The Modern Guide to Minor Accounts: Comparing 529s, Roth IRAs, UTMAs, and the New Trump Account

Choosing the proper investment accounts for kids is one of the most consequential decisions a parent can make, yet the sheer variety of options often leads to analysis paralysis. For decades, families were stuck choosing between the rigid structure of a college fund or the lack of control found in a traditional custodial account.

Today, it’s different. With new legislation expanding how we save and transfer wealth, parents must now navigate an intricate web of tax benefits and long-term legacy goals to ensure their children enter adulthood on a firm financial footing.

For most families in 2026, the optimal strategy is to stack a 530A Trump Account (for early tax-deferred growth), a 529 plan (for education), and a custodial Roth IRA (once the child has earned income), while keeping a parent-owned taxable account as the flexible backstop.

Speak with an Education Planning Professional

Key Takeaways

Below, we’ll cover how:

- Modern legacy planning involves stacking different accounts to balance education, retirement, and flexible spending.

- The 530A Trump Account and SECURE 2.0 529 rollovers have fundamentally changed the overfunding risk of minor accounts.

- Understanding the 2026 Kiddie Tax thresholds is essential to avoid unexpected tax hits on unearned income.

- Choosing between student-owned and parent-owned assets can significantly impact your child’s future financial aid eligibility.

- For some families, prioritizing savings in a parent-owned taxable account provides greater control and flexibility than directing every dollar into child-specific vehicles.

Understanding the Landscape of Minor Investment Accounts

A custodial account is a financial vehicle managed by an adult for the benefit of a minor, who legally owns the assets. Custodial accounts such as UTMAs and UGMAs generally involve irrevocable gifts to the child, while 529 plans typically allow the account owner to retain control.

In the past, families typically chose between basic savings or simple brokerage accounts that offered little in the way of tax strategy. However, the financial landscape has shifted toward sophisticated, tax-advantaged vehicles. Today’s options let parents target specific goals (i.e., tuition, retirement, or general wealth building) while shielding growth from the heavy hand of the IRS.

The 529 College Savings Plan: More than Just a Tuition Fund

The 529 plan remains the gold standard for education-specific savings. However, its utility has expanded far beyond traditional four-year universities. Recent legislative changes have added layers of flexibility, making it a powerful tool for various career paths.

Tax Advantages and Qualified Expenses

The main draw of a 529 college savings plan is its triple tax advantage: contributions grow tax-deferred, and withdrawals are entirely tax-exempt when used for qualified education costs. Beyond the tax savings, these accounts offer a major perk for financial aid planning. Parent-owned 529s are assessed at a maximum rate of 5.64% in the FAFSA formula, which is far more favorable than the 20% rates applied to student-owned assets.

Furthermore, the definition of qualified expenses is surprisingly broad. You can use funds for vocational schools, registered apprenticeships, and even up to $10,000 per year for K-12 private school tuition, ensuring 529 plan benefits apply to almost any educational journey.

Beyond federal benefits, some states offer their own income tax deductions or credits for contributions to an in-state 529 plan, which can provide an immediate return on your savings in the year the contribution is made. Check your state's plan or speak with a tax advisor to understand what is available where you live.

The 529-to-Roth IRA Rollover: Solving the Overfunding Dilemma

Many families worry about saving too much in a 529 college savings plan. A child may earn scholarships, skip college, or spend less than expected. In the past, unused funds could create taxes or penalties. SECURE 2.0 added a new option.

Eligible beneficiaries can move up to $35,000 from a 529 plan into a Roth IRA over time. The 529 account must be open for at least 15 years. Contributions and associated earnings made within the prior five years are generally ineligible for rollover. Yearly rollovers must stay within the annual Roth IRA contribution limit, which is $7,500 in 2026. The beneficiary also needs earned income.

This rule gives families more flexibility. Unused college savings can now help start a child’s retirement savings instead.

