Equity Markets Rise As Does Consumption; Even as Confidence Wanes

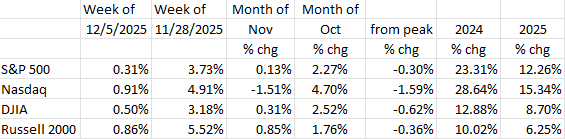

After sputtering for the first three weeks of November, the equity markets rallied during Thanksgiving week, and that resulted in three of the four major indexes finishing marginally in the black for the month of November (the Nasdaq was the exception). Markets continued to advance those gains during the first week of December as shown in the table. Except for the small-cap Russell 2000, which set a record high on Thursday, December 4th, the major indexes closed up for the week (December 5) but remained below their historic highs of late October and early November. Nonetheless, it appears that Mr. Bull is still in control. And while the gains in the major indexes for 2025 are not likely to be as awesome as those of 2024, they are still substantial (see table).

The “Santa” rally continued during the first week of December, led by tech and by small-caps, perhaps now playing “catch-up” as they have lagged the large caps in both 2024 and 2025 (see table). The question on everyone’s mind is: can the equity rally continue? The short answer is “no-one knows.” However, there are emerging signs that the economy is weakening, and, if those trends continue, economic growth will slow. And that isn’t conducive for equity values.

Consumer Attitudes

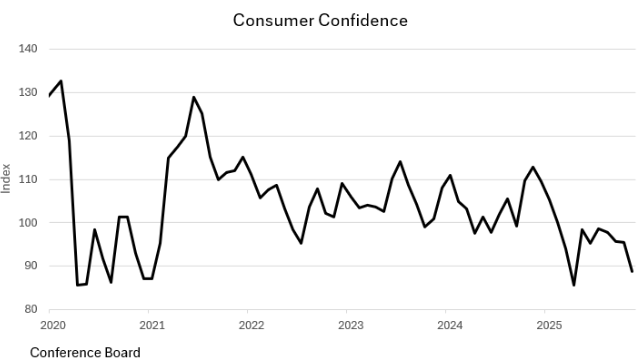

The University of Michigan’s Consumer Sentiment readings (51.0 November; 53.3 December) are sitting at levels registered during the COVID slowdown and are now at levels last seen in 1980 during the presidency of Jimmy Carter. November was the second lowest on record and below the troughs of all the downturns in the post-WWII era.1 The similar survey from the Conference Board showed up as the second lowest in the last five years. These surveys tend to be leading indications of consumer health, as lower confidence in the future is normally accompanied by frugality.

The most immediate question is: “Will consumers open their wallets/purses one more time for the holiday season?” The confidence surveys imply disappointment – consumers appear to be price conscious which implies that they will wait for post-holiday bargain prices. But the hard data, at least up till now, says the opposite:

- TSA screened a record 17.77 million passengers in the Monday (11/24) through Sunday (11/20) period.2 The previous high was set last year (17.76 million).

- Adobe Analytics reported record on-line sales ($44.3 billion) for the five days from Thanksgiving Thursday through Cyber Monday.3 This was a whopping 7.7% increase over last year’s (2024) record spending.3

So, while there are concerns about the health of the consumer, it isn’t yet evident in the spending data. We suspect that holiday spending will be the climax with frugality to follow in 2026. The trend toward frugality is evident. For example, three million more consumers shopped at Dollar Tree stores in Q3 compared to a year ago. We also note that in other western countries, i.e., the Eurozone, retail sales in October were flat (i.e., +0.0%).

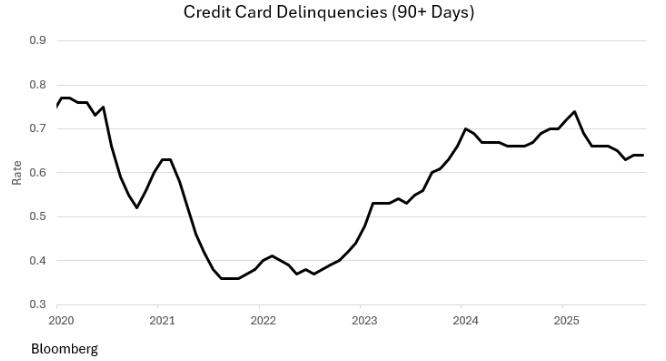

In addition, loan delinquencies continue at high levels. First, the good news. Credit card delinquencies, while still at high levels, have come off their peak levels of early 2025. Nevertheless, they remain at high levels showing strain in consumer wallets.

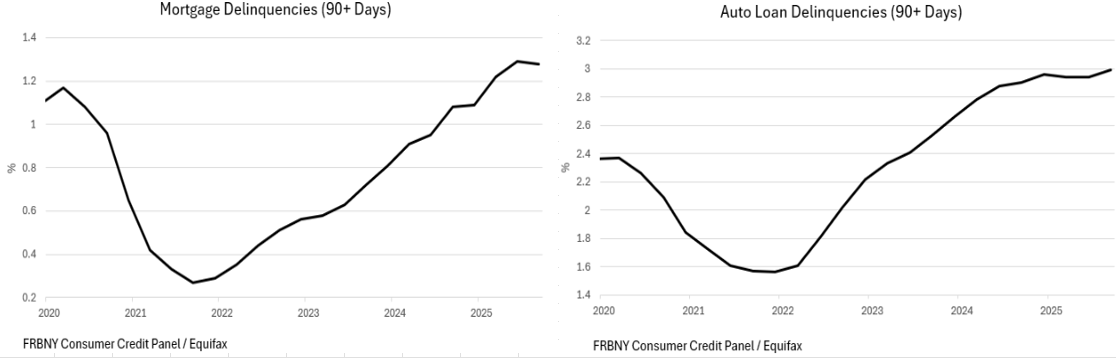

Unfortunately, this is not true for auto loans and mortgages; their delinquency rates have continued to move higher.

