Lack of Data Makes The Fed’s Job Harder: But There Is No Doubt That The Economy Is Slowing

For the week (ended November 14), the major indexes were basically flat (see table), continuing the weakness seen so far in November. The exception was the small cap Russell 2000 as it continued its retreat from its late October peak, with the tech-heavy Nasdaq not far behind.

Three of the Magnificent 7 were winners (NVDA, MSFT, AAPL) while the other four (AMZN, META, TSLA, GOOG) lost ground last week. It is noteworthy that five of the Magnificent 7 peaked in the October 28th to November 11th period. (TSLA peaked last December, META last August). From recent market behavior, new record highs are unlikely in the near term.

Despite the end of the shutdown, it is likely to be at least January, when we get December’s data, for us to have a solid picture of the U.S. economy. We note that BLS has lost 25% of its staff and a third of its leadership positions are vacant.1 BLS announced that the September jobs report will be published on Thursday, November 20, and, according to the White House, the October inflation and jobs report may never be released (or even calculated).

The Fed

As a result, the Fed will have much less information to mull at its December 9-10 meetings, and the market odds of an interest rate reduction now sit in the 50% range.2 A month ago, such odds were 95%. In fact, this week, two Fed voting members issued hawkish remarks. Atlanta Fed President Raphael Bostic indicated that it was his preference to continue to focus on the Fed’s inflation mandate over its employment one. While progress on inflation has breached the 3% level to the downside, its progress toward the magic 2% goal has slowed.

Susan Collins, another voting FOMC member, also uttered somewhat hawkish rhetoric, indicating that, while she voted to cut in September, the bar remains “relatively high” for further cuts, as she believes more time is needed for risks to come back into balance (translation: inflation needs to move lower). Our view is that inflation is a lagging indicator, and that weakness in the labor market is concerning. Lowering rates appears to be the obvious move, but, as Chairman Powell said at his last press conference, “that’s not a foregone conclusion – far from it!”

The Slowing Economy

Despite the lack of labor market data emanating from the federal government, there are still private sector firms that measure labor market conditions, specifically ADP and Challenger, Gray & Christmas.

- The ADP employment release indicated that the private sector lost more than -11,000 jobs per week in October.

- Challenger, Gray and Christmas indicated that October job cuts, at 153K+, were up 183% from September, and +175% from September ’24.3

- We fully expect that, when the next unemployment statistics are released, that we will see a rise in the unemployment rate, likely to 4.5% – the latest report for August was 4.3%.

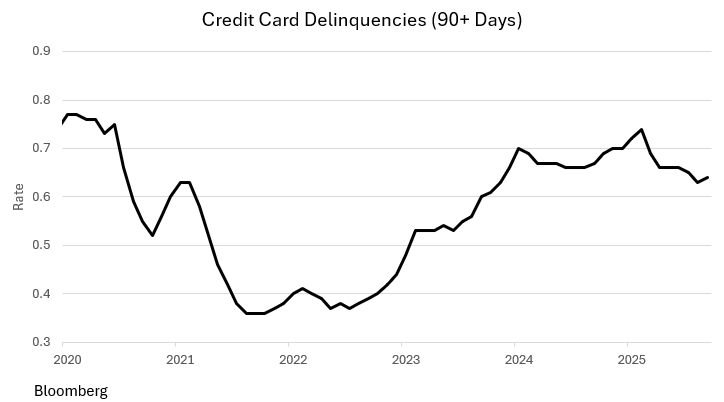

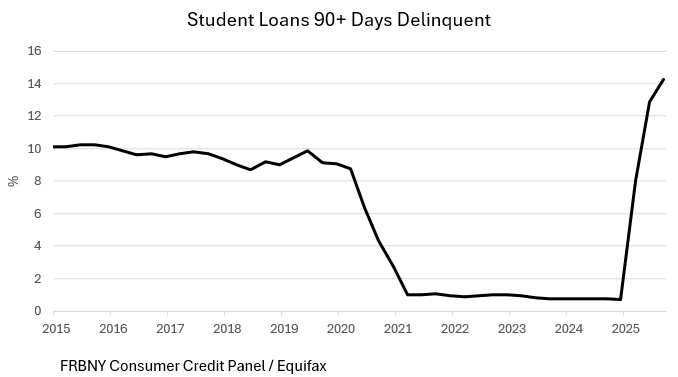

- Unpaid credit card balances are sitting at record highs, both in the aggregate and per capita. Newly delinquent loans (30+ days past due) were higher last quarter, now at 5.33% of outstanding balances, the highest level since 2014. In addition, new seriously delinquent loans (late for 3+ months) now sit at a 12-year high. 12% of credit card balances are 3+ months late, as are 10% of student loans.

- 5% of outstanding auto loan balances are 90+ days past due, up from 4.6% a year ago and 3.9% in 2023. We have not seen a number this high since 2011.

- Unpaid credit card balances sit a record highs, at $4,200 per capita. Newly delinquent loans (30+ days past due) moved higher in Q3, rising to 5.33% from 5.26% in Q2, now at the highest level since 2014, and new seriously delinquent loan balances (late for 3+ months) inched up to a near 12-year high.

- Student loans, the collection of which had been on hold during the Biden Administration, now show a delinquency of 14%.

- Based on this data, it is our view that the odds of a Recession are now quite high.