The Custodial Roth IRA: A Head Start on Tax-Free Retirement

A Roth IRA for minors is perhaps the most powerful tool for long-term wealth because it harnesses time in a way adult accounts can’t. By starting a retirement fund in childhood, you give your child a multi-decade head start on tax-free growth.

The Earned Income Requirement for Minors

To open a custodial Roth IRA, a child needs to have legitimate earned income. This means they must receive taxable compensation, like W-2 wages from a part-time job or 1099 income from self-employment. The IRS is strict; you cannot contribute more than the child actually earned that year.

For instance, if your teenager earns $4,000 as a lifeguard, their total contribution is capped at $4,000, even though the 2026 federal limit is $7,500. Common ways for minors to meet this requirement include summer jobs, professional modeling, or small businesses such as lawn care or babysitting, provided the income is documented and reported.

The Long-Term Growth Potential of a Minor Roth IRA

The true potential magic of this account lies in the compounding interest that occurs over fifty or sixty years. A few thousand dollars invested during high school can potentially grow into a six-figure sum by retirement without ever being taxed again. Unlike many other vehicles, Roth IRA withdrawal rules are exceptionally flexible regarding the principal.

Contributions are made with after-tax dollars, so the original seed money can be withdrawn at any time, for any reason, without taxes or penalties. This provides a built-in safety net for future needs, like a home down payment or emergency expenses. Because this account remains in the child’s name and is not tied to a specific school, parents don’t have to worry about the overfunding issues associated with education-only plans.

The New Trump Account (530A IRA): A Revolution in Long-Term Saving

The introduction of the 530A, also known as the Trump Account, represents one of the most significant shifts in generational wealth planning in decades. This account bridges the gap for families who want to start a retirement-style fund for their children without waiting for them to get a job.

How the 530A IRA Bridges the Gap for Families

The 530A is a game-changer because it removes the earned income barrier that prevents many children from opening a Roth IRA. Parents, grandparents, or even employers can contribute to this tax-advantaged account regardless of whether the minor has a paycheck. Current proposals contemplate limiting investments primarily to diversified index-style investments designed for long-term growth.

This prevents speculative trading and focuses on long-term market participation. The accounts are intended for long-term saving during childhood, with many traditional IRA rules applying after the beneficiary reaches adulthood. . “Trump Accounts are structured as traditional IRAs with special rules that apply during the beneficiary’s childhood years. .

Eligibility, Contribution Limits, and the Federal Seed Money Pilot

For 2026, the annual contribution limit for a Trump Account is $5,000, including a maximum of $2,500 from an employer as a pre-tax benefit. Perhaps the most talked-about feature is the Federal Seed Money Pilot. The legislation also created a pilot program that may provide a one-time $1,000 federal contribution for certain eligible children born between 2025 and 2028, subject to IRS implementation rules.

While individual contributions are made with after-tax dollars, meaning they don’t provide an immediate tax deduction, the account grows tax-deferred. This means no taxes are due on dividends or capital gains until the money is eventually withdrawn in adulthood, potentially providing a massive tailwind for a child’s future financial security.

Custodial Accounts: Navigating the UTMA vs. UGMA Debate

While newer accounts like the 530A are making headlines, traditional custodial accounts remain a staple for families who want to gift assets without the strictures of a trust. These accounts provide a simple way to move wealth to the next generation, but choosing the wrong flavor can limit your investment options.

Why UGMA is Fading While UTMA Remains the Standard for Tangible Assets

The Uniform Gifts to Minors Act (UGMA) was once the primary tool for parents, but its limitations have caused it to fall out of favor. UGMA accounts are limited to financial assets, such as cash, stocks, and bonds, and typically transfer to the child’s control at age 18.

In contrast, UTMA vs. UGMA comparisons favor the Uniform Transfers to Minors Act (UTMA) because it allows for the investment of tangible assets, including real estate, fine art, and even intellectual property.