Inflation

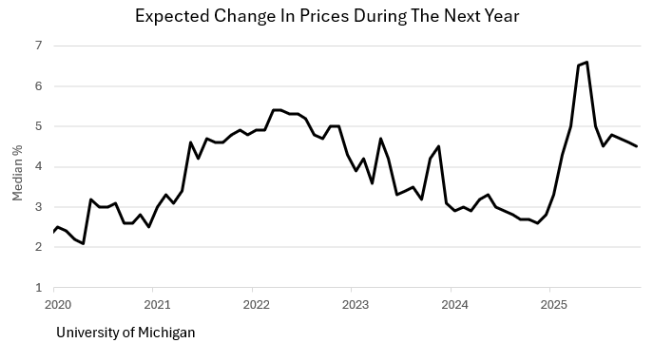

Inflation expectations remain stubborn. The chart shows one-year ahead consumer inflation expectations by month since October ’21, i.e., five years. In November ’24, those expectations bottomed at 2.6%. Then they rose to 6.6% last June. They currently sit at 4.5%. Inflation will continue to be problematic until such expectations are subdued.

Employment

Due to the government shutdown, the latest government (Bureau of Labor Statistics) data we have on employment is September. Being that we are already well into December, September’s data is somewhat stale. And there is a good chance that the next BLS release will be November’s data, skipping October altogether. So, we must look elsewhere for some clues.

One of those places is ADP’s private payroll data. October’s ADP data showed up as +47K. (In a healthy economy, this number is triple digits.) Then November clocked in at -32K.4 November showed up as the third decline in the last four months and the fourth decline in the last six. Of significance, small businesses (<50 employees), which are trend leaders, showed up with large payroll losses (-120K). Worse, in the four months ending in November, payrolls shrank by a rather large -222K, the worst four-month performance since the Pandemic (2020) and before that, 2010 (the Great Recession). Challenger, Gray and Christmas indicate that job cuts surpassed +153K in October, up 175% from a year earlier. According to Challenger:

“October’s pace of job cutting was much higher than average for the month. Some industries are correcting after the hiring boom of the pandemic, but this comes as AI adoption, softening consumer and corporate spending, and rising costs drive belt-tightening and hiring freezes. Those laid off now are finding it harder to quickly secure new roles, which could further loosen the labor market” said Andy Challenger, workplace expert and chief revenue officer for Challenger, Gray & Christmas.

As an observation, rising unemployment has always been associated with falling inflation expectations. And while higher joblessness may be a hard pill to swallow, after three years of stubborn inflation, it may be the only alternative.

Business

The ISM Manufacturing Index for November showed up at 48.2.5 The demarcation between expansion and contraction is 50. And the Industrial Production Index has flatlined, moving up a scant +0.1% in September after August’s -0.3% drubbing (latest data). Given the slowing economy, we suspect that both October and November Industrial Production data will show flatlines at best and are likely contracting.

Final Thoughts

The equity markets continued higher during December’s first week with the small cap Russell 2000 hitting a record high on Thursday, December 4th.

With consumer confidence now in decline, can economic growth continue? The sentiment surveys indicate a souring consumer, but the latest hard data shows that concerns about the consumers’ health are misplaced, or at least premature. Nevertheless, rising loan delinquencies bear watching.

Due to the government shutdown, the latest employment data comes from ADP (-32K November). This was the third decline in the last four months and the fourth in the last six. Challenger Gray and Christmas indicate that the labor market has loosened, i.e., jobs are harder to find.

The Fed meets on December 9-10. While BLS data is still scant, other economic markers indicate some economic slowing; so we expect a 25-basis point rate reduction.

Dr. Robert Barone, Ph.D. is an economist whose storied career spans numerous decades and positions within the world of finance. Since gaining his Ph.D. in Economics from Georgetown, he has been a Professor of Finance (University of Nevada), a community bank CEO (Comstock Bancorp), and a Director of the Federal Home Loan Bank of San Francisco, where he served as its Chair in 2004. He lives and breathes the world of finance, continuing to provide clients and avid Forbes readers with his latest market insights.

(Joshua Barone and Eugene Hoover contributed to this blog.)

Robert Barone, Joshua Barone and Eugene Hoover are investment adviser representatives with Savvy Advisors, Inc. (“Savvy Advisors”). Savvy Advisors is an SEC registered investment advisor. Material prepared herein has been created for informational purposes only and should not be considered investment advice or a recommendation. Information was obtained from sources believed to be reliable but was not verified for accuracy.

Ancora West Advisors, LLC dba Universal Value Advisors (“UVA”) is an investment advisor firm registered with the Securities and Exchange Commission. Savvy Advisors, Inc. (“Savvy Advisors”) is also an investment advisor firm registered with the SEC. UVA and Savvy are not affiliated or related.

Reference:

1 https://library.cqpress.com/cqalmanac/document.php?id=cqal80-1176058#_

5 https://tradingeconomics.com/united-states/business-confidence