The Consumer

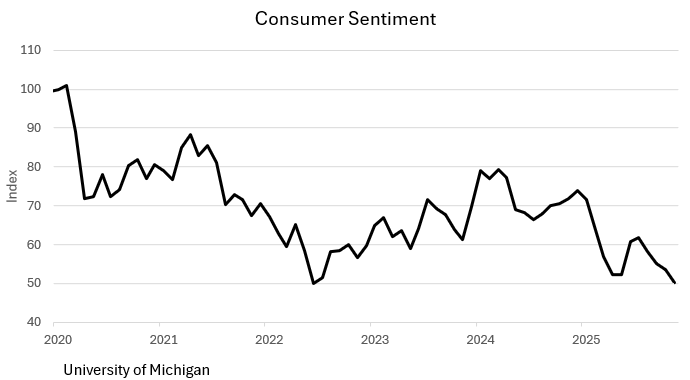

One can tell from the delinquencies noted above that the consumer is hurting. The University of Michigan’s Consumer Sentiment Index, at 50.3 in November (vs. 53.6 in October) was the 2nd lowest reading in the history of the series (back to the early 1950s) – the low being November ’22. The Current Conditions Index fell to 52.3 in November from 58.6 in October. The consensus estimate was 59.2 – so a huge miss. The fear of losing one’s job over the next five years in the University of Michigan’s poll was nearly 23%, and in NY, the fear of losing one’s job in the next year rose to nearly 43%!

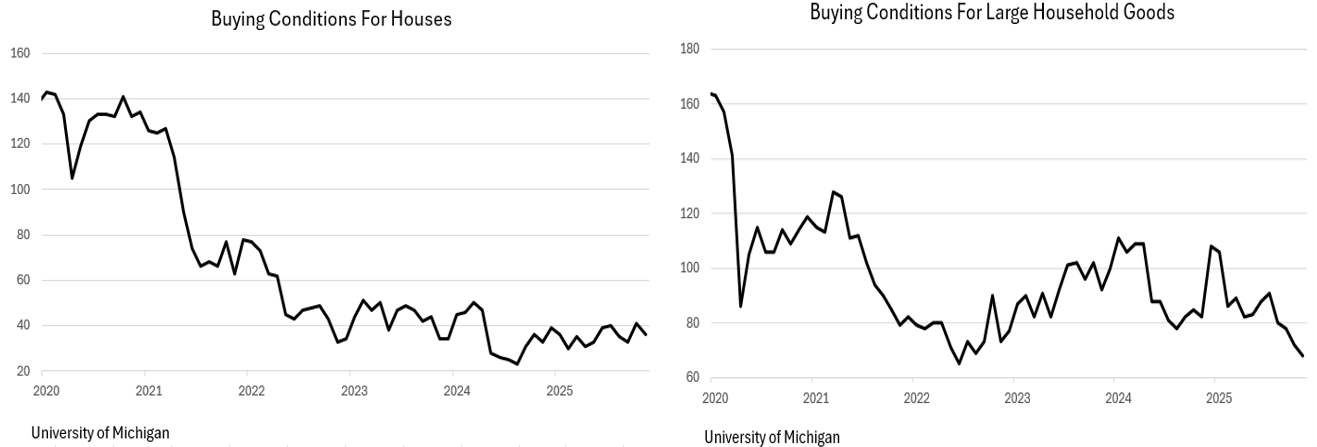

It isn’t any wonder, then, why the housing industry is back on its heels. The charts show that

buying conditions for houses are plugging along at a low level as are buying conditions for large household goods.

With Consumption representing 70% of GDP, it seems obvious that Q4 GDP growth will be slight, and, if conditions continue as they are, Q1’s GDP growth could conceivably show up with a negative sign.

Final Thoughts

Financial markets, having risen significantly over the last two years (S&P 500: +23% in ’24; +14% ytd in ’25), appear to be pausing; perhaps waiting for AI profits to materialize (which may take several years).

The government shutdown will delay inflation and jobs numbers; the White House suggests that those numbers for October may not even be calculated.

As a result, the Fed will have little new information on which to make its rate decision at its December 9-10 conclave. And while inflation appears to be sticky at the 3% level, given a weakening labor market, the Fed should lower rates (by at least 25 basis points although our reading is that 50 basis points makes more sense.)

Dr. Robert Barone, Ph.D. is an economist whose storied career spans numerous decades and positions within the world of finance. Since gaining his Ph.D. in Economics from Georgetown, he has been a Professor of Finance (University of Nevada), a community bank CEO (Comstock Bancorp), and a Director of the Federal Home Loan Bank of San Francisco, where he served as its Chair in 2004. He lives and breathes the world of finance, continuing to provide clients and avid Forbes readers with his latest market insights.

(Joshua Barone and Eugene Hoover contributed to this blog.)

Robert Barone, Joshua Barone and Eugene Hoover are investment adviser representatives with Savvy Advisors, Inc. (“Savvy Advisors”). Savvy Advisors is an SEC registered investment advisor. Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Ancora West Advisors, LLC dba Universal Value Advisors (“UVA”) is an investment advisor firm registered with the Securities and Exchange Commission. Savvy Advisors, Inc. (“Savvy Advisors”) is also an investment advisor firm registered with the SEC. UVA and Savvy are not affiliated or related.

Reference:

1 https://www.markets.com/news/economic-data-black-hole-us-shutdown-2226-en

2 https://ca.finance.yahoo.com/news/odds-december-fomc-rate-cut-145607856.html?

3 https://www.challengergray.com/blog/october-challenger-report-153074-job-cuts-on-cost-cutting-ai/