Furthermore, UTMA often lets a donor delay the transfer of control until age 21 or 25, depending on state law. Today, only a few states, like South Carolina and Vermont, still primarily support UGMA as the default, making UTMA the modern standard for families seeking broader investment flexibility.

The Age of Majority and the Risk of Irrevocable Gifting

With both account types, your child gains complete legal control once they reach the age of majority. This is a critical point for parents to understand: these transfers are irrevocable. Unlike a 529 plan, where you can change the beneficiary, money placed in a custodial account belongs to the child permanently.

You cannot take the funds back if your child decides to use the money for a purpose you don’t approve of, such as a sports car instead of a house deposit. Once the age limit is reached, usually 18 to 21, your child can withdraw and spend the funds without any restriction from the original donor. This lack of control is the price parents pay for the simplicity and flexibility these accounts offer.

Account Comparison at a Glance

Comparison Guide: Taxation, FAFSA, and Strategy

Choosing the proper account requires understanding how these vehicles interact with the IRS and the Department of Education. Balancing immediate tax hits against future financial aid eligibility is the key to a successful long-term strategy.

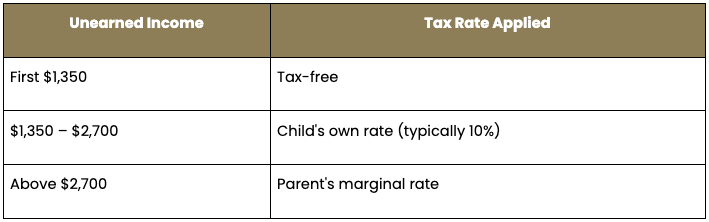

Taxation and the 2026 Kiddie Tax Thresholds

The Kiddie Tax sets limits on how much unearned income a child can receive before higher tax rates apply. Any unearned income above the threshold is taxed at the parent’s marginal tax rate to prevent families from shifting large investment gains into a child’s lower tax bracket.

For the 2026 tax year, the thresholds have been adjusted: the first $1,350 of unearned income (i.e., dividends or interest in a UTMA) is completely tax-free. The next $1,350 is taxed at the child’s own rate, which is generally 10%. However, once a child’s unearned income exceeds $2,700, every additional dollar is taxed at the parent’s highest marginal rate. This makes it critical to monitor high-yield assets or large capital gains with custodial accounts to avoid an unexpected tax bill.

Impact on Financial Aid (FAFSA) and Student vs. Parent Assets

When it comes to the FAFSA, not all educational savings accounts are equal. The formula counts money held in a custodial account (UTMA/UGMA) as a student asset and assesses it at a high rate of up to 20% each year. This can greatly reduce the amount of financial aid a student receives.

In contrast, parent-owned assets, including 529 plans, receive much more favorable treatment, as they are assessed at a maximum rate of only 5.64%. Retirement-focused tools like the new Trump Account (530A) or a Roth IRA offer an even greater advantage, because retirement accounts generally are not counted as FAFSA assets, although future distributions may affect financial aid calculations. Understanding the distinction lets families shield their savings from aid calculations while still providing for their child’s future.

