mistakes to Avoid

Estate planning often goes wrong for one reason: people assume the rules are simple. In reality, estate taxes can show up in unexpected places, particularly at the state level. Minor oversights can also create large tax bills or leave heirs with extra work during an already difficult time.

Overlooking State-Level Exposure

Many families focus only on federal estate taxes. That makes sense at first glance because the federal exemption rises to $15 million per person in 2026. However, state estate taxes can still apply at much lower levels. A $10 million estate may sit below the federal limit, yet still trigger a state estate tax bill in places like Illinois or Maryland.

State rates can also climb quickly. Washington State is one of the strongest examples because it has the highest estate tax rate in the country, topping out at 20% on taxable estates above certain thresholds, which can reduce what heirs receive even when the estate remains below the federal exemption4.

If you live in a state with an estate tax, you need a plan that addresses the state’s rules, not just federal rules.

Failing to Update Plans After Life Changes

Estate planning is not a one-time task. Your plan should change as your life changes. Marriage, divorce, a new child, a business sale, or a significant life move can all impact how your estate planning should work.

Even if nothing dramatic happens, your asset values can change over time. A plan that worked well when your net worth sat at $8 million might no longer fit when your investments grow or when real estate values rise. Valid documents could also fall behind current tax law. Older plans may not take full advantage of the current exemption amounts, particularly with the 2026 changes.

A regular review also gives you a chance to adjust your tax strategy. For example, you might want to shift which assets you pass at death to take advantage of the step-up in basis, rather than gifting those assets during your lifetime.

Procrastinating on Irrevocable Decisions

Some of the most effective estate strategies take time. You can’t set up detailed trust structures or business transfers overnight. A SLAT, GRAT, or valuation-based gifting strategy typically requires coordination between multiple professionals, including an estate attorney, Certified Public Accountant (CPA), and valuation expert.

Timing is also crucial because markets move. When you wait, you could miss the chance of gift assets while values remain lower. That can reduce how much wealth you can transfer under your exemption.

The IRA also expects support for the value of private assets. Business interests, private equity holdings, and real estate often require formal appraisals. Those appraisals must be definable and well-documented, and that process takes time. If you rush it, you increase the chance of problems later.

How a Fiduciary Financial Advisor Enhances Estate Planning

Estate planning often involves more than a will or a trust. It connects to your investments, taxes, insurance, retirement accounts, and long-term goals. A fiduciary financial advisor can guide the entire picture and keep your plan working as your wealth grows and your life changes.

Coordinating Estate Planning with Comprehensive Wealth Management

A fiduciary advisor can serve as the “quarterback” of your planning. They look at how your estate plan and your financial plan work together rather than separately. That matters because your estate plan can fall apart if your investment strategy, beneficiary designations, or insurance coverage do not match your intent.

A fiduciary advisor also helps with liquidity planning. Even wealthy families can face cash-flow problems when a large portion of the estate sits in real estate, business ownership, or long-term investments. An advisor can plan for accessible funds, structured insurance or other resources so your heirs can cover taxes and expenses without selling assets quickly.

They also coordinate with your CPA and estate attorney. Teamwork makes it easier to time gifts, manage taxable income, and build a plan that transfers wealth with fewer taxes over time.

Technology-Enabled Visibility Into Your Full Financial Picture

Modern estate planning works better when you see your full net worth in one place. Many fiduciary advisors use wealth dashboards that track accounts, investments, liabilities, and asset values in real time. This lets you monitor your net worth against both federal and state exemption thresholds as markets change.

Technology also ensures you plan better gifting. A clear view of your holdings makes it easier to identify high-basis versus low-basis assets, so you can decide which assets make more sense to gift during life and which assets make more sense to pass at death.

Many firms also offer a secure digital value. This allows you to store essential estate documents, insurance policies, account details, and instructions in one protected place. When the time comes, your heirs and professional partners can access what they need without any holdups or confusion.

Plan Now to Protect Your Legacy in 2026

Estate taxes might not impact every family, but they can significantly reduce what heirs receive when planning falls behind current law. In 2026, high exemption limits create a valuable window for many high-net-worth individuals, but state estate taxes, asset growth, and future tax changes can still affect outcomes. A clear estate plan gives you control, reduces taxes where possible, and makes the transfer of wealth easier for the people you care about most.

Next Steps:

- Estimate your current net worth and project how it might grow over the next 10-15 years.

- Review your estate plan documents and beneficiary designations for gaps or outdated provisions.

- Check whether your state imposes an estate tax and what exemption applies.

- Identify assets that could work well for gifting, trust funding, or charitable planning.

- Meet with a fiduciary advisor, CPA, and estate attorney to build a coordinated plan.

Connect with a Savvy Advisor Today!

Frequently Asked Questions

How much can you inherit without paying estate tax?

At the federal level, heirs can receive assets without estate tax as long as the total estate value stays below the federal exemption, which rises to $15 million per person in 2026. If the estate exceeds that amount, only the portion above the exemption may be taxed. State estate taxes are different and often apply at much lower levels, so some heirs may still face state taxes even when no federal tax is owed.

What is the estate tax rate?

The federal estate tax uses a graduated rate system, starting at lower rates and topping out at 40% on the taxable portion of an estate. The highest rate does not apply to the entire estate—only to the amount that exceeds deductions and the exemption. State estate tax rates vary and can add another layer of tax exposure.

What's the difference between estate tax and inheritance tax?

An estate tax is paid by the estate before assets are passed to heirs, while an inheritance tax is paid by the person who receives the assets. Estate taxes can exist at both the federal and state levels. Inheritance taxes only exist at the state level and often depend on the heir’s relationship to the person who passed away.

Works Cited

- Instructions for Form 706

- Tax-Exempt Bonds: A Description of State and Local Government Debt

- Estate and Inheritance Taxes by State, 2025

- Estate Tax

Chris Benda is the Founder of Benda & Co., where he helps clients who have done everything right financially but are seeking clarity on what comes next. His approach combines strategic planning with a deep understanding of each client’s goals, helping them align their wealth with a more intentional and fulfilling life.

Chris Benda is an investment adviser representative with Savvy Advisors, Inc. (“Savvy Advisors”). Savvy Advisors is an SEC registered investment advisor. The views and opinions expressed herein are those of the speakers and authors and do not necessarily reflect the views or positions of Savvy Advisors. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy.

Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.Savvy Wealth Inc. is a technology company. Savvy Advisors, Inc. is an SEC registered investment advisor. For purposes of this article, Savvy Wealth and Savvy Advisors together are referred to as “Savvy”. All advisory services are offered through Savvy Advisors, while technology is offered through Savvy Wealth. The views and opinions expressed herein are those of the speakers and authors, and do not necessarily reflect the views or positions of Savvy Advisors.