If you’re tired of seeing part of your investment gains disappear to taxes annually, consider tax loss harvesting as a strategy. With it, investors can reduce their tax burden in taxable accounts, particularly when market declines occur.

Many investors miss opportunities to preserve gains. Why? They aren’t actively managing the tax impact of their portfolios. For example, selling a stock that dropped 10% while realizing gains elsewhere can lower your tax bill.

This guide explains what tax loss harvesting is, how it works, and how to implement it to enhance after-tax returns.

Talk with a Savvy Advisor Today!

Key Takeaways

- Tax loss harvesting involves selling investments in taxable accounts that have declined in value to offset realized gains from other assets, thereby lowering your overall tax bill.

- If your total losses exceed your gains, you can use up to $3,000 of the excess loss to offset ordinary income for the year, with remaining losses carrying forward indefinitely to future tax years.

- To preserve the portfolio's risk and return profile, proceeds from the sale should be reinvested into a distinct but correlated asset (e.g., swapping an S&P 500 ETF for a Total Market ETF).

- The IRS disallows a tax loss if you repurchase the same or a "substantially identical" security within 61 days (30 days before or after the sale). This rule applies across all your accounts, including IRAs.

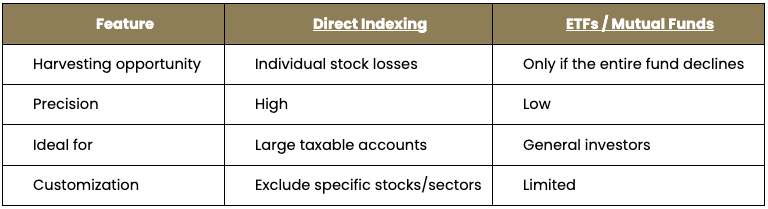

- Unlike ETFs, which can only be harvested if the entire fund declines, direct indexing involves owning individual stocks, allowing you to harvest losses on specific underperforming companies even when the broader index is performing well.

- Investors can utilize automated harvesting tools offered by major brokerages or hire professional advisors (RIAs) for complex strategies, such as direct indexing, provided that the potential tax savings outweigh the management fees.

Understanding Tax Loss Harvesting: Definitions, Benefits, and Rules

Let’s start with the basics: what is tax loss harvesting? At its core, tax loss harvesting involves selling investments in a taxable account that have declined in value. Realizing these losses allows you to offset gains from other assets.

What is Tax Loss Harvesting and How Does It Work?

Now that we’ve laid the groundwork, let’s move on to our next question: how does tax loss harvesting work? When an investment drops in value, selling it enables you to capture a realized loss. That loss offsets gains from other investments in taxable accounts, reducing your tax bill.

An important note: this strategy does not apply to tax-advantaged accounts such as IRAs or 401(k)s. Even modest losses can, over time, preserve more capital for compounding. For instance, selling a tech ETF that dropped 8% in a volatile quarter can offset gains from a bond fund sale, lowering your net taxable gain.

Reinvesting and Maintaining Market Exposure

After selling a losing investment, you can reinvest in a similar but not “substantially identical” asset. This tax-loss harvesting strategy maintains your portfolio’s risk and return profile while capturing the tax benefit.

If you sell a large-cap S&P 500 ETF at a loss, you could reinvest in a different large-cap index fund. Remaining invested keeps you positioned for a market recovery while staying compliant with IRS rules.

The Mechanics of Offsetting Gains and Ordinary Income

If total losses exceed gains, up to $3,000 annually can be applied against ordinary income. Excess losses carry forward indefinitely, so you can apply them against gains in future years.

Consider the case where your total realized losses are $7,000, and gains are $4,000. You can use $3,000 to offset ordinary income this year and carry forward the remaining $3,000 to next year.

Such an efficient use of losses prevents unrealized declines from going to waste.

Navigating the Wash Sale Rule: The Essential Guardrail

The wash sale rule is an IRS regulation that prevents investors from claiming a tax loss if they repurchase the same or “substantially identical” security too quickly. Violating this rule can disallow your loss, eliminating the intended tax benefit.

That’s why understanding this tax loss harvesting rule is so critical.

Defining the Wash Sale and the 61-Day Window

A wash sale occurs if the same security is repurchased within 61 days of the original sale, including 30 days before and after.

This prevents creating “artificial” losses. Selling a losing stock on December 15 and repurchasing it on January 5 would violate the rule, disallowing the loss for tax purposes. Careful timing ensures harvested losses remain valid.

Identifying “Substantially Identical” Securities

“Substantially identical” assets include not only the same stock but also very similar ETFs or mutual funds. Simply selling one fund and buying a nearly identical one may trigger the rule.

Investors can avoid this by swapping into a correlated but distinct asset. Replacing an S&P 500 ETF with a total market ETF captures similar growth potential while maintaining compliance.

Application Across IRAs and Multiple Brokerage Accounts

The wash sale rule applies across all accounts, even if held at different brokerages. Selling a security at a loss in a taxable account and repurchasing it in an IRA can trigger the rule.

For instance, selling a taxable account position at a loss and purchasing the same security in a Roth IRA within 30 days would disallow the loss. The IRS treats all accounts under your name as a single entity, so careful tracking across accounts is crucial.