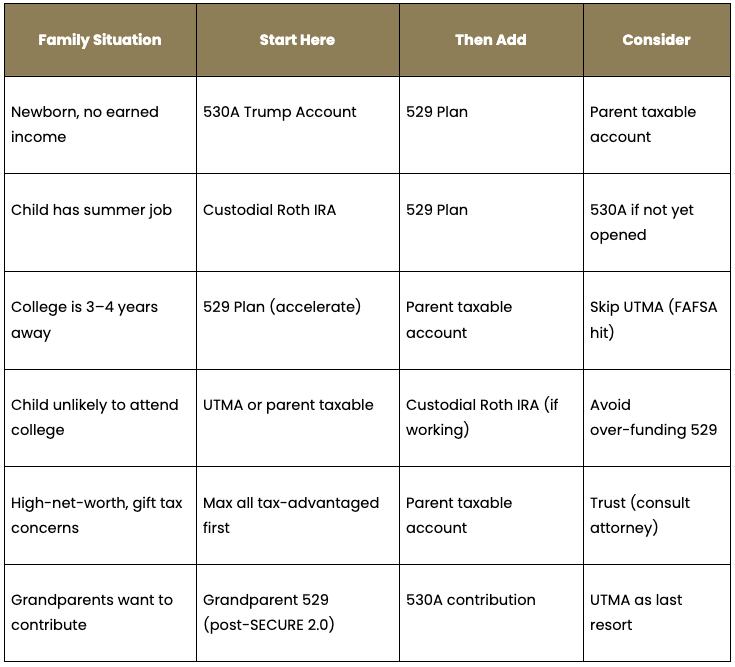

Choosing the Right Account Mix for Your Family Legacy

Modern wealth planning seldom involves picking just one account; instead, smart families use a stacking strategy to address different needs. You might start with a 530A Trump Account to capture the federal seed money and potential employer matches. Next, layer in a 529 plan to ensure education is funded with tax-free dollars.

Once your child begins a summer job, opening a Roth IRA locks in decades of tax-free growth on their earned income. This tiered approach provides dedicated funds for college, a massive head start on retirement, and the flexibility to handle life’s challenges. Because the landscape of education savings account options can be difficult to navigate, professional guidance is essential to ensure compliance with the 2026 federal gift tax limit of $19,000 per donor.

Why Some Families Prioritize Their Own Taxable Accounts First

While specialized accounts like 529 plans, custodial Roth IRAs, and UTMAs offer compelling tax advantages, many families overlook one of the most flexible planning tools available: their own joint taxable investment account.

For some parents, prioritizing savings in a jointly owned brokerage account can provide greater long-term control and adaptability than directing every dollar into child-specific accounts. Although this approach may not deliver the same upfront tax benefits as a 529 or retirement-focused vehicle, it offers something equally valuable: flexibility.

One of the most important realities in financial planning is that you can borrow for college, but you cannot borrow for retirement. Student loans, scholarships, grants, work-study programs, and income-based repayment plans all create ways to finance education later if necessary. Retirement, however, must generally be funded with assets accumulated during a family’s working years.

By keeping savings in their own names, parents maintain complete control over how and when the money is used. Funds can ultimately help pay for college, support a first-home purchase, assist with a wedding, supplement retirement income, or address unexpected family needs. Unlike custodial accounts, the assets do not automatically transfer to the child at the age of majority, and unlike 529 plans, the funds are not restricted to qualified education expenses.

This strategy can also create greater flexibility if a child receives scholarships, decides not to attend college, or pursues a less traditional career path. Parents are not forced to navigate rollover rules, penalties, or beneficiary changes to repurpose the funds.

There are tradeoffs, of course. Joint taxable accounts do not provide tax-free growth, and investment income may create annual capital gains or dividend tax liability. Parent-owned taxable assets may also still factor into financial aid calculations. However, for many families, the additional flexibility and retained control outweigh the reduced tax efficiency.

In practice, many high-net-worth and retirement-focused families use a blended approach: maximizing retirement contributions first, maintaining substantial savings in a joint taxable account, and then layering in targeted education savings vehicles such as 529 plans or custodial Roth IRAs where appropriate. This creates a financial plan that prioritizes parental security while still preserving opportunities to support future generations.

Conclusion

Building a financial legacy for your child is no longer a matter of simply opening a savings account and hoping for the best. With the introduction of the 530A Trump Account and the flexibility of modern 529 rollovers, the tools available to parents in 2026 are more powerful than ever before. Strategically stacking these accounts provides your children with a coordinated foundation that covers everything from their first classroom to their final retirement.

Here are some next steps:

- Review any existing UGMA or 529 accounts to see how they match with the 2026 Kiddie Tax and FAFSA rules.

- Determine if your child is eligible for the Federal Seed Money Pilot or if your employer offers a matching contribution.

