The Fed Moves to Easier Money as Inflation Falls; Who Will Be Its Next Chair?

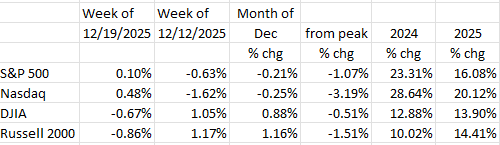

Markets treaded water for the week ending December 19th with the S&P 500 and the Nasdaq slightly in the green while the DJIA and Russell 2000 were marginally red. It is a similar story for the month but with roles reversed: the S&P 500 and Nasdaq were down slightly while both the DJIA and the Russell were up near 1% as of the close on Friday. As we approach year’s end, a look at the table reveals that the DJIA and the Russell, year to date, are beating their 2024 double digit returns while the S&P and Nasdaq, while both showing significant growth, look like they will end 2025 slightly shy of 2024’s advances.

The Job Market

BLS released the long-awaited October and November payroll data on Tuesday, December 16th. The data showed that October payrolls fell -105K, much of which was from forced federal government civil service retirements. Official November payrolls were positive (+64K).1 Given that the birth/death automatic add-on is over +90K, we are looking at a real number of -195K for October and -26K for November. As a result, the U3 Unemployment Rate rose to 4.6%.2 (Note: the most recent (December) forecast from the Fed pegs the U3 unemployment rate at 4.5% for 2026; so, this forecast is already in a hole, even before the new year begins!!) This 4.6% rate is the highest since September ’21. Worse, the U6 Unemployment Rate, which counts the underemployed, rose to 8.7%, the highest level since August ’21!3 That U6 number was 8.0% in September, so quite the run-up showing rapid deterioration in the job market. Full-time jobs have been disappearing, falling by nearly -1 million (-983K) in November’s count.1 Additionally, weakness was evident in those working “part-time for economic reasons” (wanting full-time employment but unable to find such). That category rose by +909K to the highest reading since March ’21. Other signs of weakness in the job market include a rapid rise in self-employment (+526K), which always rises when the job market becomes tight, and a significant increase in those holding more than one job (+499K).1

The most important takeaway from all this is that the labor market deterioration is rapid.

The Fed and Monetary Policy

Last Wednesday, the Fed lowered rates by a quarter of a percentage point (25 basis points in financial jargon). The Federal Funds Rate, the rate that banks pay when they borrow from the Fed, now stands in a range at 3.50%-3.75%. That rate cut was expected by the markets.

What wasn’t expected was the significant differences of opinion among the Federal Open Market Committee members. There are 19 of them, but at any given time, only 12 vote.

Of the 12 voters, 9 voted for the cut – so there were three dissenters. Three dissents are very very unusual. Two of the three wanted no rate cut at all, while one of them (Stephen Miran) wanted a half-point cut (i.e., 50 basis points). If we count the opinions of the non-voters, then there were 7 dissenters – that’s a very significant 37% of the FOMC that disagreed with the rate cut!! I think I can say that we haven’t seen such a difference in economic views at the Fed in modern times.

It is also clear that the Fed has switched its emphasis from the inflation mandate to the employment mandate. And that means that they will continue to ease policy if the unemployment rate continues to rise.

In addition, and what wasn’t covered by the media, the Fed announced that they have stopped selling bonds from their portfolio (called Quantitative Tightening of QT) and will be buying $40 billion of short-term Treasury securities per month (called Quantitative Easing or QE). Those purchases, combined with the rate-reduction, are a signal of a new regime of monetary policy easing. So, while markets and the Fed’s own FOMC see only one or two more rate reductions in 2026, the reintroduction of Treasury bond purchases signals that monetary policy will be on the “easy side” for the foreseeable future.

The Chairmanship Issue

One other dilemma facing the Fed is the identity of the next Chairman, as Powell’s term as Chair expires in May 2026, but his term as an FOMC member doesn’t expire until January 2028. Markets believe that President Trump is considering one of the two “Kevins” (Hassett or Warsh) as the next Chair. Christopher Waller, currently an FOMC member, is also considered to have an outside chance. Normally, the sitting chair (Powell) would resign from the board to make room for the new Chair if that person were an outsider (like the two Kevins). In the press conference accompanying the December FOMC meeting, Powell was asked if he planned to finish out his FOMC term (expiring January ’28). He said he planned to remain on the FOMC. That leaves President Trump with two possibilities: 1) If his “firing” of FOMC member Lisa Cook is upheld by the Supreme Court (which hears the case in January), he can appoint someone from the outside to fill that post and anoint that person as the next Chair, or 2) his recent appointment, Stephen Miran, stepped in to an FOMC post (vacated by Adrianna Kugler) whose term expires in January (2026). It is possible that Trump could use Miran’s FOMC slot for his choice for Chair and reappoint Miran when the next FOMC opening occurs (Powell’s term expiring in January 2028 or Lisa Cook’s position if Trump’s position is upheld by the Supreme Court). Given the circumstances, and the fact that the Lisa Cook situation may not be decided by the court prior to Powell’s term as chair expiring in May, it appears that the second possibility (use Miran’s position) is the most realistic. Stay tuned.