Handling Disallowed Losses and Cost Basis Adjustments

If a wash sale occurs, the loss is temporarily disallowed, rather than permanently lost. The disallowed loss is added to the cost basis of the newly purchased shares, preserving the tax benefit until those shares are sold.

Let’s say you sold a stock for a $2,000 loss but repurchased it too soon. That $2,000 is added to the cost basis of the new shares. The benefit is realized eventually, just delayed.

Advanced Tax Strategies: The Power of Direct Indexing

Direct indexing involves buying the individual stocks within an index rather than a single fund or ETF. Investors can then harvest losses at a granular level and manage concentrated holdings.

Owning the individual components lets you take advantage of small losses even when the index is up. Selling an underperforming energy stock in a broadly rising index can generate a tax deduction without altering the portfolio’s performance.

What is Direct Indexing and How Does It Maximize Tax Efficiency?

Direct indexing enables investors to sell underperforming stocks individually to realize losses and keep the portfolio aligned with market benchmarks.

Because each stock can be harvested separately, tax benefits increase. That kind of granular approach turns minor declines into potential tax savings.

Granular Harvesting vs. Pooled Funds like ETFs

Direct indexing allows a higher degree of precision and flexibility. Investors with large or complex taxable accounts find this especially valuable.

Customization and ESG Benefits for Wealthy Investors

Direct indexing allows investors to exclude specific companies or sectors based on their personal values, such as ESG priorities. It also reduces the concentration risk from existing holdings, such as company stock.

The combination of tax efficiency and customization makes direct indexing an appealing option for sophisticated investors seeking portfolios tailored to both financial and ethical objectives.

Learn more about High-Net-Worth Financial Planning Strategies.

Implementing Your Strategy: Services and Pricing

Major brokerages such as Vanguard, Fidelity, and Schwab offer automated tax loss harvesting. It involves tracking portfolio losses and executing trades without constant manual oversight.

Direct indexing is typically accessed through RIAs or specialized platforms like Wealthfront or Public.com. Professional guidance guarantees proper execution, compliance, and alignment with broader financial objectives.

Minimum Investment Thresholds and Fee Structures

Full-featured direct indexing services often require $100,000–$250,000 minimum investments. Fees usually range between 0.1% and 0.5% of assets under management.

A $200,000 portfolio paying 0.25% annually would cost $500 per year, often far less than the potential tax savings from harvested losses. Evaluating ROI empowers informed decisions about strategy use.

Managing Capital Gains and Long-Term Tax Planning

Harvested losses offset short-term gains taxed at higher rates, providing immediate value. Holding assets longer allows them to qualify for favorable long-term capital gains rates.

Gain-harvesting in low-tax years can reset cost basis without triggering wash sale rules. Conducting a year-end portfolio review ensures the capture of unrealized losses before December 31.

Finding a Capital Gains Tax Specialist or Planning Service

High-net-worth investors benefit from CFPs and CPAs who specialize in tax planning. Advisors can model scenarios, optimize harvesting strategies, and provide protection against wash sale errors.

Vetting advisors carefully verifies that their approach aligns with your portfolio complexity and long-term goals. Checking expertise and client references are helpful steps in the vetting process.

Talk with a Savvy Advisor Today!

Key Takeaways for Tax-Efficient Growth

What to remember:

- Tax loss harvesting and direct indexing can preserve gains and enhance after-tax returns.

- Understanding IRS rules, using granular strategies, and reviewing accounts regularly support tax efficiency.

What to do next:

- Review taxable accounts for potential losses.

- Confirm compliance with wash sale rules.

- Explore automated harvesting or direct indexing solutions.

- Consult a professional advisor for complex portfolios or guidance.

FAQs

How much capital gains tax do I pay on $100,000?

It depends on whether the gain is short-term or long-term and your income level. Short-term gains are taxed at ordinary income tax rates. Long-term gains are taxed at 0%, 15%, or 20% federally. For many investors, $100,000 of long-term gains is taxed at 15%, but higher earners may owe 20% plus a 3.8% net investment income tax.

How to get 0% tax on long-term capital gains?

You qualify if your taxable income stays below IRS thresholds for the 0% capital gains bracket. For single filers, that means keeping taxable income below the lower limit set for the year. Income timing, deductions, and withdrawals all affect eligibility.

What is the 6-year rule for capital gains tax?

There is no official IRS “6-year rule” for capital gains on stocks. The term is sometimes confused with real estate rules or state-specific tax provisions. For investments, holding period rules are short-term (one year or less) and long-term (more than one year).

What is the 7/5/3-1 rule in mutual funds?

This is not an IRS rule. It’s an informal guideline sometimes used by advisors to describe declining sales charges or holding-period breakpoints in certain mutual funds. It does not affect how capital gains taxes are calculated.

Can you write off 100% of stock losses?

No. Capital losses first offset capital gains. If losses exceed gains, up to $3,000 per year can be deducted against ordinary income. Any remaining losses carry forward to future years until used.

Hi 👋🏼 I'm Ryan. I help individuals, families, and business owners build plans that offer clear financial direction while empowering them to make the most of their resources and lead more fulfilling lives. I specialize in complex estate and wealth transfer planning, tax strategies that minimize lifetime income taxes, and designing sustainable, tax-efficient retirement income plans. I view this profession as a noble calling, and I'm committed to building clear, personalized plans that help clients confidently prepare for the future.

Contact a Savvy advisor

Contact a Savvy advisor