- If your child has a summer job, start tracking their earnings now to maximize their 2026 Roth IRA contribution.

- Coordinate with a wealth manager to ensure your total annual gifts stay within the $19,000 tax-free limit.

Work with a Savvy Advisor Today!

Frequently Asked Questions

What is the best savings account for a child in 2026?

For most families in 2026, the best approach is to stack multiple accounts rather than relying on any single vehicle. Start with a 530A Trump Account, which requires no earned income and allows up to $5,000 per year in tax-deferred contributions. Layer in a 529 plan to cover qualified education expenses with tax-free growth. Once your child earns their first paycheck, open a custodial Roth IRA to begin building decades of tax-free retirement wealth. Each account targets a different goal: retirement, education, and flexibility, and together they form a coordinated foundation that addresses nearly every financial scenario a child might face.

Does a UTMA affect FAFSA?

Yes. A UTMA account is classified as a student-owned asset in the FAFSA formula and is assessed at a rate of up to 20% when calculating your child's Expected Family Contribution. This is significantly higher than the 5.64% rate applied to parent-owned assets such as a 529 plan.

Can you open a Roth IRA for a minor with no income?

No. A custodial Roth IRA requires the minor to have legitimate earned income, such as W-2 wages or documented self-employment income, in the year a contribution is made, and contributions cannot exceed the child's actual earnings, regardless of the annual federal limit.

What is a 530A Trump Account?

A 530A Trump Account is a new type of tax-advantaged account introduced in 2026 that allows families to begin saving for a child's long-term financial future without requiring the child to have earned income. Annual contributions are capped at $5,000, with up to $2,500 of that available as a pre-tax employer contribution. Investments are generally limited to diversified, index-style funds designed for long-term growth, and the account grows tax-deferred. Traditional IRA rules apply once the beneficiary reaches adulthood.

Can you transfer a 529 to a Roth IRA?

Yes, under a provision introduced by SECURE 2.0. Eligible beneficiaries can roll up to $35,000 from a 529 plan into a Roth IRA over their lifetime, subject to several conditions. The 529 account must have been open for at least 15 years, and contributions or earnings made in the prior five years are generally ineligible for rollover. Annual rollovers cannot exceed the standard Roth IRA contribution limit, which is $7,500 in 2026, and the beneficiary must have earned income equal to or higher than the rollover amount.

Dan grew up in the Chicago area and developed a strong interest in the stock market. After completing his bachelor's degree in business administration with concentrations in finance and information systems from Fordham University's Gabelli School of Business in New York City, he embarked on his career at Eze Software Group, a financial technology company and electronic trading software. Starting in client service, he steadily progressed to consulting and implementation roles, where he directly interacted with traders, portfolio managers, and operations personnel at institutional trade desks. During his time at Eze., he had the pleasure of meeting his wife, Jess. Together, they decided to relocate to Bellingham, Washington, to be closer to her family. This prompted his transition to Merrill, where he served as a financial advisor, gained valuable experience, before eventually managing a local independent advisory office in Bellingham. His specialization is to help individuals in our community achieve their retirement goals. For those approaching retirement, his focus is on implementing effective savings and contribution strategies. For those already in retirement, he prioritizes sustainable and tax-efficient income strategies. Collaborating closely with clients' tax professionals is crucial to ensure that our investment advice aligns seamlessly with their unique tax situations.

Works Cited

- IRS Publication 590-A, What’s New for 2026: https://www.irs.gov/publications/p590a#en_US_2025_publink100074297

- Trump Accounts | IRS: https://www.irs.gov/trumpaccounts

- Topic no. 553, Tax on a child's investment and other unearned income (kiddie tax): https://www.irs.gov/taxtopics/tc553

- Frequently asked questions on gift taxes: https://www.irs.gov/businesses/small-businesses-self-employed/frequently-asked-questions-on-gift-taxes

- Trump Accounts: Overview and Policy Considerations: https://www.congress.gov/crs-product/R48910

.webp)