Inflation

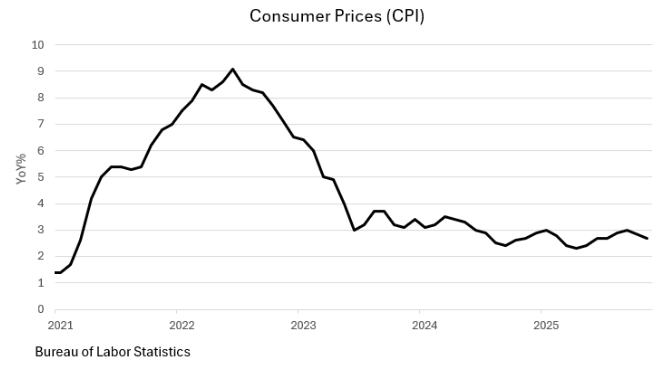

The long-awaited CPI report was released by the Bureau of Labor Statistics (BLS) on Thursday, December 18th. The official release indicated that Headline CPI rose +0.2% from September to November. That’s a two-month interval as October’s data was never collected. According to the release, the CPI was up 2.7% from a year ago.4 That’s down from 3.0% in September and handily beat the consensus estimate of a rise of 3.1% from a year earlier. The “core” measure (excludes food and energy) rose 2.6% from a year earlier, and is the slowest rise in four years, i.e., since 2021!! The Headline three-month trend rate came in at a 2.1% annual rate, while the core three-month trend fell to 1.6%. While the markets rejoiced, this was something we predicted would happen last Spring, as the heavily weighted but significantly lagged fall-off in the heavily weighted rents input to the index has now come to bear. It appears that the trend toward lower inflation is baked in, and that means that we will likely see easier monetary policy in 2026 than what is currently in the market, especially since the jobs market appears to be deteriorating.

Final Thoughts

The unemployment rate is rising. U3, at 4.6%, is the highest it has been since September ’21. At the same time, the U6 measure (8.7%) has hit its highest level since August of that year. That U6 number is up big-time from its 8.0% level in September. Worse, full-time jobs fell nearly -1 million in November and those working part-time for economic reasons (unable to find full-time positions) rose by over +900K to the highest reading since March ’21. Clearly the labor market is rapidly deteriorating.

As expected, the Fed cut rates 25 basis points at its December 10th meeting, with 9 of the 12 voting FOMC members casting ‘yes’ votes. Three dissenting votes is quite unusual and if we counted all 19 FOMC members, there were seven dissenters, quite an unusually large difference of opinion on the state of the economy. Also of note is the switch of emphasis in the FOMC statement from the inflation mandate to the employment one. Given the emerging weakness in the job market, we see more rate cuts coming in 2026. The fact that they’ve begun a small Quantitative Easing (QE) program ($40 billion/month) is a strong clue as to the ongoing stance of monetary policy.

Powell’s term as Chair expires in May; his term on the FOMC doesn’t expire until January ’28. While it is usual and customary for the outgoing chair to resign from the Board to make way for a new Chair, Powell said he will finish his term. In the hunt for the Chairmanship are the two Kevins. If Trump picks one of them, there will have to be an open seat. Miran’s term expires in January, and the other possibility is the Lisa Cook position, and that depends on a Supreme Court decision as to Trump’s ability to ‘fire’ her.

There was good news on the inflation front in November. As we forecast several months ago, the headline CPI fell below 3% to a 2.7% rate on a year/year basis in November. That number was 3.0% in September. That 2.7% number handily beat the consensus estimate of 3.1%, and this implies that inflation, going forward, will be less of a problem. The “core” CPI reading on a year/year basis fell to 2.6%. Better yet, the three-month trend in the core headline index was the slowest in four years at 2.6%. Even better, the headline three-month trend fell to a 2.1% annual rate, while that same measure for the core index fell to 1.6%.

Dr. Robert Barone, Ph.D. is an economist whose storied career spans numerous decades and positions within the world of finance. Since gaining his Ph.D. in Economics from Georgetown, he has been a Professor of Finance (University of Nevada), a community bank CEO (Comstock Bancorp), and a Director of the Federal Home Loan Bank of San Francisco, where he served as its Chair in 2004. He lives and breathes the world of finance, continuing to provide clients and avid Forbes readers with his latest market insights.

(Joshua Barone and Eugene Hoover contributed to this blog.)

Robert Barone, Joshua Barone and Eugene Hoover are investment adviser representatives with Savvy Advisors, Inc. (“Savvy Advisors”). Savvy Advisors is an SEC registered investment advisor. Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Ancora West Advisors, LLC dba Universal Value Advisors (“UVA”) is an investment advisor firm registered with the Securities and Exchange Commission. Savvy Advisors, Inc. (“Savvy Advisors”) is also an investment advisor firm registered with the SEC. UVA and Savvy are not affiliated or related.

Resources

1 https://www.bls.gov/news.release/empsit.nr0.htm

2 https://www.nytimes.com/live/2025/12/16/business/jobs-report-economy